Is Your VC Even a VC Anymore!?

Non-AI venture capital quietly stopped funding risk. It now waits for proof, then still demands the equity, the board seat, and control. Here is the bargain that broke, and the fix.

Somewhere between 2021 and now, your friendly neighbourhood venture capitalist stopped venturing. Today they want customers, revenue, and receipts before they will risk a nickel, then still demand the equity, the board seat, and the keys to your company. That is not venture capital. That is a landlord with a pitch deck.

The Day Venture Capital Stopped Venturing

Venture capital used to mean something gloriously reckless. An investor looked at a founder, a whiteboard, and a prayer, and wrote a cheque against pure uncertainty, betting that one moonshot in ten would pay for the other nine craters. That was the deal: big risk, big patience, big upside. For non-AI startups in 2026, that investor has quietly left the building.

What replaced them looks similar and behaves nothing alike. Today’s non-AI venture capitalist would like to see customers first. And revenue. And retention curves, signed contracts, a repeatable sales motion, ideally a grant or two and some debt you have already arranged yourself. In plain terms, they would like you to remove the risk before they invest in the risk. The share of sub-$5 million rounds fell to a decade low in 2025, because the small, early, faith-based cheque is precisely the one that went extinct.

This is not venturing. It is acceleration wearing a venture costume. The money now arrives after the dangerous part, which makes it closer to growth equity in a hoodie than the wild capital of legend. With AI hoovering up 65 percent of all deal value, the patience and risk appetite that once flowed to everyone now flow to one room, and you are not in it.

The cruel twist is that real venture capital, the reckless, risk-loving kind, still exists. It just emigrated to AI. Frontier model startups raise enormous sums on little more than a thesis and a famous founder, the exact bet-on-the-future behaviour non-AI founders are scolded for as naive. So venturing did not die. It moved, took the good weather with it, and left everyone else a polite note about checking back once they have traction.

The Bargain That Quietly Broke

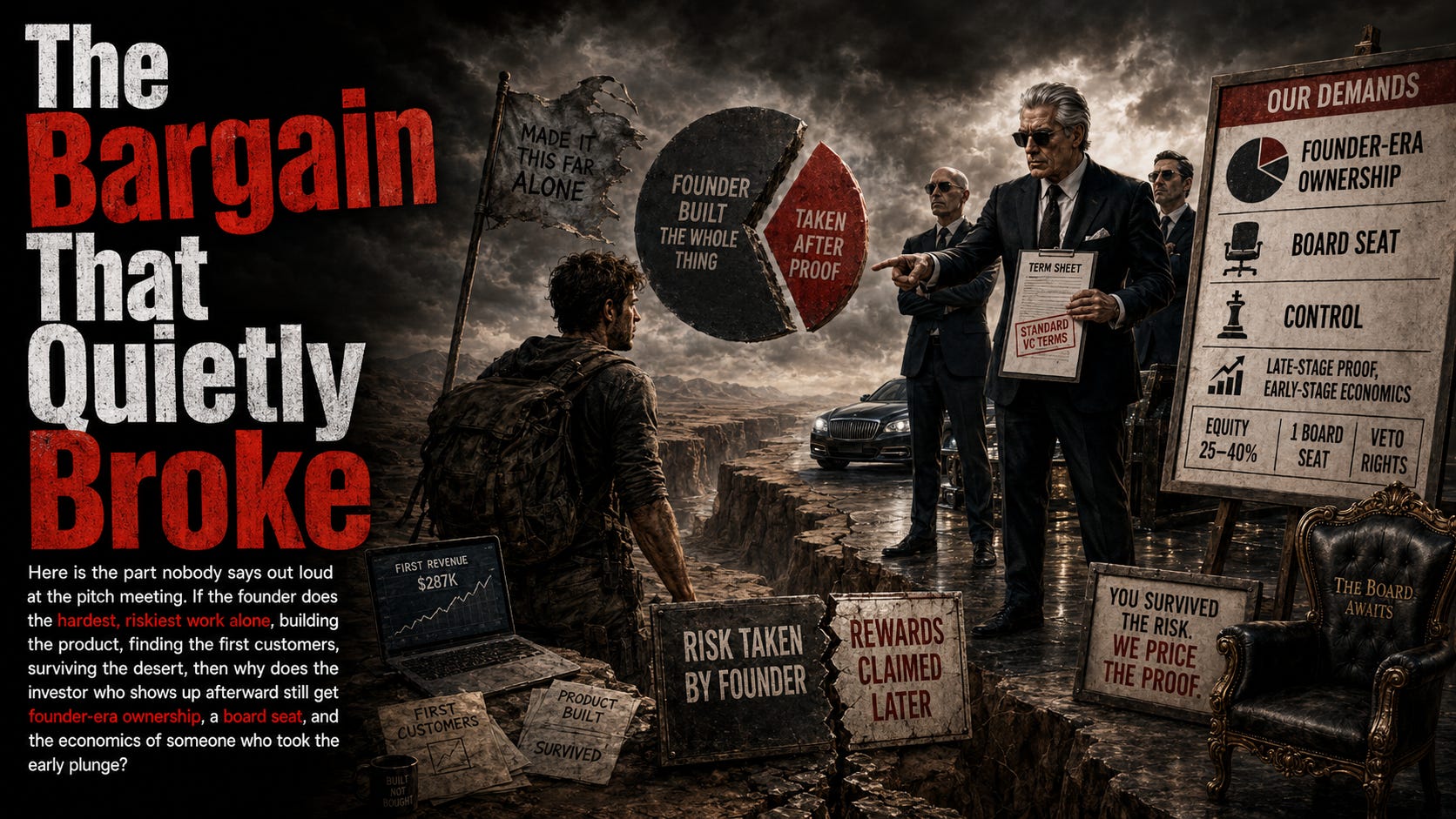

Here is the part nobody says out loud at the pitch meeting. If the founder does the hardest, riskiest work alone, building the product, finding the first customers, surviving the desert, then why does the investor who shows up afterward still get founder-era ownership, a board seat, and the economics of someone who took the early plunge?

That is the broken bargain. The old trade was simple and almost fair. The VC took terrifying risk, so the VC earned outsized reward and a seat at the table. Strip the terror out of the equation and the reward structure stops making sense. Yet the term sheet never got the memo. It still asks for the same slice, the same control, the same protections, as though it were 1975 and the founder had nothing but a hunch and a haircut.

For non-AI companies the asymmetry is brutal. You arrive having de-risked the business with your own sweat, savings, customers, and grants, and you are handed a deal priced as though you walked in empty-handed. You did the venturing. They want the venture economics. It is like paying full price for a house you already renovated.

Give it an honest name and the discomfort sharpens. Money that shows up only after the proof is not venture capital, it is late growth capital cosplaying as a pioneer. Growth capital is a fine thing. The trouble is the pricing. Growth-stage risk should command growth-stage terms, not the ownership and control owed to a first believer. The non-AI founder gets sold seed-era dilution for late-stage safety, the worst trade on the menu, and grins through it because the alternative is no cheque at all.

Control Is the New Price

Founders love to fixate on valuation, the one big number on the front page. In 2026, that is the wrong thing to watch. As any honest advisor will tell you, economics and control clauses matter far more than the headline valuation. And while the economics have actually gotten politer, the control absolutely has not.

The numbers give the game away. By one Cooley analysis, 98 percent of recent venture rounds used a founder-friendly 1x non-participating preference, which sounds like a gift, until you read the next line and learn that investor veto rights still appeared in more than 90 percent of deals. They handed back the wallet and quietly kept the steering wheel. Meanwhile full ratchet anti-dilution, all but extinct in 2021, has crept back into 2024 to 2026 term sheets, surfacing exactly where founders have the least room to say no.

And the non-AI founder has the least room of anyone. In a two-market world you are often the only non-AI deal in the building, with no rival bid to wave around. Control follows leverage the way water follows downhill. When you cannot credibly threaten to walk, you sign the board seat, the veto, the protective provisions, and you call it a partnership. In Canada the squeeze runs sharper still, where capital is thinner and investor protections tend to creep higher. The result is a founder who built the whole company, then has to raise a hand for permission to run it.

And vetoes are not abstract paperwork. A protective provision can mean you need an investor’s blessing to hire a senior leader, to sign a transformative partnership, to raise your next round, or to sell the company you started. One reluctant board member can stall the very decisions that keep a non-AI business breathing in a slow market. You did not take on a partner. You took on a permission slip, and it does not expire when the cheque clears.

Why The VC Risk Swap Hands You Back the Keys

This is where the VC Risk Swap does something the modern term sheet flatly refuses to: it funds you without governing you. There is no board seat to surrender, no veto to grant, no investor sitting in judgment of every hire. The Swap replaces the priced equity round with a milestone-based revenue guarantee, backstopped by company-owned coverage for business continuity, so the funder is protected without owning a single vote. You keep your equity and your control straight through commercialization. Capital that behaves like capital, not a quiet coup.

Subscribe to SaferWealth for more field notes from the part of the funding world that does not get a parade, plus the structures that let you keep both your company and the captain’s chair.

Questions about your specific situation? Reach out directly at riskswap@saferwealth.com.

CONNECT WITH SAFERWEALTH

Expand your learning beyond this post:

1. Web: SaferWealth.com, alternative startup funding structures.

2. YouTube: The Capital ToolKit, funding strategy and structure breakdowns.

3. Rumble: @SaferWealth.

4. Contact: riskswap@saferwealth.com.

ABOUT THE AUTHOR

Sean Cavanagh (BAS, CPA, CA, CF, CBV) is the founder of SaferWealth and creator of the VC Risk Swap, an alternative startup funding structure that preserves founder equity and control through milestone-based, downside-protected capital. With over three decades in business valuation, M&A advisory, and structuring, Sean writes about funding the businesses the venture market overlooks.

DO YOUR OWN RESEARCH

Sources referenced in this post:

• NVCA 2026 Yearbook, United States venture totals and AI concentration.

• citybiz coverage of the 2026 Yearbook, AI share of 2025 deal value.

• Venture capital statistics, 2026, sub-$5 million round share at a decade low.

• GoingVC on term sheet provisions, Cooley data on liquidation preferences and veto rights.

• VC Beast, anatomy of a 2026 term sheet, anti-dilution and board control trends.

• PitchGrade term sheet guide, why economics and control outweigh valuation.

• CVCA market reports, Canadian venture trends and investor protections.

📖 RELATED READING

• VC Beast: Anatomy of a Venture Capital Term Sheet in 2026: what the modern term sheet really takes from founders.

• GoingVC: Term Sheet Provisions That Matter: where control hides after the economics look fair.

• CVCA Market Reports: the Canadian view, where leverage is thinner and terms are tougher.

Educational disclaimer: This content is for educational purposes only and does not constitute legal, tax, financial, or investment advice. The VC Risk Swap is a sophisticated structure that must be implemented with independent professional advisors for your specific situation. All examples are illustrative. Neither the author nor SaferWealth accepts liability for actions based on this content. This material supplements but never replaces proper professional consultation and judgment.

© 2026 SaferWealth. All rights re