Multiple Choice Questions

1. What is the central message of the M&A adage “you name the price, I name the terms”?

A. Price negotiation always precedes terms negotiation B. The party that controls the structural terms typically captures more value than the party that focuses on the headline price C. Buyers and sellers should negotiate price and terms separately D. Terms are negotiable but price is fixed

2. What are the three pillars of an aligned incentive earnout structure?

A. High cash percentage, short earnout period, and personal guarantees B. Operational control, contractual resource commitments, and combined entity performance metrics C. Senior secured notes, equity participation, and tax efficiency D. Strategic veto, competitive bidding, and arbitration provisions

3. Why does the chapter argue that “best efforts” language is inadequate as a buyer commitment?

A. Courts have ruled best efforts language unenforceable B. Best efforts language is decoration without quantified, contractual specificity C. Best efforts language increases legal fees during disputes D. Best efforts language creates tax disadvantages for the seller

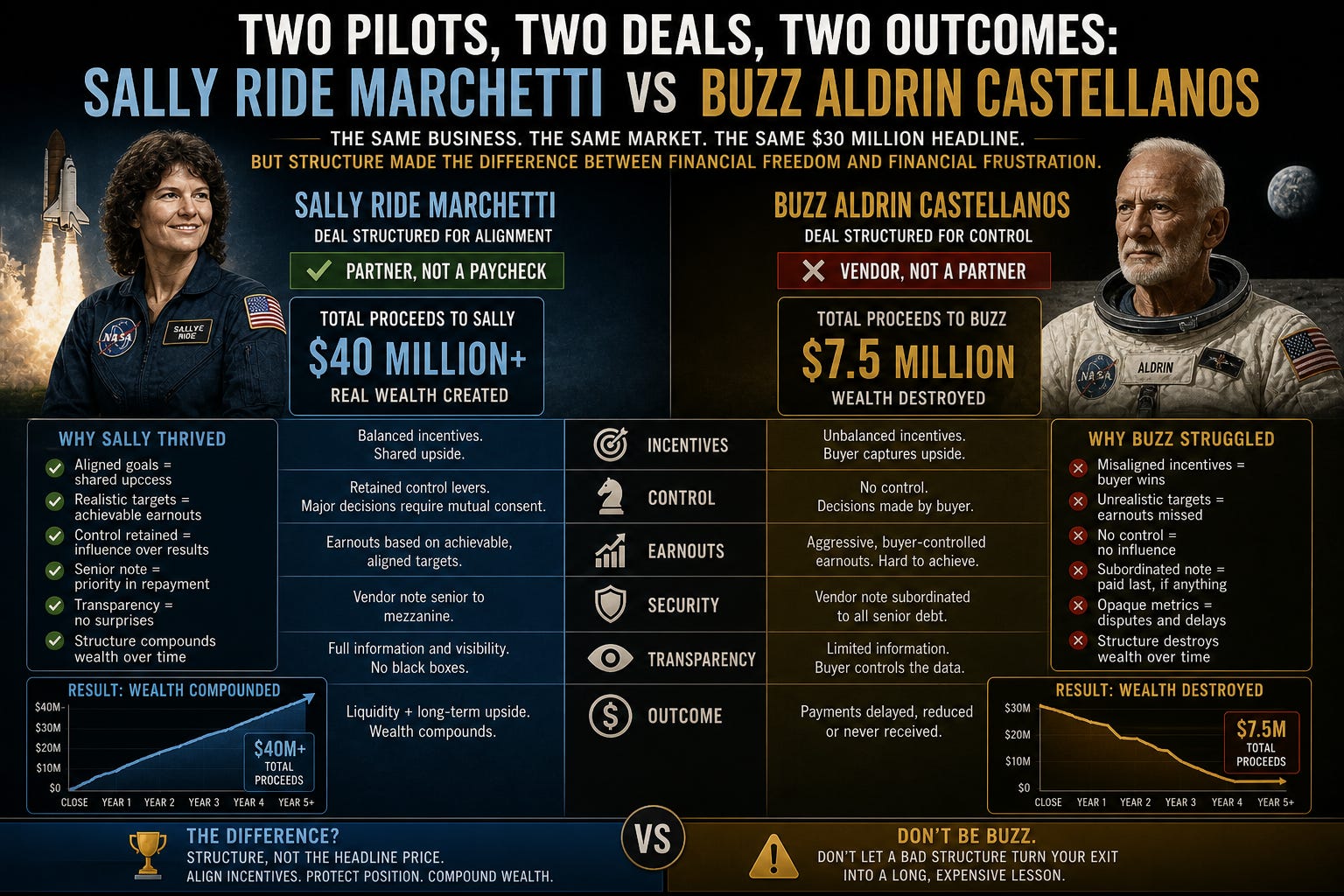

4. In the Sally Ride Marchetti versus Buzz Aldrin Castellanos comparison, what was the headline offer made by MedStack Holdings to both founders?

A. $24 million B. $28 million C. $32 million D. $40 million

5. What was the cash at closing component of Sally’s final negotiated structure?

A. $5 million B. $9 million C. $14 million D. $19 million

6. What was Buzz’s total realization at year five of his deal?

A. $5 million B. $9.4 million C. $14 million D. $20 million

7. What structural feature converted $5 million of Sally’s earnout from contingent into deferred but certain value?

A. A personal guarantee from MedStack’s CEO B. A minimum payment floor payable regardless of performance C. A senior secured note position D. A change of control acceleration clause

8. Why did Sally insist that her earnout be tied to combined healthcare technology segment EBITDA rather than Apogee’s standalone results?

A. Combined metrics produced higher numerical targets B. Combined metrics eliminated MedStack’s ability to manipulate Apogee’s standalone metrics through resource allocation and transfer pricing C. Combined metrics simplified the calculation methodology D. Combined metrics qualified for preferential tax treatment

9. What governance authority did Sally retain that allowed her to block the proposed product platform consolidation in year one?

A. Board veto rights B. Strategic veto power on product roadmap, customer transitions, and personnel changes affecting Apogee’s core team C. Shareholder approval rights D. Audit committee oversight

10. What was the total realized value of Sally’s deal by year five?

A. $19 million B. $27 million C. $32 million D. $39 million

Explanation Questions

Question 1. Explain the principle that “terms determine outcomes more than price” using the specific outcomes of the Sally Ride Marchetti and Buzz Aldrin Castellanos comparison. Quantify the difference and identify the structural drivers.

Question 2. Describe each of the three pillars of an aligned incentive earnout structure, and explain how each pillar addresses a specific failure mode of poorly designed earnouts.

Question 3. Identify the specific characteristics of a “cash worthy” business and explain why building these characteristics is a prerequisite for earning the right to demand cash on closing rather than accepting earnout structures.

Question 4. Compare the negotiation behavior of Sally and Buzz during their respective MedStack interactions. Identify three specific decisions Sally made that Buzz did not, and explain how each decision contributed to the outcome differential.

Question 5. Explain why the chapter argues that “the buyer’s negotiation behavior predicts post closing behavior.” Use the contrasting MedStack experiences of Sally and Buzz to illustrate the principle.

Multiple Choice Answer Key

B. The party that controls the structural terms typically captures more value than the party that focuses on the headline price. The adage exists because terms determine whether the price is real, and most sellers spend their negotiation energy on the headline rather than on the structural mechanics.

B. Operational control, contractual resource commitments, and combined entity performance metrics. These three pillars working together convert an earnout from a value extraction mechanism into a genuine partnership structure.

B. Best efforts language is decoration without quantified, contractual specificity. Generic best efforts and good faith clauses are nearly useless because they cannot be enforced against documented business judgment by the buyer.

C. $32 million. MedStack Holdings offered both Sally and Buzz the same $32 million headline number, demonstrating that identical headline offers can produce dramatically different realized outcomes based purely on structural negotiation.

C. $14 million. Sally’s negotiated structure included $14 million cash at closing, nearly tripling Buzz’s $5 million cash component despite identical headline numbers.

B. $9.4 million. Buzz’s total realization at year five was approximately $9.4 million from a $32 million headline, with the remaining contingent value effectively destroyed by MedStack’s strategic pivot, subordination of his vendor note, and manipulation of operational efficiency metrics.

B. A minimum payment floor payable regardless of performance. The $5 million minimum floor converted contingent value into deferred but certain value, dramatically improving the risk adjusted present value of Sally’s deal.

B. Combined metrics eliminated MedStack’s ability to manipulate Apogee’s standalone metrics through resource allocation and transfer pricing. Tying earnouts to combined entity performance neutralizes most of the soft default mechanisms available to a sophisticated buyer.

B. Strategic veto power on product roadmap, customer transitions, and personnel changes affecting Apogee’s core team. This authority, contractually established for the five year CEO retention period, gave Sally enforceable tools to defend the operational decisions that determined earnout achievement.

D. $39 million. Sally’s total realized value at year five was $39 million, composed of $14 million cash, $8 million earnout payments, $5 million minimum floor, and approximately $12 million in MedStack equity.

Explanation Question Solutions

1. The principle that terms determine outcomes more than price is demonstrated in the Marchetti and Castellanos comparison by a $29.6 million realized outcome differential on identical $32 million headline offers. Sally received $39 million. Buzz received $9.4 million. The structural drivers of the differential are direct and traceable. Sally negotiated $14 million cash at closing versus Buzz’s $5 million, capturing $9 million of additional certain value. Sally negotiated a $5 million minimum payment floor that converted contingent value into deferred but certain value, while Buzz had no floor. Sally negotiated combined entity performance metrics that prevented manipulation, while Buzz accepted standalone metrics that MedStack could and did manipulate. Sally negotiated CEO retention with strategic veto, preserving her ability to defend operational decisions, while Buzz had no governance authority. Sally negotiated $5 million in MedStack equity that captured portfolio level appreciation, while Buzz had no equity participation. Each structural decision compounded the other across five years to produce a 4x outcome differential on identical price.

2. The first pillar, shared operational control, addresses the failure mode in which the buyer makes every decision that determines earnout achievement while the seller bears the financial consequences. Operational control through a CEO or president role with strategic veto rights gives the seller enforceable tools to defend the decisions that drive earnout outcomes. The second pillar, contractual resource commitments with quantified specificity, addresses the failure mode of soft defaults where the buyer starves the acquired company of resources to depress earnout metrics while remaining technically compliant. Quantified commitments such as “$15 million in incremental capital across years one through three, allocated as follows” eliminate the discretion the buyer would otherwise use to redirect resources elsewhere. The third pillar, combined entity performance metrics, addresses the failure mode in which the buyer manipulates standalone metrics through transfer pricing, cost allocation, and resource reallocation. Tying earnouts to combined business performance neutralizes most of the manipulation pathways and aligns the buyer’s incentives with the seller’s earnout achievement.

3. A cash worthy business has six identifiable characteristics: predictable recurring revenue spread across a diversified customer base with no single client over 15% of revenue, operational systems that run without the founder’s daily involvement, documented processes that allow seamless ownership transfer, management depth that enables independent operation, financial infrastructure meeting institutional buyer due diligence standards, and transferable customer relationships not dependent on the founder’s personal involvement. Building these characteristics is a prerequisite for demanding cash because they directly reduce the buyer’s perceived risk, which lowers the required rate of return, which raises enterprise value while simultaneously eliminating the buyer’s justification for contingent payment structures. Buyers structure earnouts when they perceive risk they want to transfer back to the seller. A cash worthy business has eliminated most of that risk. The buyer cannot credibly demand contingent structures when the business itself does not require them, and the seller therefore has the negotiating leverage to demand cash on closing.

4. Three specific decisions Sally made that Buzz did not, with their outcome contributions. First, Sally hired a chartered business valuator with forty seven healthcare technology deal closures, while Buzz used a generalist lawyer. The valuator ran a probability weighted present value analysis on MedStack’s initial $32 million proposal before any negotiation began and calculated the real value at $11 million on a single page. This established Sally’s analytical foundation and prevented anchoring on the headline. Second, Sally explicitly told MedStack she would not accept their initial structure but would consider a partnership structure with aligned incentives, while Buzz signed within six weeks of the first conversation. This converted the negotiation from a price discussion into a structural redesign. Third, Sally invested four months in the negotiation to obtain quantified protections, while Buzz prioritized speed. The four months of additional negotiation work produced the $29.6 million outcome differential, representing one of the highest hourly returns on negotiation labor in the chapter’s framework.

5. The chapter’s principle that the buyer’s negotiation behavior predicts post closing behavior rests on the recognition that buyer behavior during negotiation reveals the buyer’s actual intent and operating style. Good faith buyers willing to operate as genuine partners will negotiate substantively on structural protections, accepting minimum payment floors, agreeing to combined entity metrics, and committing to quantified resource investments because they expect to honor those commitments. Extraction artists will offer cosmetic concessions, fight every meaningful protection, and retreat into ambiguous best efforts language because they intend to use the post closing flexibility to extract value back. The MedStack contrast illustrates the principle precisely. With Sally, MedStack negotiated for four months and accepted substantive structural protections, then operated as a genuine partner during the earnout period, allowing Sally’s strategic veto to block a value destroying platform consolidation in year one. With Buzz, MedStack negotiated quickly with charm and headline focus, accepted the standard extraction template without resistance, and then proceeded to pivot Lunar’s product roadmap toward a competing platform, manipulate the operational efficiency metrics, and subordinate his vendor note within ninety days. Same buyer, two different negotiations, two entirely different post closing behaviors. The negotiation revealed the intent.

Educational Disclaimer

The content of this assessment is provided for educational and informational purposes only. It does not constitute legal, financial, tax, valuation, or investment advice. All case studies and scenarios referenced are fictional and created from collective industry experience. The names used are inspired by real historical figures but represent fictional business owners with no connection to the actual persons, their families, or their estates. Consult qualified advisors for your specific situation. Neither the author nor YBAWS! accepts liability for actions taken based on this material.

YBAWS! (Your Business Ain’t Worth Sh*t!) is a trademark and educational platform dedicated to helping business owners understand corporate value and marketability.

© 2026 YBAWS! All rights reserved.