Limited Partners Are Forcing VC Structure Innovation

The shift from paper valuations to actual cash returns creates $290 billion alternative funding opportunity for patient capital structures

Limited partners have fundamentally changed the venture capital success metric. “DPI is the new IRR” means LPs demand actual cash returned to investors, not paper valuations that may never convert to liquid exits. This forces VCs toward alternative structures that return capital programmatically rather than requiring exit events, creating unprecedented opportunity for properly designed patient capital deployment.

10 KEY TAKEAWAYS - THE DPI REVOLUTION

DPI replaces IRR as success metric: Distributed to Paid-In Capital measures actual cash returned, ending reliance on mark-to-market paper gains that never materialized.

2021 unicorns destroyed LP confidence: Inflated private valuations that exited at massive down-rounds or never exited created LP skepticism of reported performance.

GPs face unprecedented pressure: General partners must deliver actual liquidity rather than promising eventual exits that fund timelines can no longer accommodate.

M&A accelerates as primary exit: Brex’s $5.15 billion acquisition exemplifies VCs pushing strategic sales rather than waiting for IPO markets to fully recover.

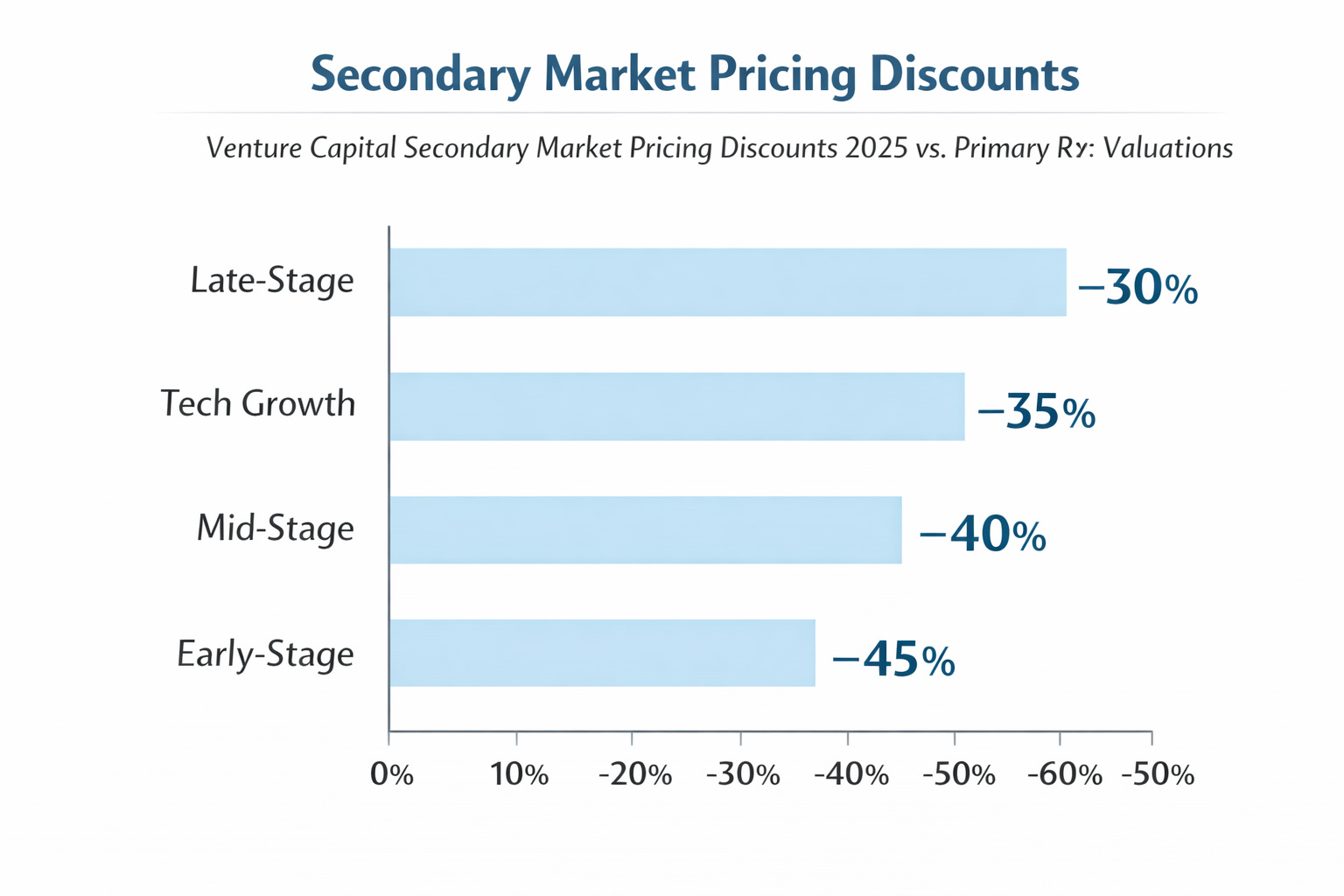

Secondary markets provide partial relief: $160 billion in 2025 secondary transactions offer liquidity but at significant discounts to last-round valuations.

Fund cycle compression intensifies: LPs demanding faster DPI force VCs toward shorter holding periods, further misaligning with companies requiring patient capital.

Alternative structures gain mainstream acceptance: Revenue guarantee mechanisms that return capital throughout development rather than requiring exits address LP liquidity demands.

Insurance-backed structures emerge: Downside protection through insurance enables patient capital deployment while providing LPs comfort on capital preservation.

Portfolio construction shifts dramatically: VCs increasingly avoid long-cycle opportunities regardless of quality, because LP pressure demands portfolio liquidity concentration.

Patient capital sources seek new mechanisms: Family offices, high-net-worth individuals, and sovereign wealth funds want structures accommodating longer timelines traditional VC can’t provide.

📚 READING PREREQUISITES

Understanding the DPI revolution requires familiarity with venture capital fund economics, LP-GP relationships, and how fund performance gets measured. The shift from IRR to DPI represents fundamental change in how capital gets allocated across the entire ecosystem.

Recommended Prior Reading:

Understanding VC Fund Economics and LP Relationships

Why IRR Became Meaningless in 2020s Venture Capital

The Liquidity Crisis in Venture Capital 2022-2025

What DPI Actually Measures and Why It Matters Now

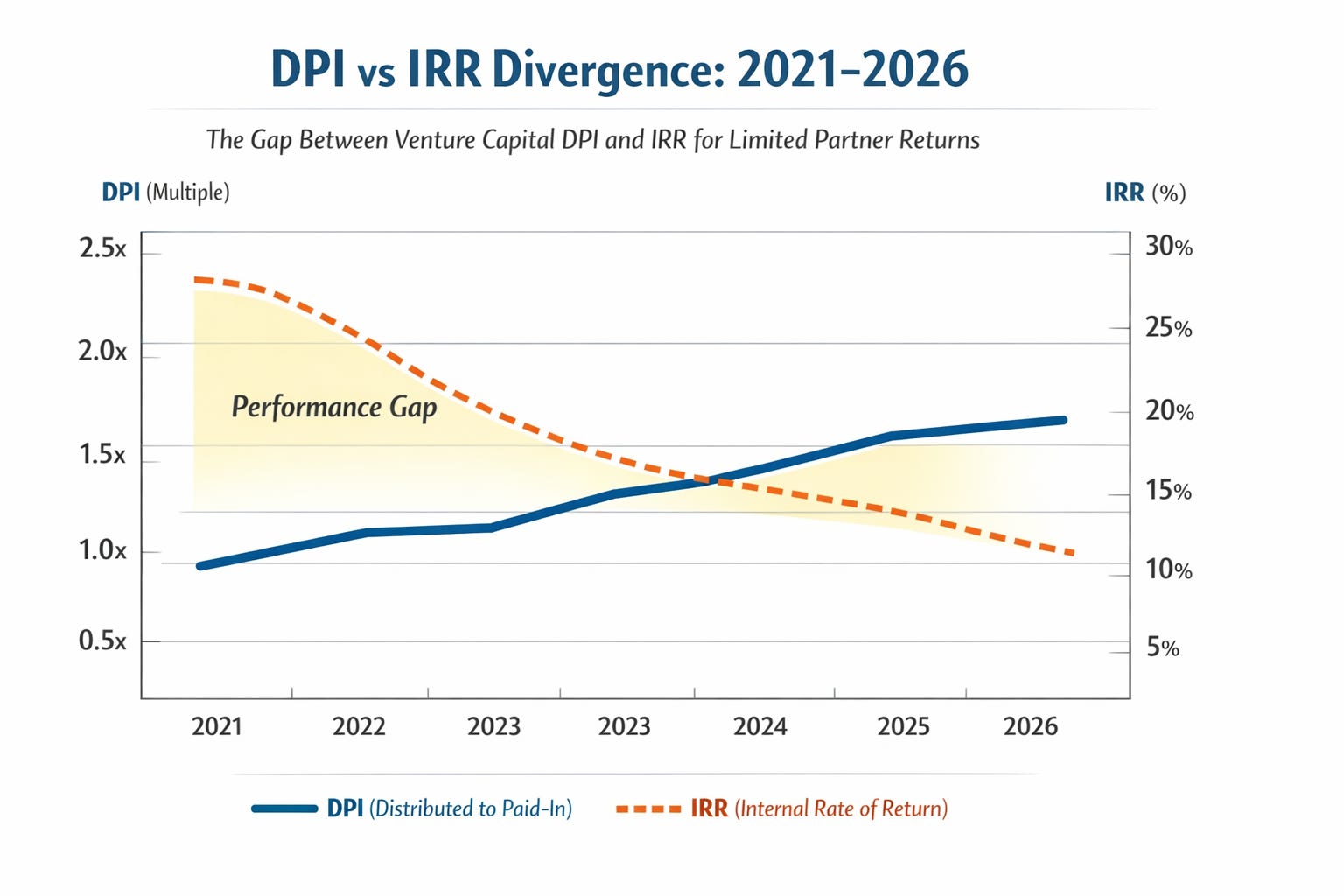

DPI (Distributed to Paid-In Capital) calculates actual cash returned to limited partners divided by the capital they invested. A DPI of 2.0x means LPs received $2 for every $1 invested, regardless of how long it took or what the intermediate paper valuations showed.

Contrast this with IRR (Internal Rate of Return), which measures annualized return rate including unrealized paper gains from mark-to-market valuations of portfolio companies. A fund holding unicorns valued at $1 billion each shows spectacular IRR even if those companies never exit or ultimately exit at far lower valuations.

The critical difference:

IRR can look fantastic based on paper valuations that never materialize

DPI only measures actual cash that LPs can spend, reinvest, or distribute to their stakeholders

IRR rewards fast markups regardless of exit reality

DPI rewards actual liquidity regardless of how long it took

Why January 2026 Marks the Inflection Point

After four years of liquidity drought (2022-2025), limited partners have lost patience with promises of eventual exits. The 2021-era unicorns that raised at peak valuations created unprecedented disconnect between reported fund performance (high IRR based on markups) and actual returns (low or zero DPI because companies can’t exit at those valuations).

The numbers tell a brutal story:

Hundreds of “unicorns” raised at $1+ billion valuations in 2021

Most have been unable to exit via IPO or strategic acquisition at those prices

Many face down-rounds or have stagnated waiting for market conditions to improve

LPs who invested in 2018-2020 vintage funds still haven’t received distributions

Meanwhile, inflation eroded the real value of whatever eventual returns might materialize

January 2026’s market developments, particularly the selective IPO reopening and M&A acceleration, create first meaningful DPI opportunities in years. But LPs now demand structural changes ensuring future portfolios generate actual liquidity rather than paper valuations.

How DPI Pressure Changes VC Behavior

The shift from IRR to DPI as primary success metric fundamentally alters how venture capitalists construct portfolios, evaluate opportunities, and structure deals.

Avoiding Long-Cycle Opportunities Regardless of Quality

VCs increasingly pass on exceptional opportunities that require 7-12 year development timelines, not because the opportunities lack merit, but because LP pressure demands portfolio liquidity. This creates systematic market failure where high-quality companies requiring patient capital can’t access traditional VC regardless of fundamentals.

The vicious cycle:

LPs demand DPI, forcing GPs toward shorter-cycle investments

GPs pass on long-cycle opportunities to avoid LP criticism

Long-cycle companies can’t access traditional VC funding

Remaining patient capital sources lack structures to deploy effectively

Market failure creates $290 billion alternative funding gap

This explains why non-AI companies with validated products, proven market demand, and sustainable economics still can’t raise traditional VC. It’s not that they’re bad investments, it’s that they don’t fit fund timelines driven by LP liquidity demands.

Pushing Portfolio Companies Toward Premature Exits

VCs facing DPI pressure increasingly push portfolio companies toward strategic acquisitions even when longer independent development would create more value. The Brex acquisition by Capital One, while representing fantastic outcome, exemplifies this dynamic.

The founder’s dilemma:

Strategic acquirer offers $5 billion today

Continuing independent development might create $15 billion company in 5-7 years

But VCs need liquidity now to satisfy LP demands

Board pressure intensifies toward accepting premature exit

Founder forced to choose between personal vision and investor relationships

The VC Risk Swap structure eliminates this pressure because it generates programmatic cash flows to funders throughout development rather than requiring exit event for returns. Funders get DPI from revenue guarantees while founders retain option to pursue optimal long-term strategy.

Increasing Reliance on Secondary Markets

The $160 billion in secondary transactions during 2025 provided some relief valve, allowing VCs to generate DPI by selling positions to other investors rather than waiting for company exits. But secondary pricing typically occurs at substantial discounts to last-round valuations, destroying returns.

Secondary market dynamics in DPI-focused environment:

Sellers (VCs needing DPI) accept discounts to generate liquidity

Buyers (patient capital sources) acquire positions at attractive valuations

Companies suffer reputation damage from down-round secondary sales

Founders see cap tables churn with investors who weren’t there at inception

Long-term patient capital gets rewarded while short-term capital exits at loss

This creates opportunity for alternative structures that attract patient capital sources from inception, avoiding secondary market discounts while providing founders with committed, long-term partners aligned with actual business timelines.

The Capital One-Brex Deal as Case Study

Capital One’s $5.15 billion acquisition of Brex on January 22, 2026 represents the largest bank-fintech deal in history and exemplifies how DPI pressure reshapes exit decisions.

Why This Deal Happened Now

Brex raised substantial capital during 2021-2022 at valuations reportedly approaching $12+ billion. The company built exceptional expense management and corporate card platform with real revenue, strong unit economics, and defensible market position. But several factors aligned to make $5.15 billion acquisition attractive despite being well below peak private valuation:

From Capital One’s perspective:

AI-native fintech stack they couldn’t build internally in relevant timeframe

Proven technology serving exactly the SMB and mid-market segments Capital One targets

Strategic imperative to compete with AI-powered competitors

Ability to deploy Brex technology across entire Capital One customer base

Willingness to pay premium for speed-to-market and talent acquisition

From Brex investors’ perspective:

Clear exit providing actual DPI after years of waiting

Valuation, while below peak, still represents strong multiple on actual revenue

Certainty versus continuing independent path with uncertain IPO timing

Capital One integration provides portfolio company exit precedent for other holdings

LP pressure to generate distributions making bird-in-hand attractive

From Brex founders’ perspective:

Opportunity to impact massive customer base through Capital One distribution

Liquidity for team and early employees after multi-year journey

Board and investor pressure toward accepting premium strategic offer

Recognition that independent IPO might require more years of waiting

The deal validates patient capital structures that don’t force premature exits. Had Brex been funded through VC Risk Swap mechanisms, founders could have waited for higher valuation or pursued independent path without investor pressure demanding liquidity.

What This Signals for M&A Market

The Brex acquisition signals that strategic acquirers recognize they must buy AI-native capabilities they can’t build internally. This creates robust M&A exit environment for companies that built defensible positions, even if valuations haven’t reached 2021 peaks.

Implications for alternative funding structures:

Patient capital enabling longer development cycles produces more valuable strategic acquisition targets

Revenue-generating companies with proven economics command premium strategic valuations

Founders who retained control through non-dilutive structures negotiate from strength

Insurance-backed structures providing downside protection enable patient capital deployment into potential strategic acquisition targets

Alternative Structures That Generate DPI Without Requiring Exits

The DPI revolution creates urgent need for funding mechanisms that return capital to investors throughout company development rather than requiring exit events for liquidity.

Revenue Guarantee Structures

For early stage companies, the VC Risk Swap generates DPI through insurance-backed revenue guarantees tied to company performance:

How it creates DPI for funders:

Company achieves revenue milestones verified by third parties

Guaranteed revenue stream flows to funders based on achievement

Insurance backs downside protection if company fails to perform

Funders receive programmatic cash returns throughout development cycle

No exit event required for funder to achieve positive DPI

How it benefits founders:

Retain 100% equity ownership and governance control

No board seats or investor veto rights constraining strategy

Timeline flexibility to pursue optimal long-term development

No pressure toward premature exits to satisfy investor liquidity needs

Optional participation rights give funders upside if company exceeds projections

This structure directly addresses LP demands for DPI while providing founders patient capital aligned with actual business requirements. The insurance component satisfies LP concerns about capital preservation, while revenue guarantees create programmatic distributions eliminating exit dependency.

The structure evolves with the development of the company.

Milestone-Based Capital Deployment

Waabi’s $1 billion funding included “milestone-based” components that likely create similar dynamics:

Capital releases as company achieves technical or commercial milestones

Risk reduction through validated performance before additional deployment

Timeline flexibility accommodating regulatory or technical delays

Governance alignment around achievement rather than ownership transfer

Partial DPI potential as early milestones generate returns before full exit

These structures recognize that complex businesses de-risk over time, and sophisticated capital wants structures reflecting that reality rather than all-or-nothing exit dependency.

Hybrid Structures Combining Multiple Mechanisms

The most sophisticated alternative structures combine multiple mechanisms addressing different stakeholder needs:

For early-stage technical risk:

Government grants or R&D funding non-dilutively

Convertible instruments that delay valuation until de-risking occurs

Milestone-based tranches released upon technical validation

For growth-stage commercial risk:

Revenue guarantees backed by insurance once product-market fit proven

Strategic partnerships providing deployment infrastructure

Debt instruments secured by revenue streams or assets

For exit optionality:

Participation rights giving funders upside in exceptional outcomes

Multiple exit pathways including strategic acquisition, licensing, IPO, or dividend capacity

Structures accommodating decade-long holding periods if optimal for value creation

The key insight: sophisticated capital recognizes that different risk profiles require different return mechanisms, and bundling everything into traditional equity optimizes for neither party.

The $290 Billion Patient Capital Opportunity

DPI pressure on traditional VC creates unprecedented opportunity for patient capital sources that can deploy through properly structured alternative mechanisms.

Who Has Patient Capital Seeking Better Structures

Family offices: Multigenerational wealth with no forced distribution timelines, seeking meaningful involvement in building valuable companies while protecting capital

High-net-worth angels: Successful entrepreneurs or executives wanting to deploy capital with longer horizons than traditional VC funds provide

Sovereign wealth funds: Nations deploying strategic capital with decade-plus timelines and willingness to accept lower returns for strategic benefits

Corporate strategics: Large companies wanting option value on emerging technologies without committing to full acquisitions immediately

Institutional allocators seeking diversification: Endowments, foundations, and pension funds with long-term mandates wanting exposure beyond traditional VC concentration

What They Want That Traditional VC Can’t Provide

Downside protection: Insurance-backed mechanisms limiting loss exposure while maintaining upside participation potential

Programmatic DPI: Cash flows throughout development cycle rather than exit dependency creating decade-long capital lockups

Governance flexibility: Involvement and oversight without board seats and veto rights that create adversarial dynamics

Timeline alignment: Structures accommodating 10-15 year development cycles for complex businesses rather than 5-7 year fund pressures

Tax efficiency: Structures optimizing for their specific tax circumstances rather than one-size-fits-all equity ownership

Strategic benefits: Beyond financial returns, access to technologies, relationships, insights, or capabilities advancing their core missions

The VC Risk Swap addresses all these requirements through insurance-backed revenue guarantees, optional participation rights, and flexible governance that traditional equity investment can’t match.

What This Means for Founders

If you’re building a company requiring patient capital with multi-year development timelines, the DPI revolution creates both challenge and opportunity.

The challenge: Traditional VCs increasingly avoid long-cycle opportunities regardless of quality because LP pressure demands portfolio liquidity within fund timelines.

The opportunity: Massive patient capital pools seek deployment mechanisms that traditional VC structures can’t provide, creating unprecedented demand for properly designed alternatives.

Action steps for founders:

Assess your actual timeline honestly: If your business requires 7-12 years to achieve meaningful scale, acknowledge this from inception rather than pretending you’ll exit in 5 years.

Structure appropriately from day one: The six-figure professional cost to implement proper alternative structures is trivial compared to value destruction from structural misalignment later.

Target patient capital sources directly: Don’t waste time pitching traditional VCs if your timeline doesn’t fit their fund cycles. Instead, pursue family offices, strategics, and sovereign capital that can accommodate your requirements.

Emphasize DPI generation: Show patient capital sources how your revenue model generates programmatic returns throughout development, addressing their need for DPI without requiring exits.

Retain control and optionality: Non-dilutive structures preserving founder ownership and governance control create massive long-term value that equity dilution destroys irreversibly.

⚠️ IMPORTANT DISCLAIMER

This content is for educational purposes only and does not constitute legal, tax, or financial advice. Alternative funding structures require comprehensive professional implementation including tax counsel, business valuators, commercial lawyers, insurance specialists, and financial advisors.

The VC Risk Swap structure mentioned requires costs typically exceeding six figures. Attempting simplified versions destroys legal defensibility. Every funding situation requires independent analysis specific to company circumstances, funder requirements, and regulatory environment.

Consult qualified advisors for your specific situation. Neither the author nor YBAWS! accepts liability for actions based on this content.

YBAWS! (Your Business Ain’t Worth Sh*t!) is a trademark and educational platform dedicated to helping business owners understand corporate value and marketability.

© 2026 YBAWS! All rights reserved.

📚 RELATED READING

Expand your understanding of DPI dynamics and alternative structures:

Cambridge Associates LP Performance Analysis: Institutional research on venture capital returns and DPI metrics

Preqin Alternative Assets Data: Comprehensive data on LP expectations and GP performance metrics

ILPA Guidelines on Fund Terms: Limited partner association guidance on fund structure and performance measurement

CONNECT WITH SAFERWEALTH

Expand Your Learning Beyond This Post:

Web: SaferWealth.com - Alternative Startup Funding Structures

Video: SaferWealth Posts - VC Risk Swap Educational Content

LinkedIn: LinkedIn @SaferWealth - Patient Capital Innovation

Rumble: @saferwealth - DPI analysis and alternative structures

Instagram: @saferwealth - Quick insights and updates

👤 ABOUT THE AUTHOR

Sean Cavanagh, BAS, CPA, CA, CF, CBV

With over three decades negotiating business acquisitions and conducting valuations, Sean brings unique perspective from 16 years at Canada Revenue Agency followed by equal time developing complex tax structures. Founder of SaferWealth.com and creator of the VC Risk Swap alternative funding structure addressing the LP liquidity crisis.

Connect with Sean:

📚 DO YOUR OWN RESEARCH

DPI analysis draws from:

Capital One acquisition of Brex $5.15 billion (January 22, 2026)

Industry reports on LP expectations and DPI requirements (2025-2026)

Secondary market transaction data ($160 billion in 2025)

Venture capital fund performance analysis across 2018-2024 vintages

Limited partner surveys on satisfaction with GP performance and liquidity

Alternative investment structure case studies and performance data

Verify all information with current market data and consult professionals before making funding structure decisions.