Terms Trump Price: How Aligned Incentives Build Real Wealth

The same $30 million headline can deliver $7.5 million or $40 million. The structure, not the price, determines which one you get

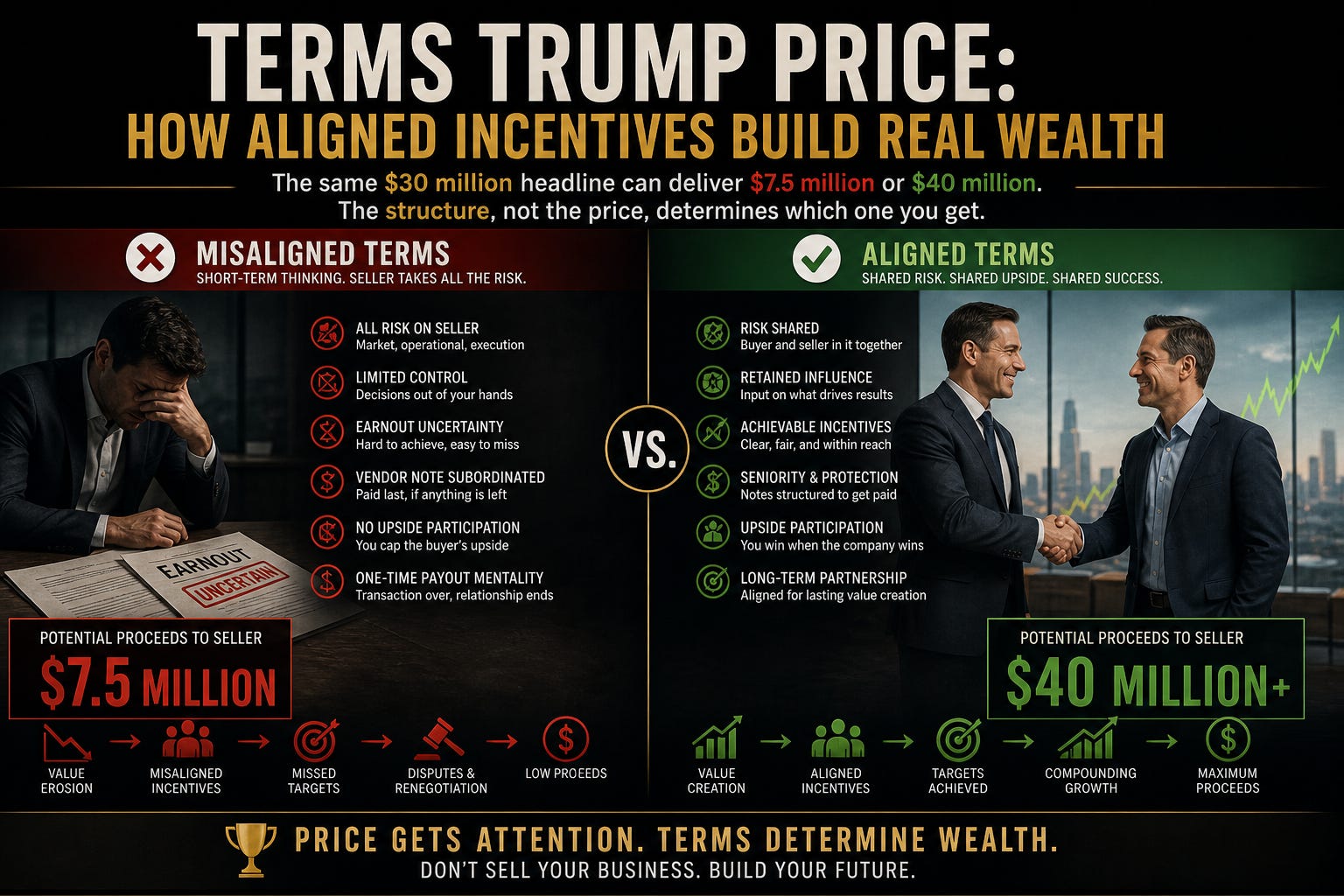

Two business owners. Same industry. Same revenue. Same headline offer of $30 million. One ends up with $7.5 million and a decade of regret. The other ends up with $40 million and a platform to build something bigger. The difference is not luck. The difference is how they structured the deal. Here is the playbook.

10 KEY TAKEAWAYS, ALIGNED INCENTIVE DEAL STRUCTURE

Terms determine outcomes more than price: The same headline can deliver dramatically different real value.

Aligned incentives convert earnouts from traps to partnerships: When both parties win or lose together, structure works.

Strategic veto power is non negotiable: If you cannot block major decisions, you cannot protect your earnout.

Resource commitments must be contractual and quantified: “Best efforts” language is not a protection, it is decoration.

Combined entity metrics beat isolated metrics: Earnout targets tied to overall performance reduce manipulation risk.

Continued equity participation is a value multiplier: Owning a piece of the bigger entity captures synergy upside.

A $15 million cash offer often beats a $30 million earnout: Run the risk adjusted present value math every time.

Build for cash sales, not earnout potential: Predictable revenue and operational independence command immediate cash.

The buyer’s negotiation behavior predicts post closing behavior: How they bargain on terms is how they will manage the business.

Sometimes the best exit is not exiting: Strategic partnerships can amplify capabilities and create generational value.

📚 READING PREREQUISITES

This post completes the Chapter 12 series. It assumes you have read Post 1 on earnout math and Post 2 on risk transfer mechanics.

Recommended Prior Reading:

The Adage That Decides Every Deal

There is a saying repeated in every M&A negotiation seminar and embedded in every transaction professional’s training: “You name the price, I name the terms. The one who names the terms usually wins.”

This adage exists because terms determine whether the price is real. A $30 million headline with the wrong structure delivers $7.5 million in actual value. A $25 million headline with the right structure delivers $35 million in actual value. The price is the marketing material. The terms are the deal.

Most sellers spend 90% of their negotiation energy on the headline number and 10% on the structure. Sophisticated sellers do the opposite. They accept a slightly lower headline in exchange for terms that protect actual value, and they walk away from higher headlines that come with structures designed to extract that value back through the back door.

The questions sophisticated sellers ask before they ask about price:

How much cash at closing, in absolute dollars, not percentage of headline?

What controls do I retain over operations, hiring, capital allocation, and strategic direction during the earnout?

Are earnout metrics tied to my isolated business unit, or to combined entity performance?

What are the minimum payment floors regardless of performance?

What contractual resource commitments has the buyer made?

What happens if the buyer changes strategy or pivots the business model?

The buyer’s reaction to these questions tells you more about the deal than any due diligence report. A buyer who negotiates substantively on these protections is signaling good faith. A buyer who fights every protection is signaling exactly how they will behave once you sign.

The Three Pillars of Aligned Incentive Structures

When earnouts and partnership structures are designed correctly, they convert from value extraction mechanisms into genuine value creation engines. The conversion requires three structural elements working together.

Pillar one, shared operational control. The seller retains meaningful authority over the operations whose performance determines the earnout. This typically takes the form of a CEO or president role with strategic veto power on major decisions. Without this, the seller is asking a competitor to score the seller’s own report card.

Pillar two, contractual resource commitments. The buyer makes specific, quantified, enforceable commitments to invest capital, allocate personnel, and provide strategic resources at agreed levels. “Best efforts” is not a commitment. “$15 million in incremental capital across years one through three, allocated as follows” is a commitment.

Pillar three, combined entity performance metrics. Earnout targets are tied to the performance of the combined business or business segment, not the isolated former company. This eliminates the buyer’s ability to manipulate transfer pricing, reallocate revenue, or starve the acquired business of resources to depress its standalone metrics.

When all three pillars exist, the earnout structure aligns rather than extracts. The buyer wins when the seller wins. The seller has tools to influence outcomes. The combined entity benefits from the seller’s continued contribution. This is the difference between partnership and exploitation.

Build for Cash, Then Negotiate for Partnership

The deepest lesson of Chapter 12 is that the negotiation begins long before the deal is on the table. The structure you can demand at the negotiation table is determined by the business you have built. Owners who build cash worthy businesses have negotiating leverage. Owners who do not, do not.

What makes a business cash worthy?

Recurring revenue that is predictable across multiple years and not concentrated in a few customers.

Operational systems that run without the founder’s daily involvement.

Documented processes that allow seamless ownership transfer.

Management depth that enables independent operation.

Diversified customer base with no single client over 15% of revenue.

Financial infrastructure that meets institutional buyer due diligence standards.

This is the YBAWS! valuation formula operationalized. Value equals Income divided by Required Rate of Return. A cash worthy business has a low required rate of return because the buyer can see, document, and quantify the absence of risk. That is the only foundation on which a seller can demand cash on closing.

When you have built a cash worthy business and the buyer wants you to accept an earnout, you have leverage. You can refuse. You can negotiate aligned incentive structures. You can demand strategic veto rights and resource commitments. You can walk away. Without that foundation, you cannot.

The flip side, when partnership beats exit. Sometimes the best deal is not an exit at all. A partnership with the right strategic acquirer can amplify capabilities, provide growth capital, and create equity participation in something larger than the standalone business. The same $30 million structure that extracts value in a bad faith deal creates generational wealth in a good faith partnership. The structure is the same. The intent is different. The negotiation reveals which is which.

The Permanent Lesson: Cash Is King

Strip away the spreadsheets, the legal language, and the strategic narratives, and the lesson of Chapter 12 reduces to a single sentence. Cash is king. Everything else is just expensive wallpaper.

Wallpaper looks impressive. It dresses up the room. It makes the headline number sound generational. But you cannot pay your mortgage with wallpaper. You cannot fund your retirement with wallpaper. You cannot send your grandchildren to college with wallpaper. You can only do those things with cash.

The earnouts that look like cash are not cash until they are deposited. The vendor notes that look like cash are not cash until they are paid. The contingent payments that look like cash are not cash until every condition has been met and every buyer interference has failed. Until then, they are wallpaper.

Build a business someone will pay cash for. Negotiate structures that protect the value you have built. Walk away from deals that transfer risk you cannot manage. And remember the adage that ends every M&A textbook ever written: you name the price, I name the terms, and the one who names the terms usually wins.

That is how you actually win.

💡 KEY TAKEAWAYS

Remember These Core Principles:

Terms trump price every time: The structure determines whether the headline is real.

Aligned incentives convert earnouts into partnerships: Three pillars, control, commitments, combined metrics.

Cash worthy businesses earn cash deals: The structure you can demand depends on what you have built.

The buyer’s behavior in negotiation predicts behavior post closing: Watch how they fight on protections.

Sometimes the best exit is partnership, not departure: Strategic alignment can multiply rather than extract value.

❓ FREQUENTLY ASKED QUESTIONS

Q: How do I know if a buyer is offering a genuine partnership or a disguised extraction? A: Test their willingness to commit contractually to specific, quantified resource investments and to combined entity performance metrics. Genuine partners will negotiate substantively. Extraction artists will offer cosmetic language and resist every meaningful protection. The negotiation reveals the intent.

Q: What is the minimum cash at closing percentage I should accept? A: This depends on the overall structure, but a useful benchmark is that cash at closing should at minimum cover your tax liability, your transaction costs, and your immediate post sale liquidity needs. Anything below that exposes you to financial harm if the contingent components fail.

Q: Can I negotiate continued equity participation in the acquiring entity? A: Yes, and you should consider it carefully. Continued equity participation aligns your interests with the acquirer’s success and can capture significant upside if the combined entity outperforms. It also locks you into the buyer’s decisions and exit timing, which is a meaningful trade off.

Q: What is the single most important question to ask before signing any earnout? A: “Who controls the levers that determine whether I receive these payments?” If the answer is the buyer, the earnout is risky. If the answer involves shared control with contractual protections, the earnout can work. If the answer is unclear, walk away.

Q: How long should the earnout period be? A: Shorter is generally better. Three years is standard. Five years is the upper bound for most situations. Anything longer compounds the probability of strategic shifts, market disruptions, and buyer behavior changes that destroy earnout achievement. Long earnouts favor the buyer almost universally.

🎯 READY TO BUILD A BUSINESS THAT COMMANDS CASH OFFERS?