The AI Valley of Death: Seed Funding Timelines Are Broken

AI startups need 24 months to validate products but seed rounds fund only 12. The temporal mismatch is killing promising companies before they can prove anything.

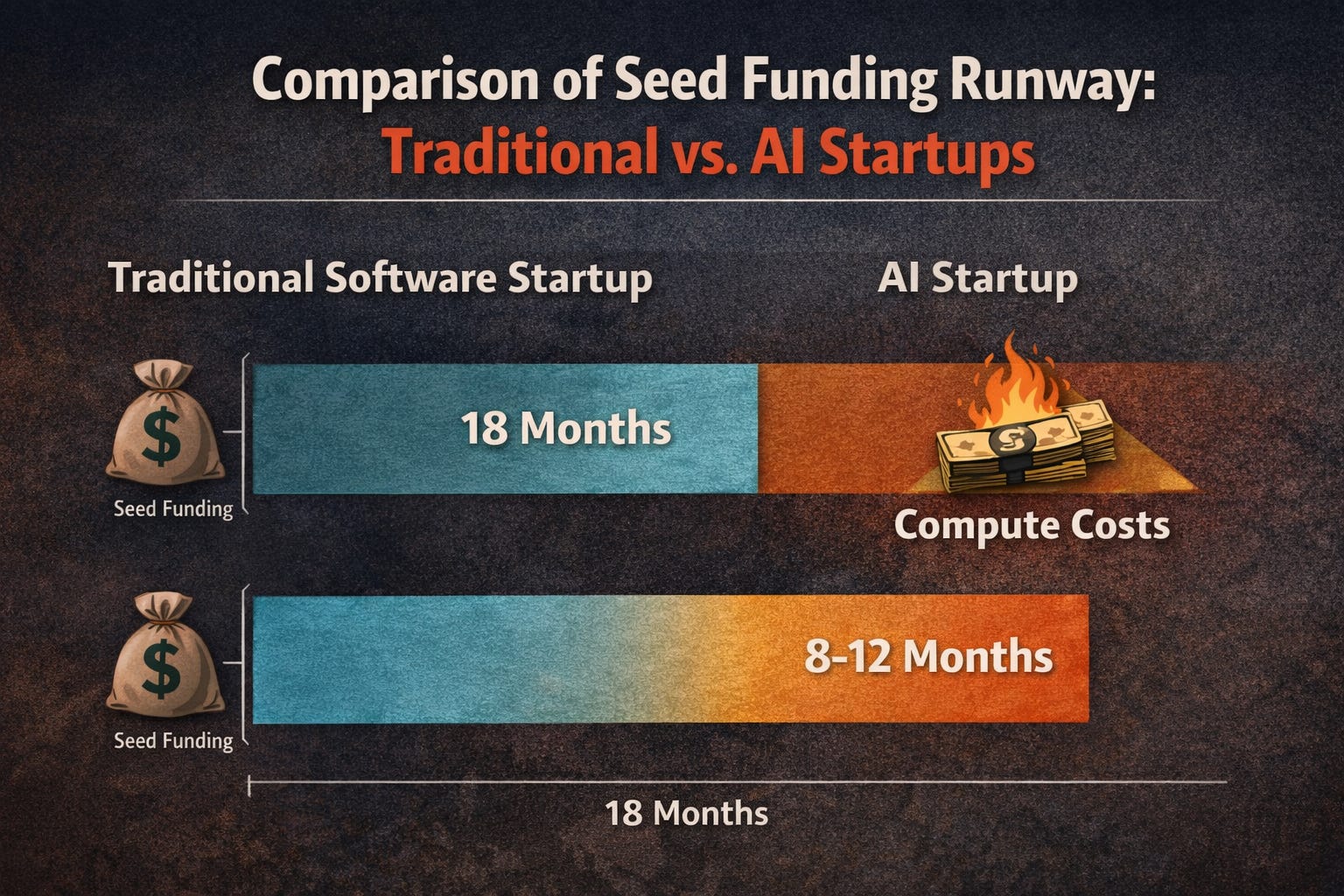

The funding gap between seed and Series A has always been brutal. AI just made it exponential. Traditional startups stretched seed capital for 18 months with lean principles. AI startups burn through runway in 8-10 months before they can prove anything. The valley of death just got a lot deeper. What changed?

10 KEY TAKEAWAYS - AI SEED FUNDING CRISIS

1. Temporal mismatch kills AI startups: AI product validation takes 18-24 months while seed rounds fund only 12-18.

2. Compute costs dwarf traditional burn: Training runs cost thousands per iteration versus zero for traditional software.

3. Traditional seed math is fiction: The assumption that $2-3M proves product-market fit fails for AI companies.

4. VC catch-22 traps founders: Achieving PMF requires capital VCs withhold until PMF is demonstrated.

5. Three impossible choices emerge: Massive dilution, underbaked products, or consulting distractions.

6. Model iteration costs compound: Each A/B test of a model variant costs what traditional startups spend monthly.

7. Talent costs accelerate burn: ML engineers command $500K+ packages before any revenue is generated.

8. Infrastructure scales before revenue: AI companies need $50K-$200K monthly compute before proving anything.

9. Seed investors remain unprepared: Traditional VCs evaluate AI startups using outdated SaaS frameworks.

10. Alternative structures are emerging: Revenue guarantees and milestone-based tranches address temporal mismatch.

📚 READING PREREQUISITES

This is the first post in the AI Startup Funding Series. It establishes foundational concepts that subsequent posts build upon: compute economics, talent concentration risk, and the structural mismatch between AI capital requirements and traditional venture funding.

Recommended Prior Reading:

• No prerequisites - this is the series introduction

• Series overview available at SaferWealth.com

The Traditional Valley of Death vs. The AI Abyss

For decades, the valley of death described that treacherous period after seed funding runs out but before Series A metrics materialize. Traditional startups could stretch seed capital for 18-24 months with lean principles and scrappy execution. They built an MVP for under $100K, validated with early customers, demonstrated unit economics, and showed a repeatable sales motion.

AI startups face a fundamentally different reality. Training runs, model iterations, and infrastructure costs create a funding curve that traditional venture math was never designed to handle. A single failed training run can cost thousands of dollars. Every A/B test of a model variant requires compute resources that would fund an entire engineering team at a traditional startup for a month.

The core problem is temporal mismatch. The time required to validate an AI product now exceeds the runway that seed funding provides. You need to iterate on models, which takes weeks or months per cycle. You need to accumulate enough data to make your AI actually useful. You need specialized ML talent commanding $500K+ annual compensation packages. And you need compute infrastructure that burns $50K-$200K monthly before you have generated a dollar of revenue.

Key Differences in AI Seed Economics:

• Traditional seed assumption: Demonstrate PMF in 12-18 months on $2-3M

• AI reality: 18-24 months just to reach production-quality models, requiring $4-6M

• The gap: By the time you can show Series A metrics, you have burned through Series A capital

• The outcome: Promising companies die not from execution failure but from runway exhaustion

The Cruel Mathematics of AI Product Validation

Consider what validation means for traditional versus AI startups. A SaaS company can validate product-market fit with 50-100 paying customers, $50K-$100K MRR, and clear unit economics. All achievable on seed capital. An AI company needs to prove their models work reliably, which requires thousands of inference calls, extensive testing across edge cases, and continuous improvement cycles.

The VC catch-22 is devastating. VCs say: show us product-market fit and we will lead your Series A. But achieving PMF for AI companies requires the capital VCs will not provide until you have demonstrated PMF you cannot achieve without the capital. It is a perfect deadlock.

By the time you have enough data to know if your AI actually works, your seed round is gone. The valley of death for AI companies is not about running out of money. It is about running out of time before you can prove anything meaningful.

Three Impossible Choices for AI Founders

The temporal mismatch creates three paths, none of them good:

Choice 1: Raise Massive Seed Rounds

Raise $5M-$10M at seed that looks more like Series A. Accept savage dilution of 25-40% before proving anything. This creates cap table problems that haunt you through future rounds. Plus, most AI companies cannot raise $8M seeds without proven traction, which is exactly the problem we are trying to solve.

Choice 2: Rush to Market

Launch with underbaked AI that disappoints customers and tanks retention. Customers expect ChatGPT-quality or better. If your product delivers mediocre AI because you could not afford proper model development, customers churn before you generate the revenue needed to improve the models. You are stuck in a local minimum.

Choice 3: Extend Runway Through Services

Try to extend seed runway through consulting or services. This distracts from core product development and signals desperation to Series A investors. The minute you start billing hours, you are no longer building a venture-scale company.

[IMAGE SUGGESTION: Three-path decision tree showing the impossible choices facing AI founders with outcomes for each path. Alt text: Decision tree diagram showing three funding paths for AI startups and their problematic outcomes]

Why Traditional Seed Investors Remain Unprepared

Traditional seed investors were not prepared for this dynamic. They are used to companies that can show meaningful traction on $2M. They price rounds assuming 18-month runways are sufficient. They evaluate progress using milestones designed for software companies where iteration costs approach zero.

When AI companies come back needing bridge rounds after 10 months because compute costs exceeded projections, investors feel betrayed. Where did the money go? To training runs that failed. To infrastructure that had to scale before revenue existed. To ML talent you could not build without.

Market Adaptation Remains Insufficient:

• Some seed investors now write $5M-$8M initial checks, effectively merging seed and Series A-1

• Some use milestone-based tranches, releasing capital as technical progress happens

• Some require early enterprise contracts before releasing full seed amounts

• These remain band-aids on a structural problem

The Real Question VCs Must Answer

How do you fund the commercialization stage when the capital requirements now resemble Series B, but the risk profile still looks like seed? Traditional VC structures assume risk decreases as capital increases. With AI companies, capital requirements increase while risk remains stubbornly high. You can burn $5M and still not know if you have product-market fit.

Until funding structures evolve to match AI companies’ actual development timelines and capital needs, the valley of death will continue claiming promising startups that simply ran out of runway before they could prove anything. The companies that survive are not necessarily the best. They are the ones that happened to raise enough capital upfront, got lucky with early hyperscaler compute credits, or had founders willing to accept brutal dilution.

For founders entering this landscape: understand that the old seed playbook does not work. You are not building a lean startup. You are building a capital-intensive research project that needs to become a business. Price your seed round accordingly, or accept that you are gambling on finding bridge capital when the traditional seed timeline proves insufficient.

💡 KEY TAKEAWAYS