Background: MapleTech Manufacturing, a $12M revenue precision parts manufacturer in Ontario, had spent 18 months courting acquisition by their largest U.S. competitor, MetalCorp Industries. The CEO, Don Cherry, was convinced this made perfect strategic sense. “They know our customers, they understand our processes, and they have distribution we could never build,” he reasoned.

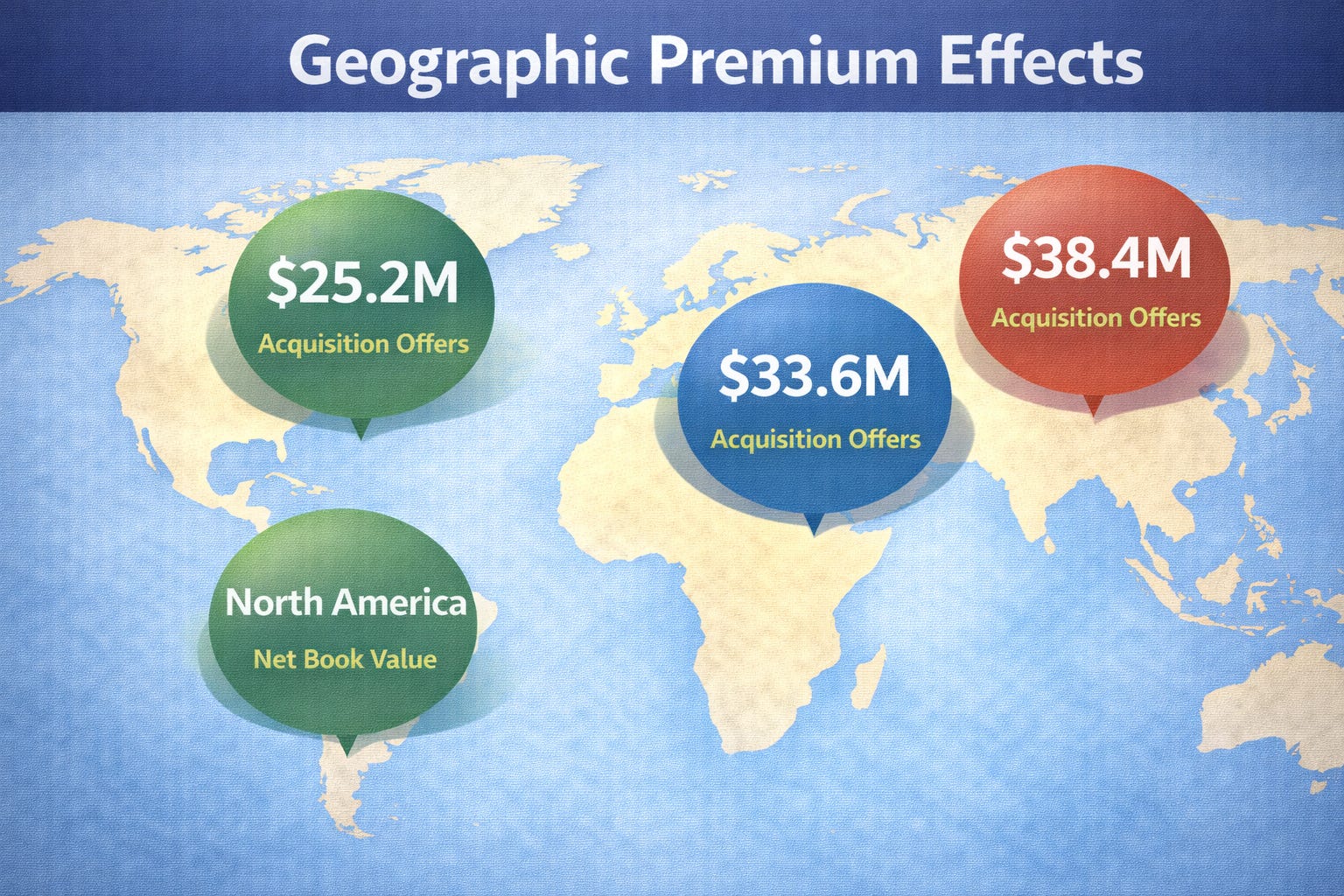

The Restricted Approach: Cherry’s advisors prepared a confidential information memorandum exclusively for MetalCorp, highlighting operational synergies and cost elimination opportunities. MetalCorp’s initial offer valued MapleTech at 2.1x revenue ($25.2M), emphasizing their plan to consolidate production, eliminate duplicate overhead, and leverage existing customer relationships.

Opening the Borders: Before accepting, Cherry’s M&A advisor convinced him to test the broader market. The expanded process revealed:

German automotive supplier seeking North American manufacturing footprint: offered 2.8x revenue ($33.6M)

Japanese precision equipment manufacturer valuing MapleTech’s aerospace certifications: offered 3.2x revenue ($38.4M)

Private equity fund focused on industrial roll-ups: offered 2.9x revenue ($34.8M) with earnout potential

The Outcome: The Japanese buyer ultimately paid $38.4M, a $13.2M premium over the original “logical” deal. The key difference: MetalCorp valued what they could eliminate, while the Japanese buyer valued what they couldn’t build domestically, specifically MapleTech’s AS9100 aerospace quality certification and CUSMA manufacturing advantages.

Lesson Applied: Cherry’s decision to open borders revealed that the same business had radically different strategic values to different buyer universes. Geographic and regulatory advantages invisible to domestic buyers became premium-worthy assets to international acquirers operating under different constraints and opportunities.

Case Study 2: DataStream Solutions - The PE Leverage Effect

Background: DataStream Solutions, a $8M ARR SaaS platform for healthcare data analytics, received an acquisition approach from HealthTech Corp, a strategic buyer offering $40M (5x ARR multiple). Founder Lisa Simpson was ready to accept, viewing it as validation of six years building the platform.