How January 2026 Changed Venture Capital Forever

From experimentation to agentic execution, January 2026 reveals how billion-dollar bets on autonomous systems and DPI-focused exits create alternative capital urgency

January 2026 marks venture capital’s pivot from “AI experimentation” to “Agentic Execution.” While billion-dollar funding rounds close for autonomous systems and IPO windows reopen selectively, an estimated 80% of fundable companies face unprecedented capital scarcity. The traditional VC model now excludes more opportunities than it serves, creating a $290 billion alternative funding gap demanding new structures.

The IPO Market’s Selective Resurrection

January 2026 witnessed what analysts are calling “The Great Unlocking,” a massive resurgence in liquidity events that many believed would never return. After four years of near-total drought, the IPO market has reopened with dramatic fanfare. Fintech companies like Klarna and Chime successfully went public this month, proving that investor appetite has returned for the right companies.

But here’s what makes 2026 fundamentally different from previous IPO cycles: selectivity has become the defining characteristic. The companies reaching public markets today look nothing like the 2021 cohort. They have actual revenue, proven unit economics, clear paths to profitability, and often, they’re already profitable.

The market is bracing for potential blockbuster listings:

SpaceX rumored at $800+ billion valuation

Anthropic preparing for potential H2 2026 listing with $26 billion projected revenue

OpenAI laying groundwork for $1 trillion valuation IPO

Multiple late-stage companies with fundamentals that would have been considered conservative in previous cycles

The implications for founders are stark. “Zombie fintechs” and companies that raised at 2021 peak valuations face down-rounds or liquidation. The IPO window isn’t closed, it’s just become far more discriminating about who gets through.

What This Means for Capital Structure Planning

The selective IPO recovery fundamentally changes how founders should think about capital structure planning from day one. If your pathway to traditional exit looks uncertain, designing alternatives from inception costs exponentially less than retrofitting later.

January’s Billion-Dollar Bets: Where the Money Actually Went

Beyond the IPO headlines, January 2026 witnessed massive capital deployment that reveals exactly where sophisticated investors are placing their bets. The pattern is unmistakable: autonomous systems, physical AI, and vertical-specific applications dominate the largest rounds.

Waabi’s $1 Billion Physical AI Breakthrough

On January 28, Toronto-based Waabi secured $1 billion in Series C and milestone-based funding, led by Khosla Ventures and G2 Venture Partners. This isn’t just another AI round, it represents the market’s decisive shift toward “Physical AI” that operates in the real world rather than purely digital environments.

The capital targets two massive opportunities: commercialization of autonomous trucking systems and a robotaxi partnership with Uber. This Canadian success story demonstrates that AI infrastructure extending beyond pure software commands premium valuations and attracts patient, milestone-based capital structures.

Why this matters for alternative funding: The milestone-based component of Waabi’s structure mirrors concepts in the VC Risk Swap, where capital deployment ties to verified achievement rather than pure valuation speculation. This represents sophisticated investors recognizing that complex physical systems require patient capital with performance validation.

The $5.15 Billion Brex Acquisition Signals Consolidation Acceleration

Capital One’s January 22 agreement to acquire expense management unicorn Brex for $5.15 billion represents what analysts are calling “the largest bank-fintech deal in history.” This isn’t just an acquisition, it’s a strategic acknowledgment that legacy financial institutions must buy AI-native fintech stacks to remain competitive.

The deal accelerates three critical trends:

AI-native infrastructure becomes acquisition target: Companies that built with AI from inception command premium valuations from legacy players lacking technical capability

Fintech consolidation reaches mature stage: The experimental phase has ended, winners are being acquired at massive multiples

Strategic M&A provides alternative exits: Founders unable or unwilling to pursue IPO paths now have proven strategic acquisition pathway

This validates the VC Risk Swap thesis that patient capital enabling longer development timelines ultimately produces more valuable exit opportunities. Brex didn’t rush to IPO at suboptimal valuations, instead building defensible market position that legacy players were forced to acquire.

xAI’s $20 Billion Series E and the Foundation Model Arms Race

Elon Musk’s xAI closed a $20 billion Series E in early January, jumping to second place in the AI model funding race behind only OpenAI. The capital scales xAI’s “Colossus” compute cluster, representing the ongoing arms race in foundation model development.

The implications are stark: only companies with access to billions in patient capital can compete in foundation model development. This creates natural consolidation around a handful of well-capitalized players while opening massive opportunities in vertical applications built on these foundation models.

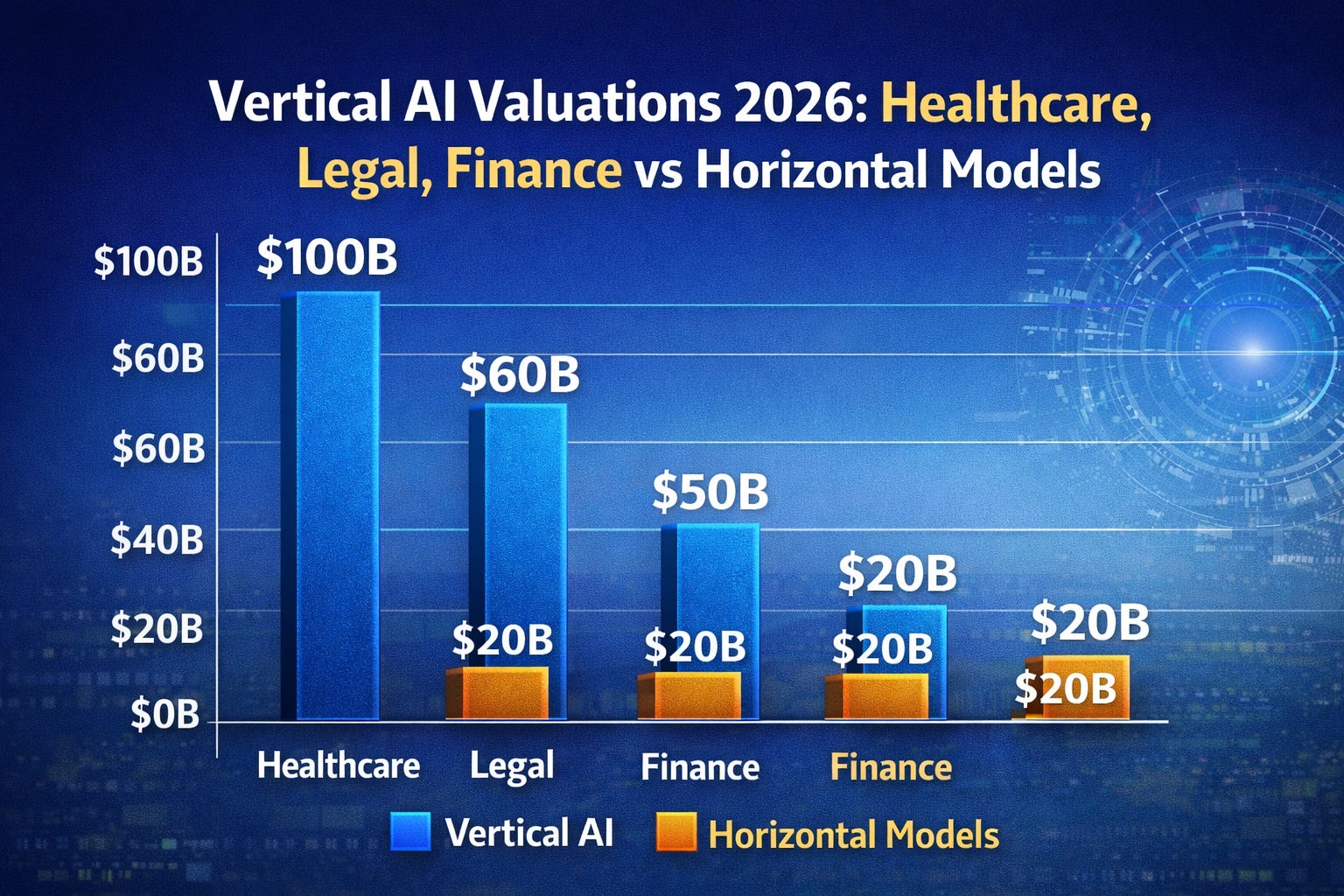

OpenEvidence Hits $12 Billion: The Vertical AI Validation

Medical AI startup OpenEvidence reached a $12 billion valuation on January 21, exemplifying the “Vertical AI” trend where industry-specific models outperform generalist approaches in both utility and valuation growth.

Key insight: Healthcare, legal, financial services, and other regulated verticals require specialized models with domain expertise and compliance capabilities that horizontal platforms can’t replicate. These vertical plays often require 7-12 year development timelines to build proprietary datasets, establish regulatory approvals, and achieve clinical validation, exactly the patient capital profile the VC Risk Swap addresses.

[Insert IMAGE: Vertical AI Valuation Comparison Chart with alt text: “vertical AI healthcare legal finance valuations 2026 versus horizontal models”]

AI Dominance Has Created a Two-Tier Investment Universe

The single most defining trend in January 2026 is the complete bifurcation of venture capital into AI versus non-AI companies. This isn’t gradual evolution, this is structural market transformation happening in real time.

The numbers tell a dramatic story:

US accounts for 85% of global AI funding

AI startups attracted 33% of all global venture capital in 2024

AI companies command 42% valuation premiums at seed stage

Four of the seven largest AI rounds globally were US-based

Foundation models and agentic infrastructure dominate growth capital deployment

One VC managing director stated it bluntly: “It will be very difficult for a SaaS company without native AI/agentic capabilities to find VC dollars at any stage.” Another noted that institutional investors show “zero interest” in non-AI deals, a mindset that has fundamentally reshaped what gets funded.

[Insert IMAGE: AI vs Non-AI Funding Split Chart with alt text: “AI startup funding dominance 2026 showing 85% US market concentration”]

The Non-AI Funding Crisis

For companies outside the AI gold rush, the valley of death has widened into a canyon. Only companies with exceptional unit economics, strong growth trajectories, and defensible competitive positions attract meaningful capital. The talent drain compounds the problem, as founders and engineers increasingly abandon other sectors entirely for AI opportunities.

This creates the precise scenario where alternative funding structures like the VC Risk Swap become not just attractive, but essential for survival. Companies with validated products, proven market demand, and multi-year development timelines can’t access traditional VC capital if they’re not building AI infrastructure.

Agentic AI Transforms How VCs Actually Operate

Perhaps the most overlooked development in January 2026 is how AI hasn’t just changed what VCs fund, it’s fundamentally altered how they operate. The industry is rapidly moving toward what insiders call “The Automated Deal Team.”

AI-Driven Deal Sourcing at 200x Human Speed

Sophisticated funds, including Andreessen Horowitz (which announced $15 billion in new capital this month), now deploy autonomous agents to scan GitHub commits, patent filings, academic papers, and niche social momentum. Some firms report their AI agents identify nearly 200 potential investment targets in the time it takes a junior analyst to find one.

What’s actually happening:

Agents continuously monitor technical forums, GitHub repositories, and research publications for breakthrough innovations

Pattern recognition identifies founding teams with specific technical profiles before companies formally raise capital

Social graph analysis maps relationships between successful founders and their former colleagues launching new ventures

Patent filing analysis reveals companies developing novel approaches before public announcements

This creates significant first-mover advantage for well-capitalized funds with sophisticated agent infrastructure, further concentrating deal flow at the top of the market. Smaller funds without agent capabilities increasingly compete on relationships rather than systematic deal discovery.

Due Diligence Agents Compress Timeline from Weeks to Minutes

The traditional due diligence process involved teams of analysts spending weeks reviewing virtual data rooms, financial projections, technical documentation, and legal contracts. In January 2026, agents summarize entire VDRs in minutes, flagging legal red flags, non-standard contract clauses, technical debt indicators, and financial anomalies that previously took extensive manual review.

Implications for founders:

Deal timelines compress dramatically, some AI rounds closing in days without formal pitch decks

Documentation quality becomes even more critical as agents flag inconsistencies humans might miss

Companies with clean, well-organized data rooms gain competitive advantage in compressed timelines

The bar for “investment-ready” documentation rises substantially as agents identify gaps instantly

[Insert IMAGE: AI Agent VC Workflow Diagram with alt text: “agentic AI venture capital due diligence workflow automation 2026”]

Agent Infrastructure Funding Booms

Funding for “Agent Infrastructure” tools that help other companies build autonomous agents is experiencing explosive growth. Concourse raised $12 million this month for its AI agent platform specifically designed for finance teams, representing just one example of the infrastructure layer enabling widespread agent adoption.

The meta-trend: We’re witnessing funding booms in three distinct layers: foundation models (xAI, OpenAI), agent infrastructure (Concourse and dozens of competitors), and vertical agent applications (thousands of startups building industry-specific autonomous systems). Each layer requires different capital profiles, development timelines, and risk characteristics.

For founders in the agent infrastructure layer, patient capital becomes essential. These companies often require 5-7 years to establish platform effects and ecosystem lock-in, timelines incompatible with traditional VC’s 5-7 year fund cycles demanding rapid exits.

Enterprise Consolidation: Higher Budgets, Fewer Winners

Here’s the paradox emerging in January 2026: enterprise AI budgets are increasing significantly, but fewer startups will capture that spending. After 2-3 years of experimentation, enterprises are consolidating their “AI vendor sprawl” and picking winners.

What’s driving enterprise consolidation:

Testing multiple tools for single use cases proved unsustainable

Difficulty discerning differentiation even during proof of concepts

Push to reduce SaaS sprawl and move toward unified systems

Demand for measurable ROI rather than experimental innovation

Concentration on tools that have delivered proven results

A Databricks Ventures vice president predicted 2026 as “the year that enterprises start consolidating their investments and picking winners.” Companies will cut experimentation budgets, rationalize overlapping tools, and deploy savings into AI technologies that have demonstrated actual value.

[Insert IMAGE: Enterprise AI Consolidation Diagram with alt text: “enterprise AI vendor consolidation 2026 showing budget concentration trends”]

The Moat Question Becomes Critical

Investors increasingly ask what makes an AI startup defensible. The answer centers on proprietary data and products that can’t be easily replicated by tech giants or large language model companies. Startups with products similar to offerings from AWS, Salesforce, or Microsoft see pilot projects and funding dry up rapidly.

This selectivity creates opportunity for companies that solve vertical-specific problems with proprietary data sets, exactly the type of business that often requires 7-12 year development timelines incompatible with traditional VC fund structures.

Mega-Fundraises Concentrate Market Power

Andreessen Horowitz announced a $15 billion fundraise in early January 2026, bringing their assets under management to over $90 billion. This single raise represents 18% of all venture capital dollars allocated in the United States during 2025.

Let that sink in: one firm raised nearly one-fifth of all US VC capital deployed the previous year.

The breakdown of a16z’s $15 billion raise:

$6.75 billion for growth investments

$1.7 billion each for apps and infrastructure

$1.176 billion for “American Dynamism”

$700 million for biotech and healthcare

$3 billion for other venture strategies

This concentration at the top creates fundamental market dynamics. Multistage firms with massive dry powder have competitive advantages in pursuing mega-rounds that close in days without decks or clear product plans. Smaller, specialized venture firms increasingly struggle to compete in markets dominated by platform players.

The firm’s mission, as stated by co-founder Ben Horowitz, is “ensuring that America wins the next 100 years of technology.” Whether that happens remains to be seen, but what’s certain is they’ve mastered raising money to fund a vision that runs through sovereign wealth funds, including at least one from Saudi Arabia.

The Shift From Growth At All Costs to Sustainable Economics

Perhaps the most fundamental shift in January 2026 is the market’s complete rejection of “growth at all costs” mentality. Companies reaching IPO today demonstrate sustainable business models with proven economics. This affects every stage of the funding pipeline.

Key characteristics of 2026 funding standards:

Actual revenue, not just user growth metrics

Proven unit economics, not path to eventual profitability

Clear competitive moats, not first-mover advantage claims

Defensible market positions, not total addressable market dreams

This shift particularly impacts the estimated 80% of companies excluded by traditional VC metrics that emphasize pure growth velocity over sustainable development. Companies building complex technology requiring patient capital face fundamental misalignment with fund structures optimized for 5-7 year exits.

The VC Risk Swap addresses this exact market failure by replacing equity investment with insurance-backed revenue guarantees, allowing founders to retain ownership while providing funders downside protection and optional future participation rights. Patient capital sources can now deploy into opportunities traditional VC structures systematically exclude.

Global Trends Reshape Capital Deployment Strategies

Beyond the US-centric AI boom, January 2026 witnessed three critical global developments that fundamentally alter how capital flows across borders and how success is measured.

Sovereign AI: Nations Deploy Patient Capital at Scale

“Sovereign AI” has emerged as a dominant investment thesis, with nations recognizing that AI infrastructure constitutes strategic national interest equivalent to energy independence or military capability. January 2026 saw major state-backed commitments:

Poland’s €350 million Future Tech Fund: Launched to develop localized large language models and compute infrastructure, ensuring Polish language and cultural context receive proper AI representation while building domestic technical capacity.

Quebec’s $500 million AI Commitment: Focused on maintaining Quebec’s position as AI research leader while commercializing academic breakthroughs through patient, government-backed capital that doesn’t demand compressed exit timelines.

Middle East AI Infrastructure Boom: The SuperReturn Saudi Arabia conference (January 26-27) highlighted how the Middle East is positioning as global “Lending and VC hub” specifically targeting AI infrastructure with multi-decade investment horizons.

Strategic implications: Sovereign AI funding operates on fundamentally different timelines than traditional VC. Governments measure success in decades, not fund cycles, creating natural alignment with companies requiring patient capital for complex technical development. This represents massive addressable market for alternative structures that can accommodate government co-investment.

[Insert IMAGE: Sovereign AI Investment Map with alt text: “sovereign AI government funding Europe Middle East Asia 2026 infrastructure investment”]

DPI Replaces IRR as Primary Success Metric

Limited Partners have fundamentally shifted success criteria in January 2026. The new mantra: “DPI is the New IRR.” DPI (Distributed to Paid-In Capital) measures actual cash returned to investors, not paper valuations that may never materialize.

Why this matters now:

After years of inflated private valuations that never converted to liquid exits, LPs demand proof of actual returns

Paper gains from 2021-era unicorns that never exited or exited at massive down-rounds destroyed LP confidence in mark-to-market reporting

The shift forces VCs toward M&A exits (like the Brex/Capital One deal) rather than waiting indefinitely for IPO markets to fully recover

Secondary markets ($160 billion in 2025) provide partial liquidity but at discounts to last-round valuations

Implications for alternative structures: The VC Risk Swap’s insurance-backed revenue guarantees create actual cash flows to funders throughout the development timeline rather than requiring exit events for returns. This DPI-focused environment makes structures with programmatic return of capital increasingly attractive compared to traditional equity’s all-or-nothing exit dependency.

EU AI Act Compliance Drives RegTech Funding Wave

With the EU AI Act requiring core compliance by August 2026, January witnessed a flurry of “Regulatory Tech” (RegTech) funding as startups scramble to build auditable, compliant AI systems that can operate in the world’s most stringent regulatory environment.

The compliance challenge:

High-risk AI systems require extensive documentation, testing, and ongoing monitoring

Companies must demonstrate transparency in training data, model decisions, and failure modes

Penalties for non-compliance reach €35 million or 7% of global revenue, whichever is higher

US companies wanting European market access must build compliance infrastructure

Investment opportunity: RegTech startups helping companies achieve EU AI Act compliance require 3-5 years to build comprehensive solutions, validate across multiple jurisdictions, and establish regulatory relationships. This patient capital profile doesn’t align with traditional VC’s compressed timelines, creating opportunity for alternative structures that accommodate longer development cycles.

The Indonesia PE-VC Summit (January 29) highlighted parallel regulatory development in Southeast Asia, with nations watching EU implementation closely while developing their own AI governance frameworks. Companies solving cross-border compliance will command premium valuations but require patient, flexible capital structures.

M&A and Secondary Markets Provide Alternative Exits

Global M&A volumes surged 40% year-over-year in Q3 2025, with eight deals exceeding $10 billion closing in that quarter alone. Private equity sponsors led the charge, with sponsor-backed M&A value up approximately 58% relative to Q3 2024.

Secondary transactions reached $160 billion, providing liquidity alternatives for founders unable or unwilling to pursue traditional IPO exits. Some key developments include:

Mega-deals return: $55 billion take-private of Electronic Arts, $18.3 billion acquisition of Hologic signal renewed appetite for large transactions

Investment banks reclaim position: Goldman Sachs reports record pipeline of 38 mega-deals exceeding $10 billion

Secondary markets mature: Still underpenetrated at approximately 2% of unicorn market value traded, but growing rapidly as liquidity normalizes

Pricing tightens: Favoring early movers and primary investors exploring exit optionality

These alternative exit pathways create opportunities for strategic acquisitions by corporate players seeking AI capabilities or market positions, particularly benefiting companies that solved vertical-specific problems but don’t fit IPO profiles.

The Reverse Acqui-Hire Phenomenon

Major tech companies increasingly recruit founding teams without acquiring companies, as seen with Microsoft, Google, and Meta in recent months. This creates scenarios where talent value exceeds company value, particularly relevant for AI infrastructure plays where human capital constitutes primary competitive advantage.

What January 2026 Means for Alternative Capital Structures

The market conditions emerging in January 2026 create unprecedented urgency for alternative funding structures. With traditional VC systematically excluding non-AI companies and demanding compressed exit timelines incompatible with complex product development, patient capital sources seek deployment mechanisms that traditional structures can’t accommodate.

The opportunity set breaks down into distinct categories:

Family offices: Seeking patient capital deployment with downside protection and participation optionality

High-net-worth angels: Wanting meaningful involvement without governance conflicts that equity investment creates

Corporate strategics: Needing option value on emerging technologies without commitment to full acquisitions

Institutional allocators: Seeking portfolio diversification beyond traditional VC’s concentrated risk profile

The estimated $290 billion in patient capital currently excluded by structural incompatibilities represents addressable market for properly designed alternative structures. The VC Risk Swap specifically targets this opportunity by providing insurance-backed revenue guarantees that replace equity dilution while offering funders downside protection traditional debt can’t match.

Looking Forward: What Comes Next

As 2026 progresses, expect continued bifurcation between AI and non-AI funding environments, but with several new dimensions emerging from January’s developments.

Predictions for Remainder of 2026

IPO activity remains strong but highly selective: Focus continues on profitable companies with proven models, but expect Physical AI and Vertical AI companies to dominate largest public debuts.

Agentic AI funding accelerates: Beyond foundation models, expect explosive growth in agent infrastructure and vertical agent applications across every industry.

Sovereign AI investments compound: More nations announce multi-hundred-million commitments as AI infrastructure becomes recognized national security priority.

DPI pressure forces creative exits: Expect more structured M&A deals, secondary transactions, and alternative liquidity mechanisms as GPs face LP demands for actual cash returns.

RegTech becomes essential infrastructure: EU AI Act compliance deadline (August 2026) drives mandatory spending on auditable, transparent AI systems.

Alternative structures gain mainstream acceptance: As traditional VC systematically excludes more opportunities, patient capital sources demand structures accommodating longer timelines, and the VC Risk Swap demonstrates viability at scale.

Physical AI commands growing capital share: Autonomous systems in trucking, robotics, manufacturing, and logistics require longer development cycles but produce more defensible moats than pure software.

Non-AI companies increasingly turn to alternatives: As traditional VC becomes inaccessible for validated companies outside AI infrastructure, alternative funding structures transition from experimental to essential.

The founders who succeed won’t be those who chase trends, but those who understand their businesses require patient capital and structure accordingly from inception. The six-figure professional implementation cost for properly designed alternative structures remains trivial compared to value preservation through appropriate capital structure planning.

The Bottom Line: Structure Matters More Than Ever

January 2026 has proven that capital structure decisions made at inception determine which opportunities remain viable as markets bifurcate along multiple dimensions: AI versus non-AI, agentic systems versus traditional software, vertical applications versus horizontal platforms, and patient capital versus compressed exit timelines.

The companies that designed for patient capital now have options:

Waabi’s milestone-based $1 billion structure demonstrates sophisticated investors accepting performance-validated capital deployment

Brex’s patient path to $5.15 billion acquisition proves that resisting premature exit pressure creates superior outcomes

OpenEvidence’s vertical focus on healthcare shows that 7-12 year development timelines build defensible $12 billion valuations

Sovereign AI investments prove that patient, decade-scale capital exists for strategic infrastructure development

Those that assumed traditional VC would always be available face bleaker choices:

Non-AI companies finding institutional investors show “zero interest” regardless of fundamentals

Companies requiring multi-year development discovering growth capital unavailable at any valuation

Founders facing down-rounds or liquidation because they raised at 2021 peaks without building toward profitability

Startups unable to compress timelines to match VC fund cycles demanding 5-7 year exits

The market has spoken clearly: it’s not just about having a great product or even great traction. It’s about matching capital structure to business reality, investor expectations to development timelines, governance models to founder capabilities, and return mechanisms to capital patience.

January 2026’s Three Critical Lessons:

First, agentic AI has become the dividing line. Companies building autonomous systems that perform specialized labor command premium valuations and patient capital. Companies building traditional software increasingly face “build it yourself” competition from enterprises using AI coding assistants.

Second, DPI pressure forces creative thinking. Limited partners demanding actual cash returns rather than paper valuations create urgent need for structures that return capital programmatically throughout development rather than requiring exit events. The VC Risk Swap’s insurance-backed revenue guarantees address this precisely.

Third, global capital operates on different timelines. Sovereign AI investments, government co-funding, and strategic corporate partnerships all accommodate longer development cycles than traditional VC. Structures that can accept these patient capital sources gain massive competitive advantage.

For the 80% of fundable companies systematically excluded by traditional VC’s structural limitations, January 2026 represents inflection point. Alternative structures are no longer experimental, they’re essential. The founders who recognized this early, designed appropriate structures from inception, and attracted patient capital aligned with their actual timelines will dominate the next decade.

The six-figure professional implementation cost remains the best investment a founder can make, because the alternative, attempting to retrofit structures after raising traditional VC or facing valuation deadlock with no good options, costs exponentially more in dilution, control, and ultimately, company value.

© 2026 YBAWS! All rights reserved.

👤 ABOUT THE AUTHOR

Sean Cavanagh, BAS, CPA, CA, CF, CBV

With over three decades negotiating business acquisitions and conducting valuations, Sean brings unique perspective from 16 years at Canada Revenue Agency followed by equal time developing complex tax structures. Founder of SaferWealth.com and creator of the VC Risk Swap alternative funding structure, Sean delivers unvarnished analysis of capital markets and funding alternatives. His approach combines CRA insider knowledge with AI-powered research to create structures designed for regulatory defensibility from inception.

📚 DO YOUR OWN RESEARCH

The market analysis in this article draws from multiple authoritative sources for a complete list, contact saferwealth.com. Consult professionals before making funding structure decisions. Market conditions change rapidly, particularly in AI-focused sectors where valuations and competitive dynamics shift monthly.