A Safe 5x Now Loses to a 50x Maybe

Venture funds live on outliers, so a dependable non-AI 5x loses to an AI lottery ticket with a possible 50x. Here is the portfolio math that buries good companies, and the way around it.

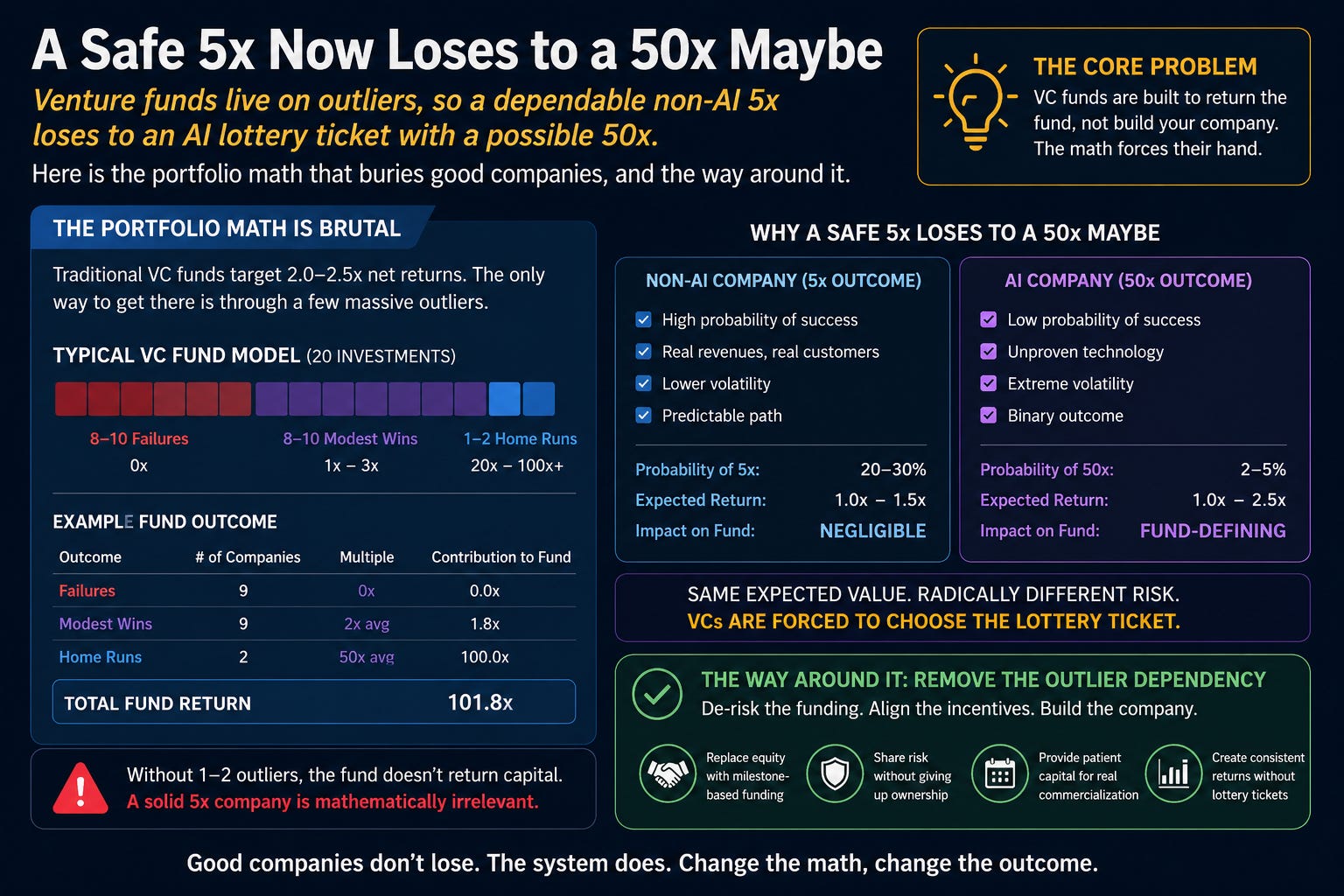

Your company could be excellent and still be wrong. Not wrong as a business, wrong as a bet. Venture funds live and die on outliers, so a dependable 5x non-AI winner loses every time to a wild 50x AI maybe. It is not personal. It is portfolio math, and the math is brutal.

The Math Nobody Pitches You

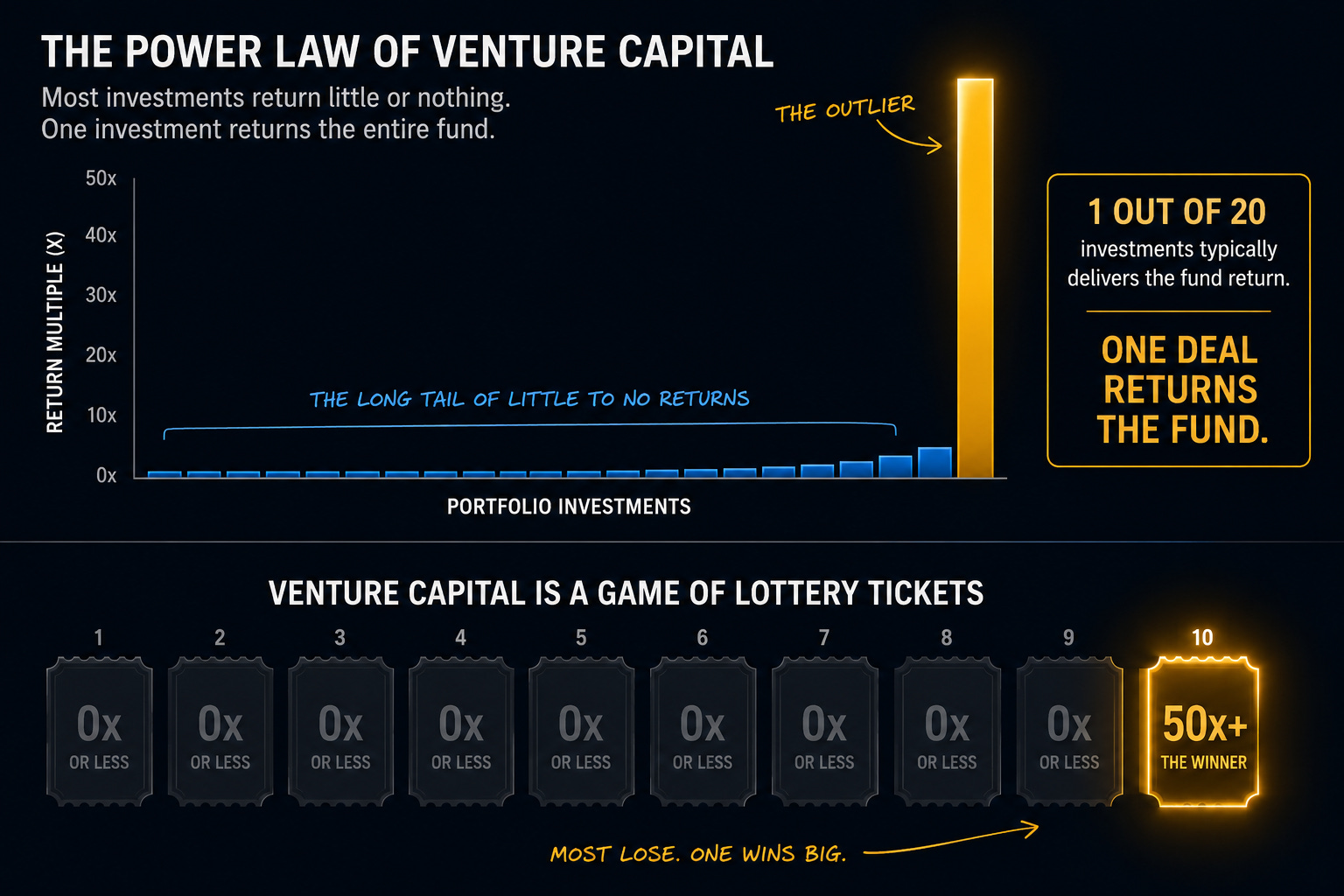

Venture capital runs on a principle most founders never hear stated out loud: the power law. A fund does not expect every bet to win. It expects most of them to lose. Out of ten investments, six go to zero, two or three limp back roughly what went in, and the entire fund rides on one or two breakout outliers. Put numerically, about 6 percent of venture deals generate roughly 60 percent of all returns. One company is expected to return the whole fund.

That single fact quietly rewires the pitch meeting. The question in the investor’s head is not “is this a good business.” It is “can this return my fund.” They are scoring, in the background, whether you could plausibly become a 10x to 100x company. A solid, profitable, growing business that tops out at a respectable multiple is, in that frame, a polite no with a follow-up email.

It also explains the behaviour that drives founders mad. The relentless focus on total addressable market, the obsession with hypergrowth over profit, the allergy to a steady, cash-generating business: none of it is personal taste. It is the power law talking. A fund judged by its ability to return capital at a multiple cannot afford to fall in love with a tidy 2x. It needs the one bet that pays for everyone, so it hunts for the shape of a fund-returner and quietly screens out everything that is merely very good.

Why Your Probable 5x Loses to a Possible 50x

This is where AI walks in and breaks non-AI’s heart. A frontier AI bet carries a plausible story about becoming infrastructure, a platform, a model layer, a hyperscaler acquisition, the kind of outcome that returns a fund several times over. A great non-AI company carries a probable, sober 3x to 8x. Both can be true. Only one fits the model.

For a founder, a probable 5x is a triumph. For a family office, a strategic, or an angel, it is a perfectly good outcome. For a fund that must cover six zeros with a single moonshot, a probable 5x is mediocre, because it cannot carry the others. The arithmetic is indifferent to how good your business is.

So a non-AI company can be the better business, better margins, real paying customers, lower burn, a clearer path to profit, and still be the worse bet. That is the knife hidden in the napkin. And the capital is voting with the math: AI took 65 percent of all 2025 deal value, while the largest AI financings dwarfed everything else on the board. You are not being judged on whether you can win. You are being judged on whether you can win big enough to matter.

The scale of the mismatch is almost comic. In a single recent quarter, a handful of AI and autonomy financings, names like OpenAI, Anthropic, and xAI, soaked up more than half of all venture dollars deployed on the planet. That is the bar your sensible logistics-software or medical-device company is implicitly measured against. Not because anyone believes you should be the next hyperscaler, but because the fund across the table needs at least one company that might be, and it would rather that slot go to a maybe-giant than a definitely-good. It is the same logic that lets an AI startup raise at nearly double a non-AI peer’s valuation for the same stage of progress.

[Suggested image: a seesaw or balance scale, a solid stone “5x” block on one side outweighed by a glittering “50x?” balloon on the other.]

The Exit Clock Without the Exit

Here is the cruel twist. Traditional venture capital still hands the non-AI founder the exit pressure, even though it will never hand over the fund-returner outcome. You inherit the seven to ten year clock, the standing pressure to swing for the fences, the board nudging you toward a binary outcome, while the swing-for-the-fences prize was never sitting on your table to begin with. You get the treadmill without the trophy.

And the engine is sputtering for everyone. Across recent vintages, distributions are running below the money investors paid in, and reported returns sit in single digits. The model is straining to produce the very outliers it depends on. Worse for you, the power law is roaring back in 2026. The cheap-money rising tide that once floated mediocre bets has gone out, the gap between the best funds and the rest is widening again, and only genuine outliers will clear the bar. For non-AI companies, that bar just moved to a different stratosphere.

The fallout lands on the founder. You get pushed to over-raise, over-promise, and over-swing, or to sell too early, optimizing your company around someone else’s lottery ticket instead of building something durable. You are running a sensible business inside a model that punishes sensible businesses.

None of this means venture capital is evil or even wrong. The power law is real, and for the rare company that can plausibly become enormous, the traditional deal is still the right tool. The mistake is assuming it is the only tool, or jamming a durable, profitable, non-AI business through a funnel engineered to find unicorns. A great many good companies do not fail in that funnel. They simply get told, politely and repeatedly, to keep everyone updated, while the clock they were handed keeps ticking.

Why The VC Risk Swap Changes the Math

This is where the VC Risk Swap quietly rewrites the equation, and it does so for both sides. The funder no longer needs your company to be the one-in-ten fund-returner; through a milestone-based revenue guarantee, backstopped by company-owned coverage, they get a defined, downside-protected return that does not depend on a unicorn or an IPO. The founder steps off the exit treadmill entirely, no forced fire sale, no swing-for-the-fences pressure, with value returned through milestones instead of a binary outcome. Both win on a probable, real result instead of an improbable, theatrical one.

Subscribe to SaferWealth for more field notes from the part of the funding world that does not fit the power law, plus the structures that let a good business get funded like a good business.

Questions about your specific situation? Reach out directly at riskswap@saferwealth.com.

CONNECT WITH SAFERWEALTH

Expand your learning beyond this post:

1. Web: SaferWealth.com, alternative startup funding structures.

2. YouTube: The Capital ToolKit, funding strategy and structure breakdowns.

3. Rumble: @SaferWealth.

4. Contact: riskswap@saferwealth.com.

ABOUT THE AUTHOR

Sean Cavanagh (BAS, CPA, CA, CF, CBV) is the founder of SaferWealth and creator of the VC Risk Swap, an alternative startup funding structure that preserves founder equity and control through milestone-based, downside-protected capital. With over three decades in business valuation, M&A advisory, and structuring, Sean writes about funding the businesses the venture market overlooks.

DO YOUR OWN RESEARCH

Sources referenced in this post:

• Qubit Capital on the VC power law, roughly 6 percent of deals drive 60 percent of returns.

• VC math, a founder’s guide to the power law, the 3 to 5x fund benchmark and 6-of-10 failure rate.

• BIP Ventures on the power law, the 10x to 100x company test.

• Commonfund, the re-emergence of the power law, why only outliers clear the bar in 2026.

• citybiz, AI’s 65 percent share of 2025 deal value.

• PitchBook-NVCA Venture Monitor, Q1 2026, returns below paid-in and top-deal concentration.

📖 RELATED READING

• Commonfund: Re-emergence of the Power Law of Returns: why the cheap-money tide going out punishes non-outliers.

• BIP Ventures: What is the Venture Capital Power Law: how the 10x to 100x test shapes every term sheet.

• PitchBook-NVCA Venture Monitor: the data on strained returns and deal concentration.

Educational disclaimer: This content is for educational purposes only and does not constitute legal, tax, financial, or investment advice. The VC Risk Swap is a sophisticated structure that must be implemented with independent professional advisors for your specific situation. All examples are illustrative. Neither the author nor SaferWealth accepts liability for actions based on this content. This material supplements but never replaces proper professional consultation and judgment.

© 2026 SaferWealth. All rights reserved.