Open Your Borders: Restrict Markets Costs $$$$

Most business owners unknowingly cap their sale price before negotiations begin. Learn how Fair Market Value’s “open market” requirement could unlock millions more for your exit.

You spent 20 years building your business. Now you’re about to sell it — to the wrong person, for the wrong price. Not because buyers aren’t out there. Because you’ve already eliminated them without knowing it. The open market isn’t a theory. It’s the difference between comfort and generational wealth.

10 KEY TAKEAWAYS — OPEN AND UNRESTRICTED MARKET

FMV requires an open market: Fair Market Value legally assumes all potential buyers have access to bid, your behaviour must match that assumption.

Restricting buyers restricts price: Every buyer category you exclude pre-negotiation is cash you are voluntarily handing back.

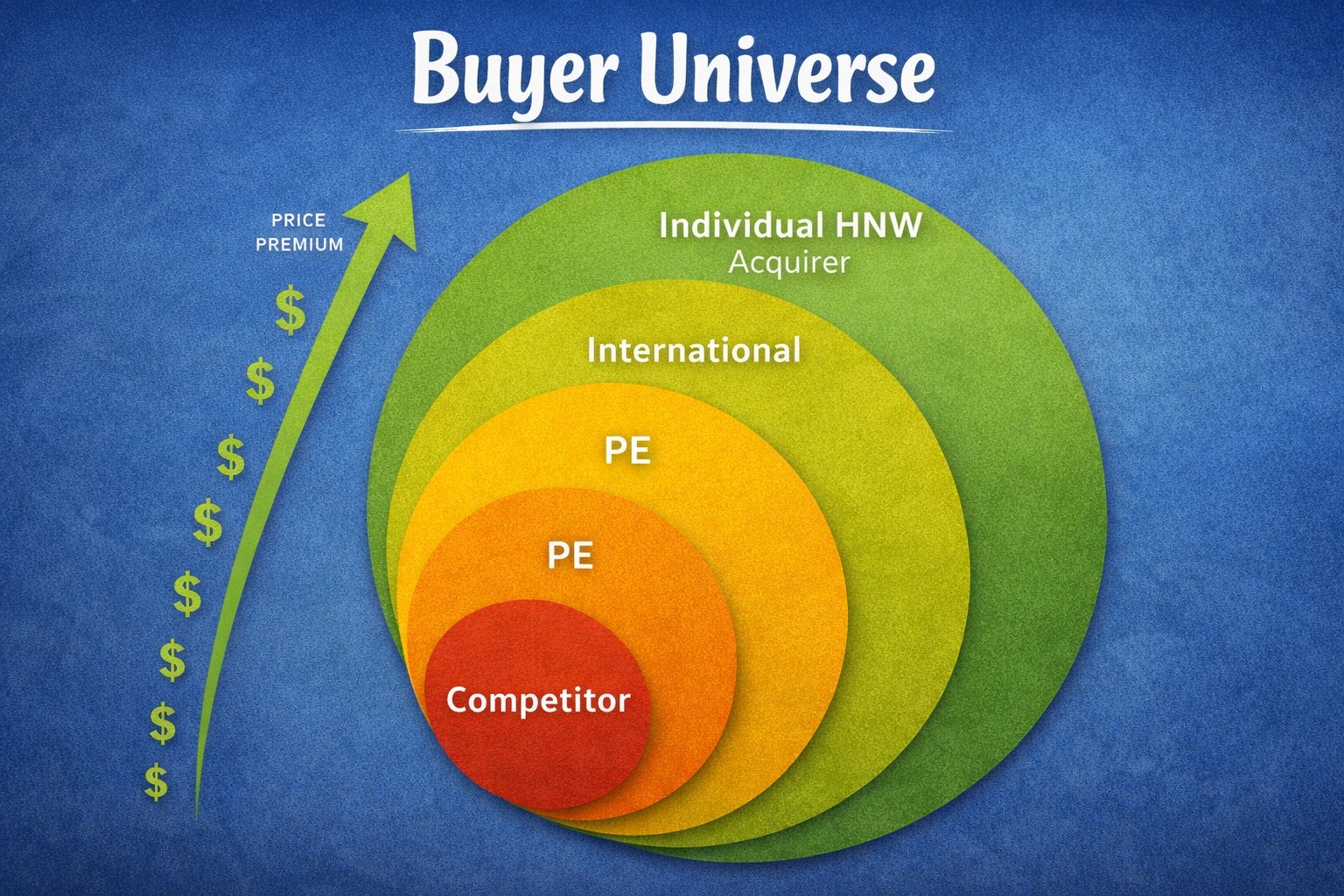

Competitors aren’t your only buyers: Strategic buyers, private equity firms, international acquirers, and high-net-worth individuals all belong in your buyer universe.

Competition is leverage: A single buyer negotiates like he’s your only option, because you made him that way. Multiple buyers compete. Competing buyers overpay.

Private equity raises the floor: Even if PE never wins your deal, their presence forces your competitor to stretch beyond what he planned to offer.

Secrecy is self-sabotage: Withholding financials or refusing to prepare a data room signals “amateur hour” to every professional buyer who sees it.

Your structure may be killing marketability: Tax structures, share restrictions, non-transferable contracts, and lease clauses can legally blockade buyers before they ever see your financials.

Always-ready beats desperate-to-sell: The worst negotiating position is needing to close. Perpetual sale-readiness flips the power dynamic entirely.

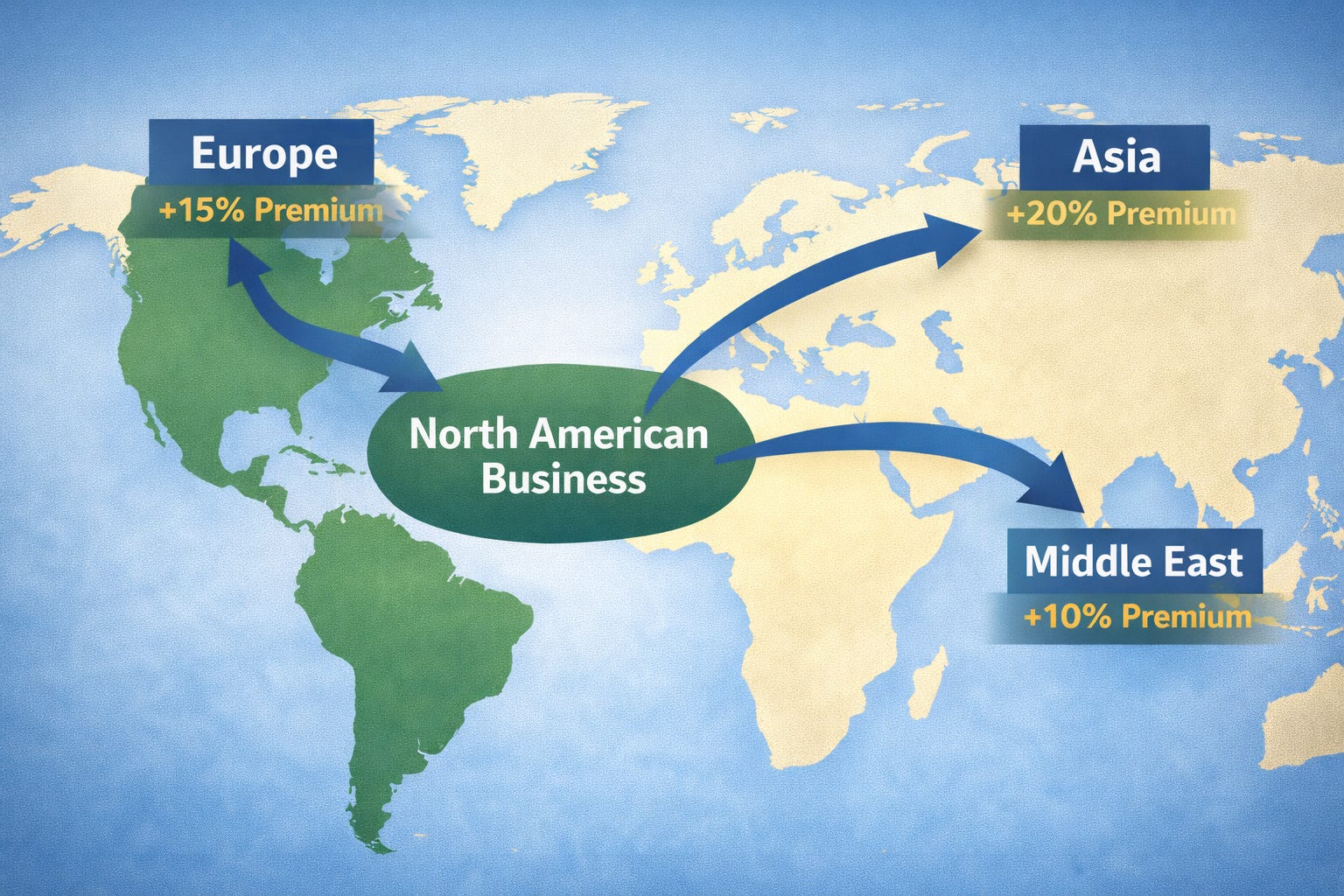

International buyers change the math: A deal that looks like $8M domestically can be $14.5M to a European buyer paying in a stronger currency for distribution access you take for granted.

The market is bigger than you think: This post walks through exactly how to open your borders — and why every door you close before launch is money you’ll never recover.

📚 READING PREREQUISITES

This post builds on foundational YBAWS! concepts. Full comprehension requires prior posts. Key terms and formulas are revisited deliberately to reinforce how they compound.

Recommended Prior Reading:

Chapter 7: Fair Market Value — Where Amateurs Stop and Professionals Begin

Chapter 5: Strategic vs. Financial Buyers — Know Who’s Sitting Across the Table

Chapter 3: Transferable Value — Building a Business That Operates Without You

What “Open and Unrestricted” Actually Means

The Fair Market Value definition isn’t just legal boilerplate. Every word is a profit instruction. “Open and unrestricted market” means the highest price you can achieve assumes no one has been blocked from bidding. The moment you restrict access, to buyers, to information, to the deal itself, you have mathematically departed from FMV and started negotiating against yourself.

Most owners don’t realize they’ve already done this before they put the sign out. They’ve decided it makes sense to sell to the biggest competitor. They’ve decided to keep financials close to the vest until a buyer shows real interest. They’ve decided the legal structure doesn’t need fixing until there’s a real deal on the table. Every one of those decisions is a buyer elimination.

The restrictions that quietly kill your price:

Limiting outreach to competitive buyers only

Refusing to prepare a data room until “serious” interest materializes

Share transfer restrictions embedded in your shareholder agreement

Client contracts or supplier agreements that don’t survive a change of control

Tax structures that make today’s sale punishingly expensive

No confidential information memorandum (CIM) or management presentation prepared

Why Your Competitor Is Your Worst-Priced Buyer

Here’s the uncomfortable math. Your biggest competitor already has what you’re selling. He has your market, your customer segment, and your distribution model or something close to it. He’s calculating synergies and cost eliminations when he builds his offer. His upside is what he can strip out. Your upside to him is bounded by how much cheaper he can run your operation post-acquisition.

Private equity buyers operate under completely different arithmetic. They’re not buying your customers, they’re buying a financial instrument with a target internal rate of return. They have b/million-dollar funds with deployment mandates. If your business fits their thesis, the spreadsheet dictates the price not a budget committee terrified of overpaying.

You may never sell to PE. But the moment your competitor knows PE is in the room, his “final offer” becomes his opening bid.

Why competition changes buyer behavior:

Strategic buyers face internal approval friction, competition creates urgency that bypasses committees

PE buyers with capital deployment pressure will stretch on price when competitive

International buyers bring alternative currency and strategic needs your domestic buyers already possess

Individual acquirers seeking turnkey entry have no existing infrastructure to justify low-ball synergy pricing

The Geography of Your Buyer Universe

The definition of “open market” has exploded in the digital age. A business valued at $5M in your domestic market could be priced at $8–12M to an international buyer purchasing market entry, technology access, or distribution infrastructure they’d otherwise spend years building.

A client was convinced his $8M deal with his largest competitor was the right move. “They know the business,” he said. Eighteen months and a proper process later, a European acquirer paid $14.5 million. The difference had nothing to do with the business changing. The European buyer was paying for distribution access the competitor already had and paying in Euros. That gap is not a rounding error. That’s retirement money, college money, and a different life for his family.

If you haven’t structured your business, your documentation, and your marketing for international buyers, you’ve already cut off potentially your highest bidder. Currency, regulatory approvals, and deal structures matter but they’re solvable. Leaving international buyers off the list because it feels complicated is just expensive laziness.

The Control Factor: Opening Borders Means Gaining Leverage

Most owners resist an open process because it feels like losing control. The opposite is true. With one buyer, he controls everything, timing, terms, information access, and the pace of your anxiety. With multiple buyers, you control all of it. You decide who gets to the next stage. You set the timeline. You determine what information goes to whom and when.

A single buyer negotiates with the confidence of a monopolist. Multiple buyers negotiate with the anxiety of someone who might lose. That anxiety is worth millions.

THE MARKET DOESN’T CARE ABOUT YOUR COMFORT ZONE. IT ONLY CARES ABOUT WHAT YOU’RE WILLING TO DO TO ACCESS IT.

💡 KEY TAKEAWAYS

Remember These Core Principles:

Open market = maximum competition: FMV assumes no one is blocked from bidding. Match that assumption or leave money behind.

Competitors are your worst-priced buyers: They calculate what to eliminate. Everyone else calculates what to gain.

Private equity raises every other offer: They don’t need to win to be valuable. Their presence alone inflates the room.

International buyers change the price ceiling: $10M to you is lunch money in Dubai. Stop pretending geography is a barrier.

Control comes from options, not secrecy: Multiple buyers give you leverage. One buyer gives you anxiety.

❓ FREQUENTLY ASKED QUESTIONS

Q: Do I have to sell to whoever bids highest in an open process? A: No. An open process gives you options and information. You control who progresses, what terms you accept, and whether you close at all. The goal is maximum exposure — final decision is always yours.

Q: Won’t showing my financials to competitors put my business at risk? A: Managed correctly through NDAs and staged disclosure, professional buyers see only what’s appropriate at each stage. Your M&A advisor controls information flow. The risk of secrecy far exceeds the risk of disclosure.

Q: How do I attract international buyers? A: Through professional business brokers with cross-border networks, targeted outreach to international strategic acquirers, and positioning your confidential information memorandum for non-domestic audiences. Currency and strategic context matter in your materials.

Q: What if I only want to sell to a specific buyer? A: That’s your right. But understand what it costs you. A restricted sale to one preferred buyer almost always produces a lower price than a competitive process — often by millions.

🎯 READY TO EXPAND YOUR BUYER UNIVERSE?

Understanding the open market principle is just one piece of building a valuable, marketable business.

Subscribe to YBAWS! for weekly insights on business valuation, M&A strategy, and maximizing your company’s worth. Join business owners building more valuable, marketable businesses through unvarnished truth about business exits.

Have questions about your specific situation? Drop a comment below or reach out directly — I respond to every message.

📖 RELATED READING

Continue Your Learning:

Investopedia — Private Equity: Definition, How It Works, and History: Foundational explanation of how PE funds deploy capital and evaluate acquisition targets.

CBV Institute — Business Valuation Standards in Canada: Professional standards governing how Canadian valuators apply the FMV definition in practice.

Harvard Business Review — The Art of Selling Your Business: Strategic framework for running competitive M&A processes and understanding buyer motivations.

CONNECT WITH SAFERWEALTH

Web: SaferWealth.com - Alternative Startup Funding Structures

YouTube: SaferWealth Posts - VC Risk Swap Educational Content

LinkedIn: LinkedIn @SaferWealth - Startup Finance Innovation

Rumble: @saferwealth - Educational video content on business valuation

Instagram: @saferwealth - Quick insights and updates

👤 ABOUT THE AUTHOR

Sean Cavanagh, BAS, CPA, CA, CF, CBV

With over three decades negotiating business sales and conducting valuations, Sean delivers unvarnished truth about business exits. Starting at Deloitte and Canada Revenue Agency, he now advises business owners through his M&A practice. YBAWS! reflects his frustration with owners who consistently overvalue their companies.

📚 DO YOUR OWN RESEARCH

Professional Standards & Organizations:

Key Terms & Definitions:

Specific Sources Referenced:

CBV Institute. “Valuation Terminology and Fair Market Value Standard.” CICBV Practice Bulletins, 2023.

https://www.cbvinstitute.com

Investopedia. “Private Equity.” Dotdash Meredith, 2024. https://www.investopedia.com/terms/p/privateequity.asp

Wikipedia. “Data Room.” Wikimedia Foundation, 2024. https://en.wikipedia.org/wiki/Data_room

⚖️ EDUCATIONAL DISCLAIMER

This guide provides information only, not professional advice. Consult qualified advisors for your specific situation. All cases are fictional, created for educational purposes from collective industry experience. Neither the author nor YBAWS! accepts liability for actions based on this content. This material supplements but never replaces proper professional consultation and judgment.

YBAWS! (Your Business Ain’t Worth Sh*t!) is a trademark and educational platform dedicated to helping business owners understand corporate value and marketability.

© 2026 YBAWS! All rights reserved.