Pure AI vs. AI-Enabled: The Taxonomy That Determines Fundability

Not all AI companies face equal risk. Pure AI startups face hyperscaler talent poaching. AI-enabled companies face commodity risk. Your category determines your funding strategy.

There is a critical distinction that determines whether you attract serious capital or get passed over. Are you a pure AI company, an AI-enabled company, or an infrastructure AI company? Get this categorization wrong and you pitch the wrong story to the wrong investors at the wrong valuation. Classification matters.

10 KEY TAKEAWAYS - AI COMPANY TAXONOMY

1. Pure AI companies build foundational models: The product IS the AI. Value proposition is breakthrough technology.

2. AI-enabled companies use AI as feature: The company would exist without AI. AI makes existing solutions better.

3. Infrastructure AI builds tools for builders: Picks and shovels of the AI gold rush. Lower talent poaching risk.

4. Hyperscaler risk threatens pure AI: Google, Microsoft, and Anthropic can hire your team without buying your company.

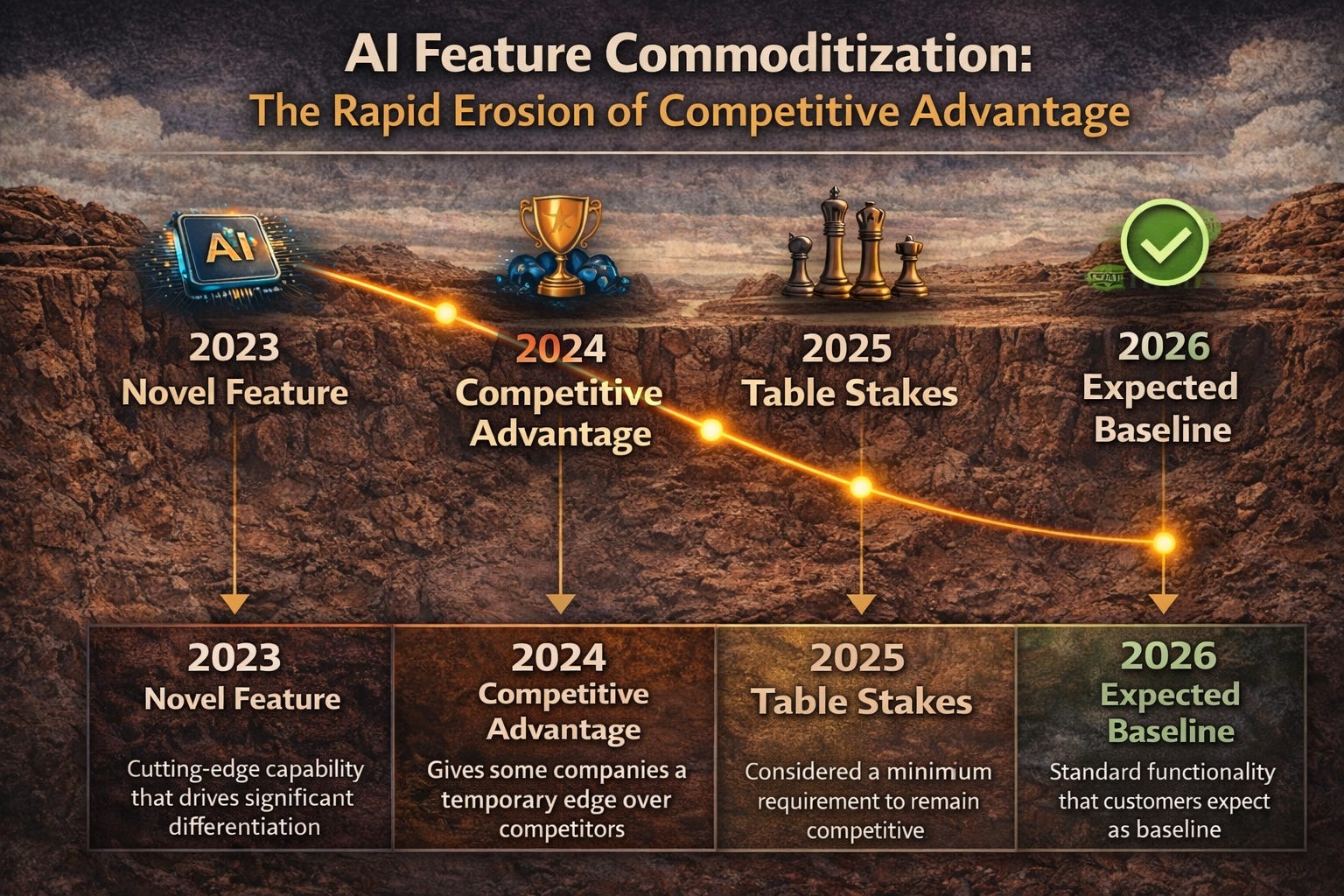

5. Commodity risk threatens AI-enabled: Foundation model improvements make your features table stakes within months.

6. Platform risk threatens infrastructure: AWS launching your feature as a service can destroy your startup overnight.

7. Each category needs different moats: Talent retention for pure AI, business moats for AI-enabled, niche focus for infrastructure.

8. Dilution expectations vary by category: Pure AI requires 25-30% per round to compensate for hyperscaler poaching risk.

9. Revenue guarantees protect both sides: The VC Risk Swap structure addresses category-specific risks through milestone funding.

10. Positioning determines your pitch: Lead with business moat for AI-enabled, talent retention for pure AI, niche defense for infrastructure.

📚 READING PREREQUISITES

This post builds on concepts introduced in the series opener. Understanding the AI valley of death and temporal mismatch between AI capital requirements and traditional seed funding provides essential context for evaluating category-specific risks.

Recommended Prior Reading:

• Post 1: The AI Valley of Death - Why Seed Funding Timelines Are Broken

• Series overview available at SaferWealth.com

The Three Categories of AI Companies

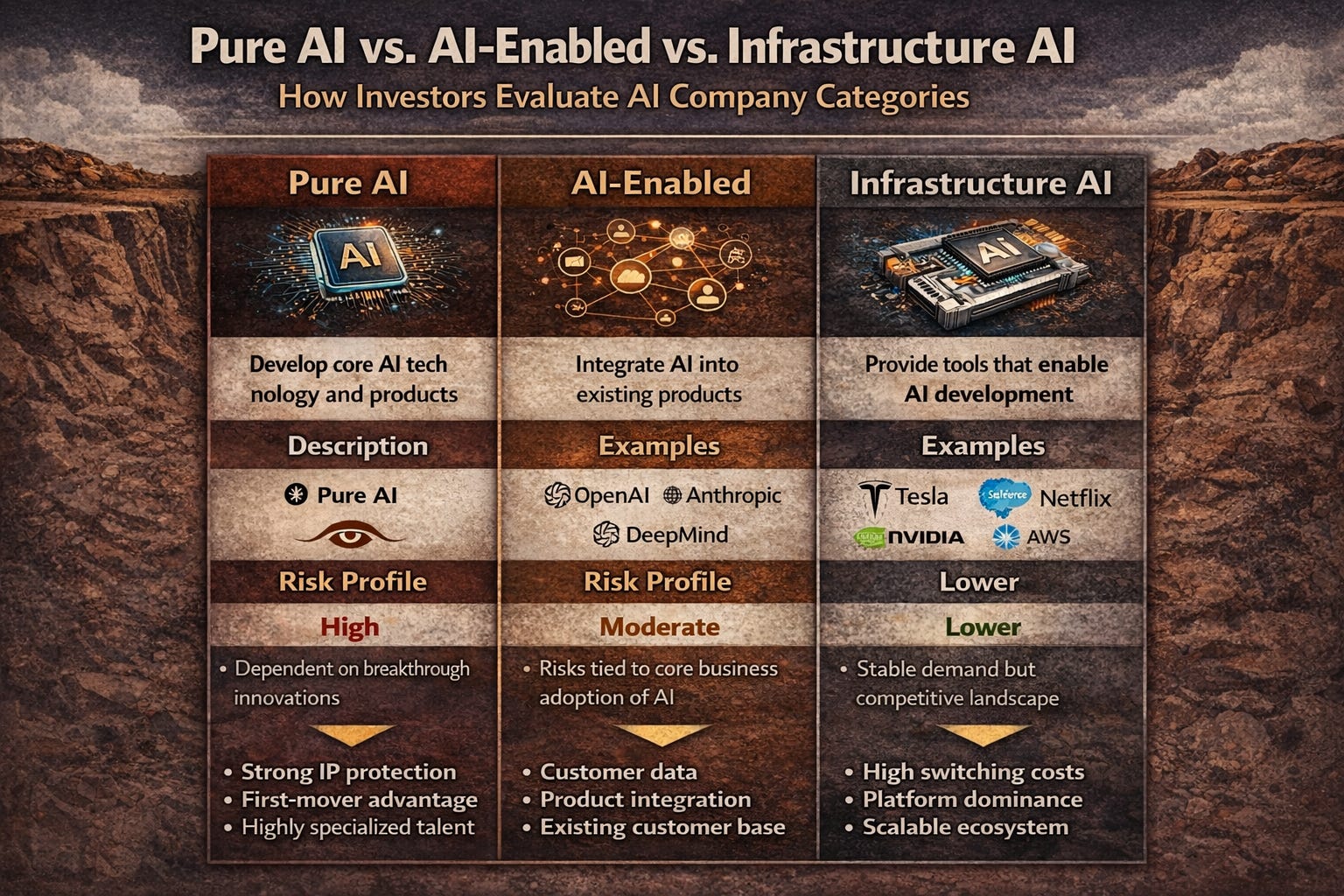

Pure AI companies build the core technology itself. Think Anthropic, OpenAI, Mistral, Cohere. Any company developing foundational models, novel architectures, or breakthrough training approaches. These companies exist because of AI. Without the AI innovation, there is no company. The product IS the AI.

AI-enabled companies use AI as a feature or component within a broader product. Think Notion integrating AI writing assistants, Figma adding AI design tools, or any vertical SaaS adding AI capabilities. The company would still exist and have value without the AI layer. The AI just makes it significantly better.

Infrastructure AI companies build tools for other AI companies. The picks and shovels of the AI gold rush. Think model optimization platforms, MLOps tooling, training infrastructure, evaluation frameworks. These companies do not build AI models themselves. They help others build AI better, faster, cheaper.

Why Taxonomy Matters for Funding

Each category faces completely different risk profiles, different moats, different exit paths, and different investor expectations. Misclassifying yourself means pitching the wrong story to the wrong investors at the wrong valuation.

Pure AI: Hyperscaler Risk

Pure AI companies face hyperscaler risk, the constant existential threat that Google, Microsoft, Meta, or Anthropic will simply hire away your founders and engineers without acquiring the company. This is the reverse acqui-hire phenomenon that gutted Inflection AI, hollowed out Character.AI, and killed Haiper.

Your entire value proposition lives inside the heads of 5-10 technical people. If they leave, the company evaporates. Investors in pure AI companies are essentially betting that you will either get acquired before hyperscalers poach your team, or that you will build enough business momentum that losing founders does not kill the company.

Pure AI Risk Profile:

• Talent concentration: 3-5 people hold all value

• Capital intensity: $50M-$200M+ to compete on model quality

• Exit pressure: Founders increasingly attractive to hyperscalers as company raises more

• Paradox: Every dollar raised increases pressure that makes founders more likely to leave

AI-Enabled: Commodity Risk

AI-enabled companies face commodity risk, the threat that AI features you are building will become table stakes within 12 months as foundation model capabilities improve. What differentiated you in 2024 becomes an expected baseline feature by 2025.

Your AI-powered customer service chatbot was novel in early 2024. By late 2025, every customer service platform has one. Your AI writing assistant was unique in 2023. Now every productivity tool has AI writing built in. The defensibility question haunts AI-enabled companies: if your competitive advantage comes from AI features, and foundation models improve by 10x every year, what happens when competitors can build your features in a weekend?

You need real business moats, integration depth, workflow lock-in, proprietary data, regulatory compliance, that exist independent of your AI capabilities. The AI should accelerate your moat, not be the moat itself.

Infrastructure AI: Platform Risk

Infrastructure AI companies face platform risk, the threat that cloud providers or foundation model companies will build your functionality into their core offerings. AWS launching a new MLOps feature can destroy your startup overnight. OpenAI adding a model evaluation dashboard makes your evaluation startup redundant.

But here is what makes infrastructure companies interesting: they carry the lowest reverse acqui-hire risk. Hyperscalers do not typically poach entire teams from MLOps startups. They just copy the features. Your team is valuable, but not irreplaceable the way a foundational model research team is. This makes infrastructure AI companies more fundable at reasonable dilution levels.

Infrastructure AI Defensibility:

• Fundable if solving pain points hyperscalers ignore: Model optimization for edge devices, MLOps for regulated industries

• Less fundable if generic: Experiment tracking already won by Weights & Biases and commoditized by cloud providers

• Best strategy: Find compliance or niche requirements that create moats hyperscalers will not address

Funding Strategies by Category

Understanding your category determines your funding approach, valuation expectations, and the story you tell investors.

Pure AI Companies:

• Expect 25-30% dilution per round to compensate investors for hyperscaler poaching risk

• Articulate credible talent retention strategies before investors ask

• Build business momentum that survives founder departure

• Consider alternative structures that hedge acqui-hire risk

AI-Enabled Companies:

• Lead with business moat, not AI capabilities

• Demonstrate value proposition survives if AI features become commoditized

• Show retention and expansion metrics that validate lock-in

• Expect evaluation using SaaS metrics, not AI metrics

Infrastructure AI Companies:

• Prove you are solving pain points hyperscalers will not address directly

• Demonstrate niche or compliance requirements that create defensibility

• Show customer concentration is manageable

• Price using B2B SaaS frameworks with platform risk discount

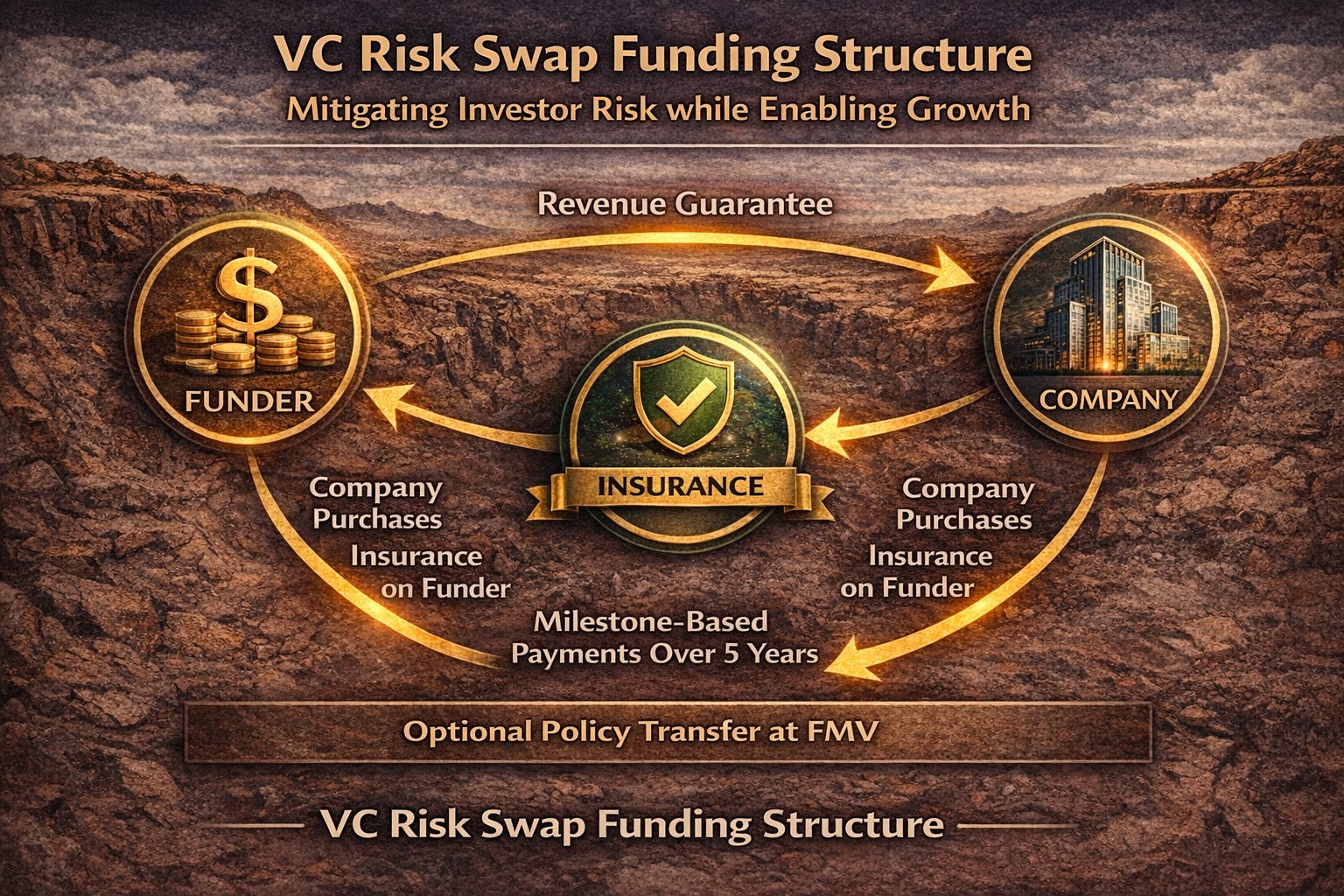

The VC Risk Swap: Category-Specific Protection

Traditional equity investment fails all three categories for different reasons. The VC Risk Swap offers an alternative structure that addresses category-specific risks while preserving founder equity and providing funder downside protection.

How the VC Risk Swap Works:

Instead of traditional equity investment, a Funder provides milestone-based revenue guarantees to the company through a Revenue Guarantee Agreement. The company uses these guarantees to access growth capital at lower cost than equity financing. The structure spans approximately five years with defined milestones.

The company purchases life insurance on the Funder’s life for business continuity protection. This insurance, owned by the company, provides downside protection if the funding relationship is disrupted. After the funding period, the Funder has an option to acquire the policy at fair market value.

Why This Addresses Category-Specific Risks:

For Pure AI Companies

The VC Risk Swap addresses hyperscaler risk through milestone-based funding that does not require massive upfront equity dilution. Founders retain meaningful ownership during the highest-uncertainty phase. If a reverse acqui-hire occurs, the insurance component provides downside protection for funders rather than total loss. The structure creates alignment without the pressure that drives founders toward hyperscaler job offers.

For AI-Enabled Companies

Revenue guarantees allow AI-enabled companies to fund feature development without taking dilution before proving the features create sustainable value. If AI capabilities commoditize faster than expected, the milestone structure allows both parties to reassess without the binary outcomes of traditional equity. The company can pivot or wind down gracefully rather than being trapped by equity investor expectations.

For Infrastructure AI Companies

Infrastructure companies face platform risk that can materialize suddenly. The VC Risk Swap provides capital access without locking companies into equity structures that assume steady growth. If a hyperscaler launches competing functionality, the milestone-based structure allows adaptation rather than forced continuation of a compromised strategy.

Key VC Risk Swap Benefits:

• Preserves founder equity: No dilution during highest-uncertainty commercialization phase

• Eliminates governance conflicts: Funders participate through revenue guarantees, not board seats

• Provides downside protection: Insurance component hedges catastrophic outcomes for funders

• Creates milestone alignment: Capital deployment matches actual progress, not arbitrary timelines

• Enables graceful outcomes: Moderate success generates returns through revenue share, not just binary equity exits

Positioning Your Company Correctly

The most common founder mistake is positioning themselves in the wrong category. Building an API wrapper but pitching as a pure AI company. Creating a foundational model but pitching as infrastructure. Developing AI features for a vertical but calling yourself an AI company.

For Founders:

• Be honest about which category you occupy

• If pure AI, acknowledge hyperscaler risk and explain talent retention strategy

• If AI-enabled, lead with business moat, not AI capabilities

• If infrastructure, prove you solve pain points hyperscalers will not address

For Investors:

• Verify category before evaluating the pitch

• Apply category-appropriate frameworks and metrics

• Price deals to reflect category-specific risks

• Consider alternative structures that hedge category-specific risks

The AI taxonomy is not about which companies are better. It is about which risk profile matches your investment thesis and which business models can actually survive the next five years. Choose your category wisely, because it determines everything that follows.

💡 KEY TAKEAWAYS

Remember These Core Principles:

• Know your category: Pure AI, AI-enabled, or infrastructure determines your entire funding strategy

• Match risk to structure: Each category faces different primary risks requiring different protective mechanisms

• Consider the VC Risk Swap: Revenue guarantees with insurance protection address category-specific risks traditional equity ignores

• Build appropriate moats: Talent retention for pure AI, business lock-in for AI-enabled, niche focus for infrastructure

• Position honestly: Misclassifying yourself leads to wrong investors, wrong valuations, and wrong expectations

❓ FREQUENTLY ASKED QUESTIONS

Q: What is the difference between a pure AI company and an AI-enabled company?

A: Pure AI companies exist because of AI. The product IS the AI, like Anthropic building Claude or OpenAI building GPT. AI-enabled companies use AI as a feature within a broader product. Notion would exist without AI; the AI writing assistant just makes it better. The distinction determines risk profile and funding strategy.

Q: Why is hyperscaler risk the primary threat to pure AI companies?

A: Pure AI company value concentrates in 5-10 technical people who understand model architecture, training approaches, and data pipelines. Google, Microsoft, or Anthropic can hire these individuals without acquiring the company. This reverse acqui-hire leaves investors with worthless equity while founders get lucrative employment offers.

Q: How does the VC Risk Swap protect against reverse acqui-hires?

A: The VC Risk Swap includes life insurance on the Funder owned by the company. If a reverse acqui-hire disrupts the funding relationship, the insurance component provides downside protection. Additionally, milestone-based funding reduces the pressure that drives founders toward hyperscaler job offers by preserving their equity during high-uncertainty phases.

Q: What moats should AI-enabled companies build?

A: AI-enabled companies need business moats independent of AI quality: integration depth with customer systems, regulatory compliance requirements, proprietary data that improves with usage, workflow lock-in that creates switching costs. The AI should accelerate the moat, not be the moat itself. Foundation model improvements will commoditize AI features within months.

Q: Why are infrastructure AI companies more fundable at reasonable dilution?

A: Infrastructure companies face platform risk but carry lower reverse acqui-hire risk. Hyperscalers copy features rather than poach entire teams. This means infrastructure company equity is less likely to evaporate through talent absorption, making traditional equity structures more viable and dilution expectations more reasonable.