Case Study 1:

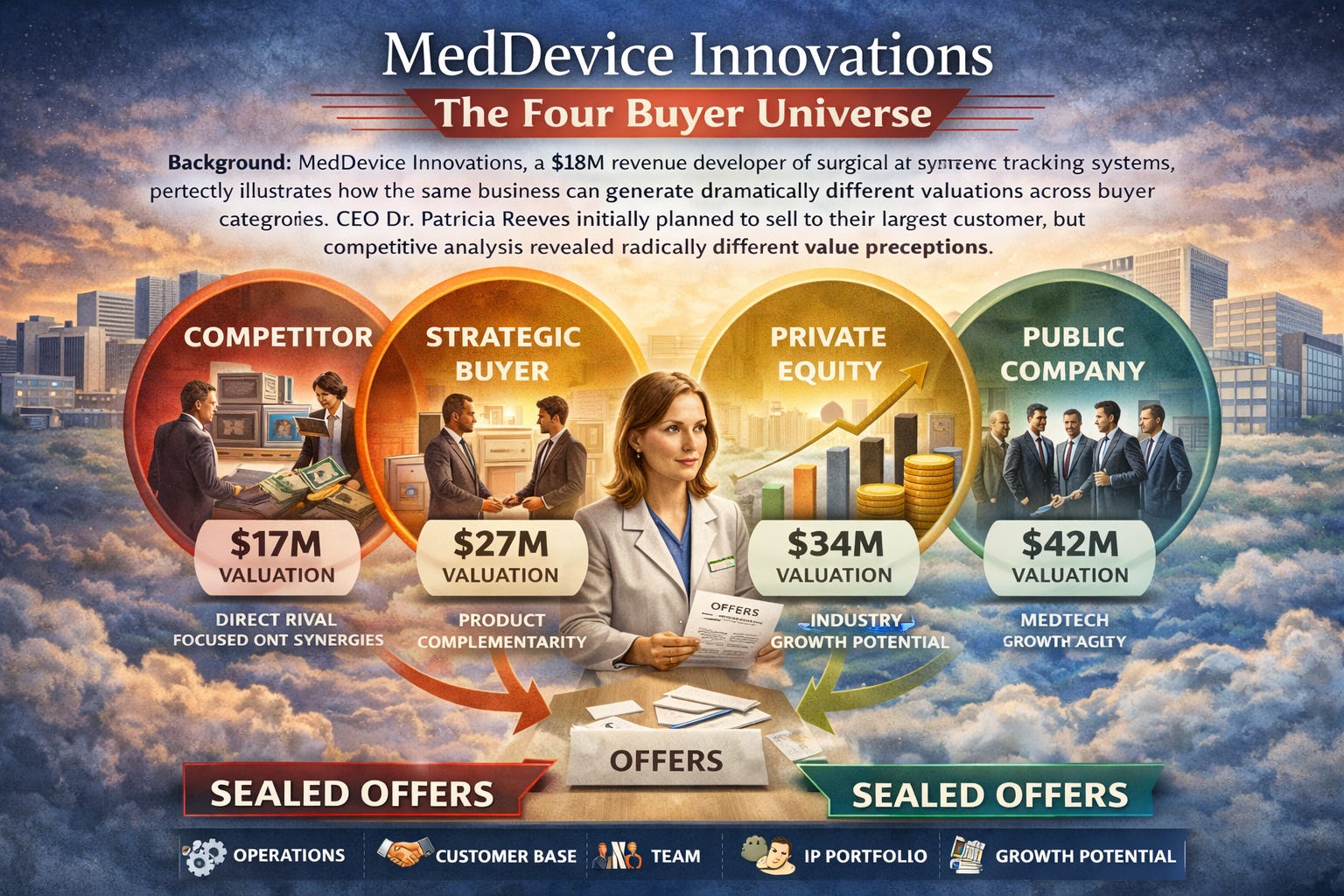

Background: MedDevice Innovations, a $18M revenue developer of surgical instrument tracking systems, perfectly illustrates how the same business can generate dramatically different valuations across buyer categories. CEO Dr. Patricia Reeves initially planned to sell to their largest customer, but competitive analysis revealed radically different value perceptions.

The Business Foundation:

Revenue: $18M annually (75% recurring software subscriptions, 25% hardware)

EBITDA: $3.6M (20% margin)

Market Position: Leading RFID tracking technology for surgical instruments

Customer Base: 240 hospitals across North America

Key Assets: Proprietary tracking algorithms, FDA clearances, hospital relationships

Buyer Category 1: Strategic Competitor Analysis

MedSupply Corp (Primary Customer/Competitor):

Valuation Approach: Asset-based with cost synergy focus

Strategic Logic: Eliminate competing technology, fold customer base into existing platform

Risk Assessment: High integration complexity, customer retention concerns

Required Rate of Return: 18% (due to integration risk and customer overlap)

Financial Analysis:

Revenue synergies: Limited (customer overlap reduces net gain)

Cost synergies: $1.2M annually (eliminate duplicate overhead)

Integration costs: $2.5M upfront

Valuation: $20M (5.6x EBITDA, 1.1x revenue)

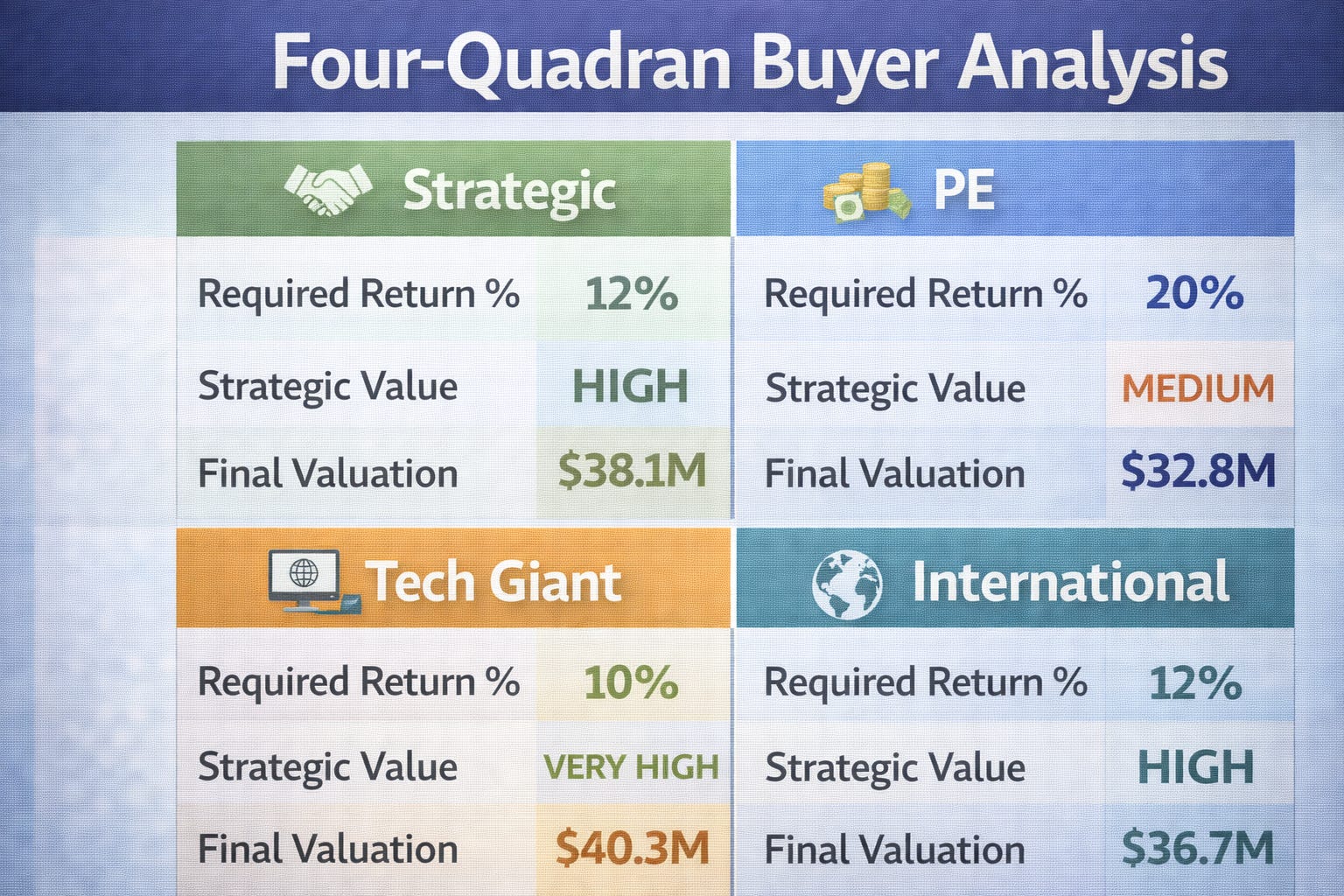

Buyer Category 2: Private Equity Analysis

HealthTech Growth Partners:

Valuation Approach: Discounted cash flow with consolidation thesis

Strategic Logic: Platform acquisition for healthcare IT rollup

Risk Assessment: Moderate (proven business model, recurring revenue)

Required Rate of Return: 14% (healthcare IT sector standard)

Financial Modeling:

Base case projections: 15% annual growth over 5 years

Multiple arbitrage opportunity (buy at 6x, sell at 10x EBITDA)

Add-on acquisition synergies: $500K annually by year 3

Valuation: $28M (7.8x EBITDA, 1.56x revenue)

Buyer Category 3: Technology Giant Analysis

TechMed Solutions (Fortune 500 Healthcare Technology):

Valuation Approach: Strategic value with ecosystem integration

Strategic Logic: Expand hospital platform with surgical workflow solutions

Risk Assessment: Low (established enterprise sales, proven technology integration)

Required Rate of Return: 12% (strategic premium for platform expansion)

Strategic Value Assessment:

Cross-selling opportunities across existing 1,200+ hospital customers

Technology integration with existing EHR platforms

Regulatory advantages (existing FDA relationships and compliance infrastructure)

Valuation: $36M (10x EBITDA, 2x revenue)

Buyer Category 4: International Strategic Analysis

EuroMed Technologies (German Healthcare Conglomerate):

Valuation Approach: Market entry premium with regulatory arbitrage

Strategic Logic: Establish North American surgical technology presence

Risk Assessment: Low integration complexity (standalone operation maintained)

Required Rate of Return: 10% (strategic market entry premium)

Market Entry Value Drivers:

Exclusive North American technology access worth 3-5 years development time

Regulatory pathway (FDA clearances) valued at $8-12M development cost equivalent

Customer relationships providing immediate market credibility

Currency arbitrage (Euro strength vs. USD at time of acquisition)

Valuation: $45M (12.5x EBITDA, 2.5x revenue)

The Competitive Process Results:

Round 1 Bidding:

MedSupply Corp: $20M

HealthTech Growth: $26M

TechMed Solutions: $32M

EuroMed Technologies: $42M

Round 2 Competitive Response:

MedSupply Corp: $24M (increased to prevent competitor acquisition)

HealthTech Growth: $30M (revised growth assumptions)

TechMed Solutions: $38M (strategic value recognition)

EuroMed Technologies: $45M (final offer)

Final Outcome: EuroMed Technologies acquired MedDevice Innovations for $45M, representing a $25M premium (125% increase) over the original strategic competitor approach.

Value Multiplication Analysis: The same $3.6M EBITDA business generated four different valuations based on buyer-specific required returns and strategic needs:

5.6x multiple (strategic competitor focused on cost elimination)

7.8x multiple (PE focused on financial engineering and consolidation)

10x multiple (tech giant focused on ecosystem expansion)

12.5x multiple (international buyer focused on market entry and regulatory advantages)

Dr. Reeves’ Reflection: “We almost sold to our biggest customer for $20M because it ‘made sense.’ The competitive process revealed that our regulatory approvals and customer relationships were worth $25M more to a buyer who didn’t already have them. Same business, same assets, completely different strategic value to different buyers.”

Case Study 2: Global Logistics Solutions - The Purchase Price Allocation Discovery

Background: Global Logistics Solutions, a $35M revenue third-party logistics provider, was acquired by TransCorp International for $78M. The purchase price allocation process revealed how unidentified intangible assets had nearly cost the seller millions in unrecognized value.

Pre-Sale Asset Understanding: CEO Michael Bolton believed his company’s value lay primarily in: