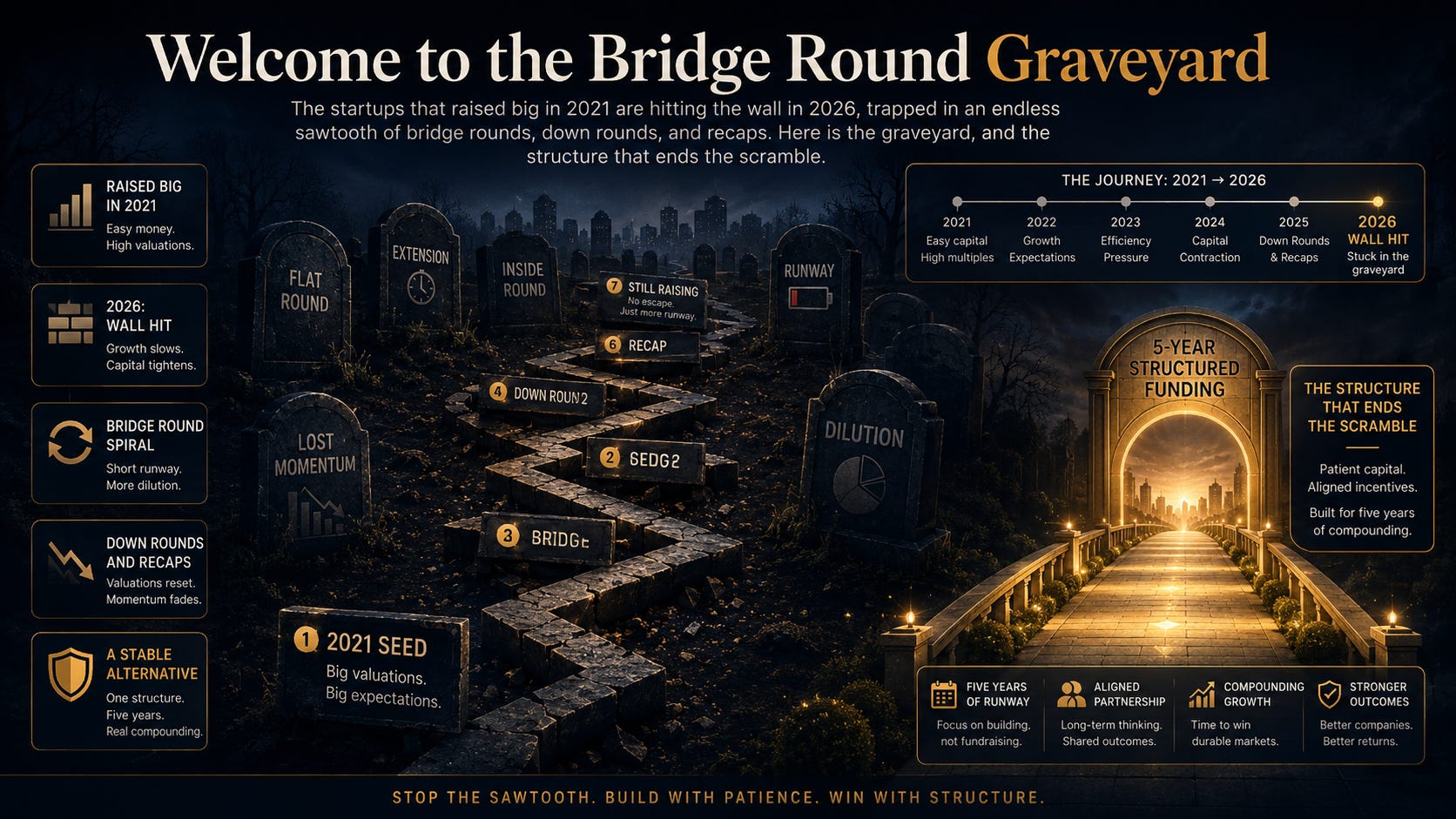

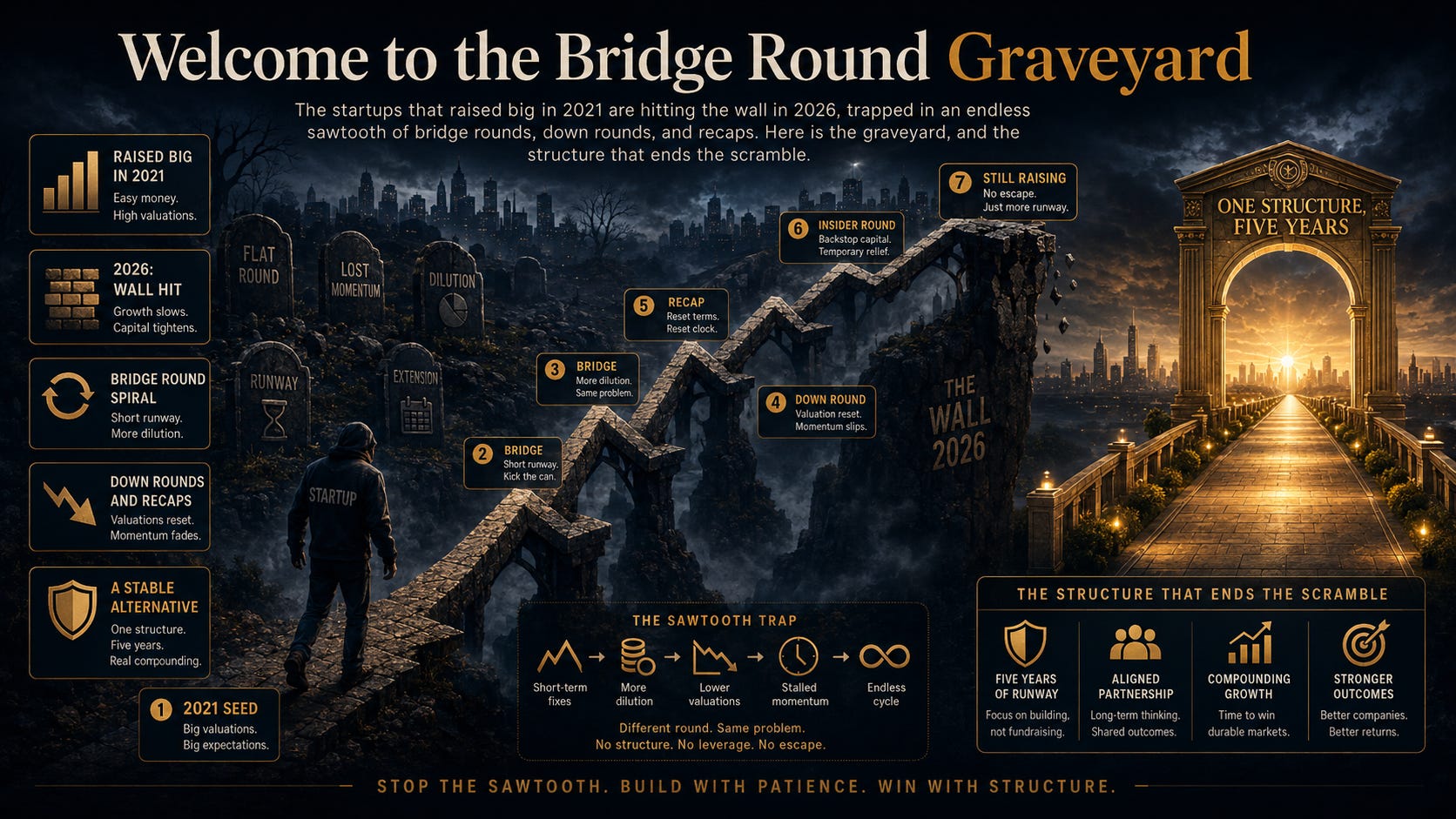

Bridge Round Graveyard

The startups that raised big in 2021 are hitting the wall in 2026

In 2021, money was free and valuations were fiction. Founders raised at dizzy numbers and told themselves the next round would be bigger. It never came. In 2026 those companies are stranded on a bridge to nowhere, raising a little, then a little more, forever. Welcome to the graveyard.

[Suggested image: a jagged sawtooth funding line that keeps spiking and dropping but never climbs, labeled bridge, bridge, bridge. Alternative: a literal bridge that ends mid-air over a foggy valley.]

The Party Everyone Is Still Paying For

In 2021 the money was cheap, the valuations were vertical, and everyone raised at the peak. The pitch was simple: grab as much as you can at the highest number you can, and the next round will be higher still. Then interest rates woke up, the music stopped, and those glorious valuations turned into anchors chained to the ankle.

The wreckage is measurable. Down rounds reached 24 percent of United States growth-stage financings in the first half of 2025, up from a 4 percent baseline in 2021. And here is the twist that should end the shame around them: roughly 60 percent of those down rounds involved companies whose revenue actually grew between the up round and the reset. It is not failure. It is repricing. The 2021 vintage was simply stamped with multiples that nobody in the 2026 market will underwrite, and in some sectors valuations fell by as much as 20x.

Part of the pain was self-inflicted, in the way a hangover usually is. Cheap money encouraged founders to raise too much, too soon. Companies grabbed a Series B three or four months after a Series A, never leaving enough runway to actually hit the metrics the next round would demand. The result was a generation of startups carrying valuations they had not yet earned, waiting for growth to catch up to a number that had already sprinted off ahead. In 2026, the growth is walking and the number is long gone.

The Moving Goalposts

While the valuations were sinking, the bar to clear the next round was quietly rising. A company that raised a Series A at $500,000 in ARR in 2021 now needs $1.5 to $2 million in ARR to justify a Series B. The same source notes the obvious cause: companies that projected 3x growth delivered closer to 1.5x. So you raised eighteen months of runway against a finish line that doubled while you were sprinting toward it.

The result is a widening canyon between rounds, and a lot of founders fall into it. More than half of Series A and B startups now fail to raise their next round of funding at all. Not because the businesses are bad, but because the goalposts moved faster than the runway could stretch. You did everything right and still arrived at the gap.

And the canyon is not evenly spaced. AI companies stroll across it on fresh capital raised at cheerful markups, while everyone else stares down at the drop. The usual detours, an insider bridge here, a slug of venture debt there, feel like progress, but as one 2026 analysis warns, they mostly postpone the repricing rather than prevent it. You are not crossing the canyon. You are paying rent to linger at its edge a little longer.

The Sawtooth and the Graveyard

Enter the bridge round, the financing equivalent of one more coffee to get through the night. You raise nine to twelve months of cash, chase the new milestone, and plan to raise the real round after. Except the bar moves again, so you bridge again, and again, and the whole thing turns into a sawtooth: a jagged line of small, dilutive, morale-sapping rounds that never reaches escape velocity. One 2026 guide puts the warning plainly: do not raise an eighteen-month bridge, because that is just a Series round with worse terms, and you will still need to raise the real one afterward. Worse, every bridge quietly signals to the market that you missed your last set of milestones. It is, in the old and honest phrase, a bridge to nowhere.

When the bridge finally fails to reach the far bank, the endgame gets grim, and it has a vocabulary all its own. The down round resets the valuation and can trigger anti-dilution. The recapitalization restructures the entire cap table. The cram-down or pay-to-play forces existing investors to write another cheque or be converted to common stock, and, as one guide bluntly notes, founders’ common shares get brutally diluted in the process. By the end, the team’s options sit underwater beneath a tall preference stack, worth precisely nothing on an exit that clears the preferences and stops.

None of this is rare anymore. When growth-stage companies do close a down round today, the deal almost always takes one of four shapes: a clean price reset, an insider bridge with a structured convertible, a pay-to-play recapitalization, or a new lead brought in to restructure the whole thing. The down round has quietly graduated from a shameful one-off into a standing operating pattern, an entire genre of financing with its own playbook. That is how normal the graveyard has become.

And the escape hatch marked AI is welded shut for this crowd. The AI exception means those companies keep commanding premium valuations while software, consumer, and capital-intensive startups absorb the resets. Guess which cohort is stuck out on the bridge, watching the fog roll in.

And the quietest casualty is the team. Salaries were traded for equity that, buried beneath a growing preference stack, is now worth a rounding error. Every bridge that dilutes the founder dilutes them too, and every reset pushes their options further underwater. People signed on to build a company, not to bail one out round after round, and morale drains a little further with each lap of the sawtooth.

Why The VC Risk Swap Ends the Scramble

This is where the VC Risk Swap trades the sawtooth for a single, multi-period milestone structure. There is no twelve-month scramble, no bridge to nowhere, and no down-round reset, because there is no priced round to reset. Funding is committed across periods against milestones, so the founder builds instead of perpetually fundraising and keeps equity intact through commercialization. The funder gets a defined, downside-protected return on a schedule, not a seat on a dilution spiral that ends in a recap. Both step off the treadmill and onto solid ground.

Subscribe to SaferWealth for more field notes from the bridge-round graveyard, plus the structures that let a good company stop fundraising and start building.

Questions about your specific situation? Reach out directly at riskswap@saferwealth.com.

CONNECT WITH SAFERWEALTH

Expand your learning beyond this post:

1. Web: SaferWealth.com, alternative startup funding structures.

2. YouTube: The Capital ToolKit, funding strategy and structure breakdowns.

3. Rumble: @SaferWealth.

4. Contact: riskswap@saferwealth.com.

ABOUT THE AUTHOR

Sean Cavanagh (BAS, CPA, CA, CF, CBV) is the founder of SaferWealth and creator of the VC Risk Swap, an alternative startup funding structure that preserves founder equity and control through milestone-based, downside-protected capital. With over three decades in business valuation, M&A advisory, and structuring, Sean writes about funding the businesses the venture market overlooks.

DO YOUR OWN RESEARCH

Sources referenced in this post:

• Yanne Capital, the down-round playbook, H2 2026, down rounds at 24 percent of growth-stage deals and the revenue-grew twist.

• Ellty, active bridge round investors in 2026, the higher ARR bar and the bridge-to-nowhere warning.

• Kruze Consulting, what is a down round, cram-downs, 20x resets, and bridges to nowhere.

• Eric Ashman, a guide to down rounds and recaps, over half of Series A and B startups fail to raise next.

• Crowley Law, down round survival guide 2026, the 2021 overhang and the AI exception.

• Morgan Lewis, staying in the fight, recap, washout, and cram-down mechanics.

📖 RELATED READING

• Yanne Capital: The Down-Round Playbook, H2 2026: the four structures behind today’s growth-stage resets.

• Crowley Law: Down Round Founder Survival Guide (2026): protecting equity when the 2021 valuation comes due.

• Ellty: Bridge Round Investors Extending Runway in 2026: why an 18-month bridge is a trap in disguise.

Educational disclaimer: This content is for educational purposes only and does not constitute legal, tax, financial, or investment advice. The VC Risk Swap is a sophisticated structure that must be implemented with independent professional advisors for your specific situation. All examples are illustrative. Neither the author nor SaferWealth accepts liability for actions based on this content. This material supplements but never replaces proper professional consultation and judgment.

© 2026 SaferWealth. All rights reserved.

PRODUCTION NOTES (not for publishing)

Meta description (SEO): The startups that raised big in 2021 are hitting the wall in 2026: down rounds at 24% of growth-stage deals, an endless sawtooth of bridge rounds, and brutal recaps. Plus the VC Risk Swap structure that ends the scramble.

SEO / GEO keywords: 2021 vintage overhang, down rounds 2026, bridge round graveyard, sawtooth financing, recapitalization startup, cram down, pay-to-play, extension round, runway gap, non-AI startup funding, milestone-based funding, VC Risk Swap.

Suggested images: (1) a sawtooth funding line that never climbs. (2) a bar chart, down rounds jumping from 4% in 2021 to 24% in 2025 of growth-stage financings.