Canada Builds Startups, America Buys Them

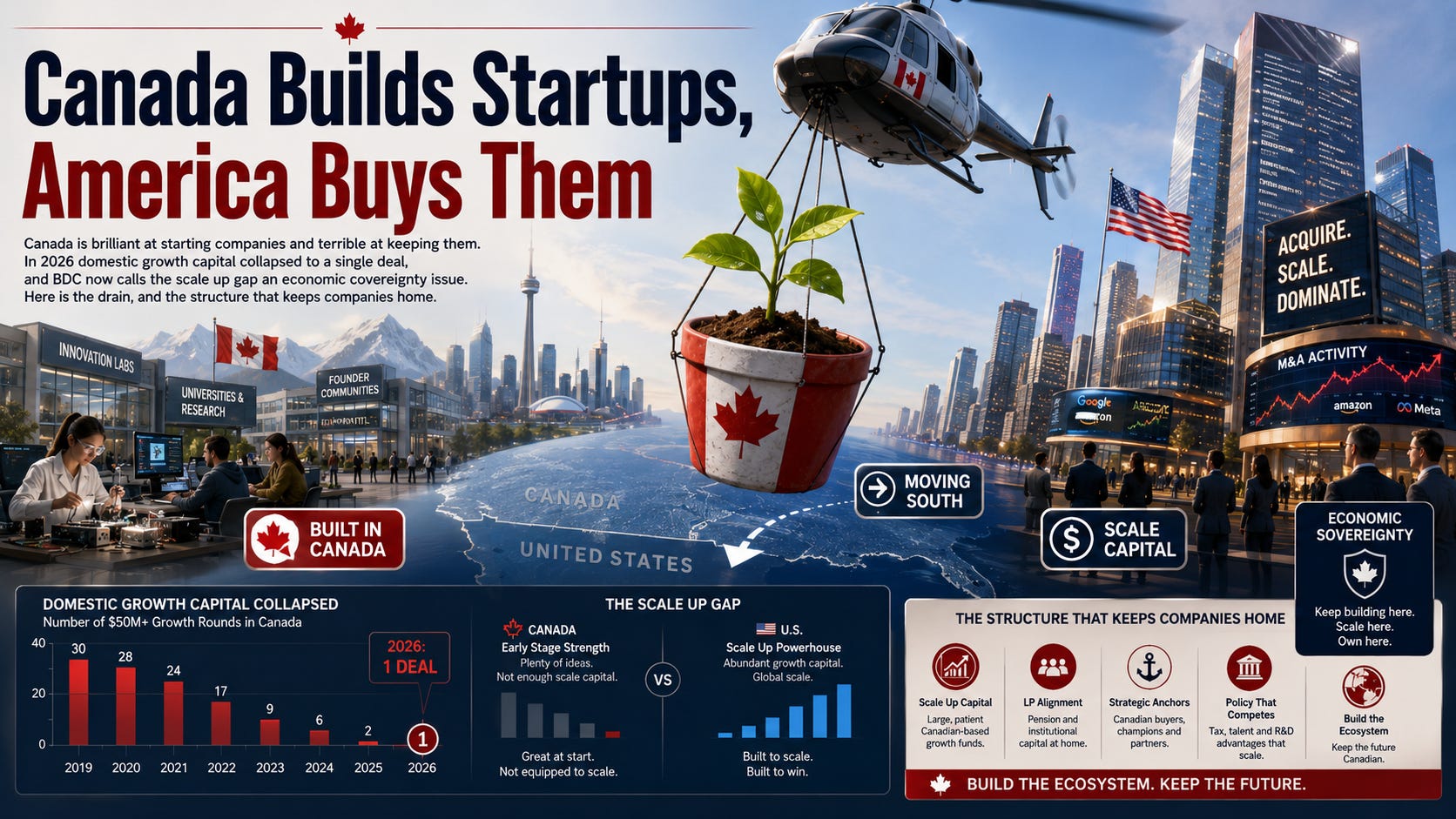

Canada is brilliant at starting companies and terrible at keeping them. In 2026 domestic growth capital collapsed to a single deal, and BDC now calls the scale up gap an economic sovereignty

Canada is a world class startup nursery. It raises brilliant young companies, then watches the best ones get bought, packed up, and flown south the moment they are ready to grow. In 2026 the domestic capital that used to keep them home nearly vanished. This is the story of a country quietly giving its winners away.

Good at Starting, Bad at Keeping

Canada has a strange talent. It is one of the best places on earth to start a technology company, and one of the worst to keep one. The Business Development Bank of Canada put it with painful simplicity in its 2026 landscape report: we are good at starting companies, we are just not getting them across the goal line. The bank gave the problem a name, the scale up gap, and then gave it a weight nobody expected, calling it an economic sovereignty issue rather than a mere market wrinkle.

The single number that captures it is almost hard to believe. In the first quarter of 2026, venture investment in Canadian growth stage companies fell to one deal worth roughly $1 million, against a typical first quarter of about $140 million. The CVCA recorded the lowest venture deal count in any quarter since 2017, and not a single initial public offering closed in the country all quarter. Canada is still minting promising young companies. It has simply stopped funding them the moment they try to grow up.

This is not a blip, it is the sharp edge of a trend the sector has watched harden for years. In 2025 Canadian startups and scaling firms raised about $8 billion, down from the year before, and just ten big ticket deals accounted for roughly half of everything invested, with AI alone taking about half the dollars. A late surge of a few megadeals flattered the annual total while the median company quietly starved. The headline held up. The middle fell out.

Where the Ownership Leaks Out

When domestic investors cannot write the big cheques, someone else does, and that someone is usually American. The pattern is visible in the data by round size. Canadian investors supplied more than 70 percent of the money in rounds under $5 million in 2024, but only 12.7 percent in rounds larger than $50 million. The bigger the round, the more foreign the cap table. Growth capital, the exact fuel a company needs to scale, is precisely where Canadian ownership thins out fastest.

And the lead investor in a round is never just a wallet. The lead typically takes the board seats, the governance rights, and a decisive say over the company’s exit strategy. So when a growth round is led from abroad, control over where the company goes, and whether it is eventually sold rather than taken public, quietly boards the same plane as the capital. The CVCA’s David Kornacki named the stage precisely. Growth is where foreign participation increases, domestic ownership dilutes, and acquisition becomes more likely than an IPO. It is a slow, polite handover, one term sheet at a time, and nobody in the room ever says the word out loud.

The exit math makes the direction of travel obvious. In that same quarter, every dollar of Canadian venture liquidity came from acquisitions, nine of them, and not a single company went public. When the only open door is a sale, and the buyers with the deepest pockets sit in another country, the outcome more or less writes itself. Growth capital does not just fund scaling. It quietly decides who owns the finish line.

The Farm Team Problem

String those facts together and you get a country that develops talent for another country’s league. Without domestic growth capital, the warning from Canadian capital circles is blunt: the scaling companies will leave, by relocation or by acquisition, and Canada settles into life as a farm team for the United States. BDC framed the loss plainly. If maturing firms are lost, Canada forfeits both the value those companies would have added at home and the returns on all the early money that built them.

The domestic engine is stalling at both ends. Concentration has become the whole story: the top five Canadian funds captured 46 percent of all capital raised in 2023, and 80 percent by 2025, while every other fund combined collapsed from $4.5 billion to $444 million, close to a 90 percent drop. The number of Canadian companies actively raising fell from 162 in early 2025 to just 61 a year later. Meanwhile investors themselves flag a widening innovation gap and a struggle to retain intellectual property and scale companies at home before they are bought by foreign interests, all of it sharpened by a familiar drain of talent to Silicon Valley.

BDC’s Geneviève Bouthillier did not soften it. The heavy reliance on foreign capital to fill the gap, she said, is no longer just a feature of the market, it carries real consequences for Canada’s ability to retain ownership, decision making, and long term value. In a year of trade tension and rising global competition for strategic technology, a startup that quietly becomes American is not only a lost cap table. It is a lost piece of the country’s economic future.

To be fair, this is not a case against foreign money. American capital is welcome, and United States investment in Canada is beginning to recover. The real problem is the missing domestic option. When there is no Canadian cheque big enough to lead the round, reliance stops being a choice and becomes a dependency, and dependency is exactly where ownership, control, and the eventual payday leak out of the country.

Why The VC Risk Swap Keeps Companies Home

This is where the VC Risk Swap gives a Canadian company a way to fund its scale up without handing a foreign lead the board seats, governance rights, and exit control that come with a big priced round. The founder keeps Canadian ownership and decision making, and is not steered toward a foreign sale just to manufacture a return. The funder, often a domestic one, gets a defined, downside protected return through a milestone based revenue guarantee, without needing to write a giant cheque or wait for an acquirer to appear. Both keep the company, and its upside, in Canada.

Subscribe to SaferWealth for more field notes from the part of the funding world the venture market overlooks, plus the structures that fund good companies on their own terms.

Questions about your specific situation? Reach out directly at riskswap@saferwealth.com.

CONNECT WITH SAFERWEALTH

Expand your learning beyond this post:

1. Web: SaferWealth.com, alternative startup funding structures.

2. YouTube: The Capital ToolKit, funding strategy and structure breakdowns.

3. Rumble: @SaferWealth.

4. Contact: riskswap@saferwealth.com.

ABOUT THE AUTHOR

Sean Cavanagh (BAS, CPA, CA, CF, CBV) is the founder of SaferWealth and creator of the VC Risk Swap, an alternative startup funding structure that preserves founder equity and control through milestone based, downside protected capital. With over three decades in business valuation, M&A advisory, and structuring, Sean writes about funding the businesses the venture market overlooks.

DO YOUR OWN RESEARCH

Sources referenced in this post:

• The Hub, growing Canadian companies finding nearly zero VC, the single $1 million growth deal in Q1 2026.

• CVCA, Q1 2026 market overview, the lowest deal count since 2017 and the Kornacki quote.

• The Logic, CVCA urges Ottawa to fund growth firms, the 70 percent to 12.7 percent ownership split by round size.

• BetaKit, Canada’s scale up gap now a sovereignty issue, the BDC landscape report and the goal line quote.

• BDC, Canada must scale what it creates, the economic sovereignty framing.

• RBCx, Canadian venture capital report 2026 mid year, the fund concentration and the drop in active raises.

• CVCA Central, 2026 Canadian private capital outlook, IP retention and the brain drain.

• Research Money, how to spend $750 million, the farm team warning.

📖 RELATED READING

• BDC: Canada Must Scale What It Creates: why the scale up gap is now a sovereignty issue.

• The Logic: CVCA Urges Ottawa to Back Growth Firms: where Canadian ownership leaks out by round size.

• CVCA: Q1 2026 Market Overview: the quarter growth capital nearly disappeared.

Educational disclaimer: This content is for educational purposes only and does not constitute legal, tax, financial, or investment advice. The VC Risk Swap is a sophisticated structure that must be implemented with independent professional advisors for your specific situation. All examples are illustrative. Neither the author nor SaferWealth accepts liability for actions based on this content. This material supplements but never replaces proper professional consultation and judgment.

© 2026 SaferWealth. All rights reserved.