Multiple Choice Questions

1. What is the “control paradox” at the heart of earnout structures?

A. Sellers retain operational control but lose financial upside B. Buyers bear the risk while sellers keep the rewards C. Sellers bear the risk while buyers control every operational lever D. Both parties share control equally during the earnout period

2. What term describes a buyer’s pattern of making technically legal business decisions that systematically prevent earnout achievement?

A. Material breach B. Soft default C. Anticipatory repudiation D. Constructive termination

3. In the typical capital structure priority queue, where does a seller’s vendor note rank?

A. Senior to bank debt B. Senior to institutional lenders but junior to banks C. Junior to senior secured debt, institutional lenders, and trade creditors D. Equal in priority to trade creditors

4. What interest rate range is typical for vendor financing notes, and why is it economically problematic for sellers?

A. 10% to 12%, problematic because it creates payment burden for the buyer B. 4% to 6%, problematic because it does not compensate for unsecured credit risk C. 8% to 10%, problematic because it triggers tax disadvantages D. 15% to 18%, problematic because it disincentivizes timely buyer payments

5. In the Valentina Tereshkova Holloway case study, what was the size of the senior credit facility that subordinated her vendor note shortly after closing?

A. $24 million B. $52 million C. $87 million D. $120 million

6. What was the total amount Valentina had realized from her $11 million headline deal as of the case study’s reporting date?

A. $4.85 million B. $7.20 million C. $9.40 million D. $11.00 million

7. Which clause in Valentina’s purchase documents allowed Apex to subordinate her vendor note to future senior debt?

A. A material adverse change clause B. A clause permitting subordination to future senior credit facilities entered in the ordinary course of business C. A change of control provision D. An accelerated payment trigger

8. What event caused the COVID era earnout collapse described in the chapter?

A. Buyer breaches of operational covenants B. Seller failures to meet performance targets C. Exogenous market shocks that landed entirely on the seller because the contract had transferred market risk D. Regulatory actions invalidating earnout structures

9. Which type of professional advisor failed Valentina during the document review stage?

A. A specialized M&A attorney B. A chartered business valuator C. A generalist lawyer who had drafted her divorce settlement D. An institutional banker

10. According to the chapter, what is the most reliable predictor of how a buyer will behave during the earnout period?

A. The buyer’s industry reputation B. The buyer’s negotiation behavior on structural protections C. The buyer’s financial statements D. The buyer’s stated mission and values

Explanation Questions

Question 1. Define the control paradox in earnout structures and explain why sellers consistently underestimate it during deal negotiation. Use specific examples from the Valentina Tereshkova Holloway case study.

Question 2. Describe four specific buyer actions that constitute soft defaults, meaning actions that destroy earnout value without breaching the contract. Explain why each is legally defensible despite its economic effect.

Question 3. Explain why a vendor note carrying 5% interest is economically inadequate compensation for the credit risk a seller bears. Use the priority queue, subordination mechanics, and Valentina’s outcome to support your analysis.

Question 4. Identify three structural protections Valentina could have negotiated into her deal that would have materially reduced her risk exposure, and explain how each protection would have changed her outcome.

Question 5. Explain the difference between a generalist lawyer and an M&A specialist in the context of transaction document review. Why is this distinction often the difference between a successful and a failed deal outcome for the seller?

Multiple Choice Answer Key

C. Sellers bear the risk while buyers control every operational lever. This asymmetry is the defining feature of poorly structured earnouts and the primary mechanism by which contingent value gets destroyed.

B. Soft default. A soft default occurs when the buyer manages the business in ways that suppress earnout achievement without violating any contractual provision, leaving the seller with no enforceable remedy.

C. Junior to senior secured debt, institutional lenders, and trade creditors. Vendor notes typically sit at or near the bottom of the capital structure, often recovering pennies on the dollar in distressed scenarios.

B. 4% to 6%, problematic because it does not compensate for unsecured credit risk. These rates approximate government bond yields, but vendor notes carry equity-like risk, creating a fundamental mispricing that favors the buyer.

C. $87 million. Apex Industrial Holdings refinanced with an $87 million senior credit facility shortly after closing, which subordinated Valentina’s vendor note to a position behind the entire senior obligation.

A. $4.85 million. Valentina’s total realization through the case study reporting date was approximately $4.85 million, with $3.71 million still sitting on a suspended subordinated vendor note.

B. A clause permitting subordination to future senior credit facilities entered in the ordinary course of business. This clause was buried in the original purchase documents and not flagged during legal review.

C. Exogenous market shocks that landed entirely on the seller because the contract had transferred market risk. The COVID period demonstrated that whatever specific shock occurs, the earnout structure routes the consequences to the seller’s side of the balance sheet.

C. A generalist lawyer who had drafted her divorce settlement. The lawyer was competent in domestic matters but lacked the M&A specialization required to identify the structural risks embedded in the transaction documents.

B. The buyer’s negotiation behavior on structural protections. How a buyer fights or accepts protections during the deal is the most reliable signal of how they will manage the business after closing.

Explanation Question Solutions

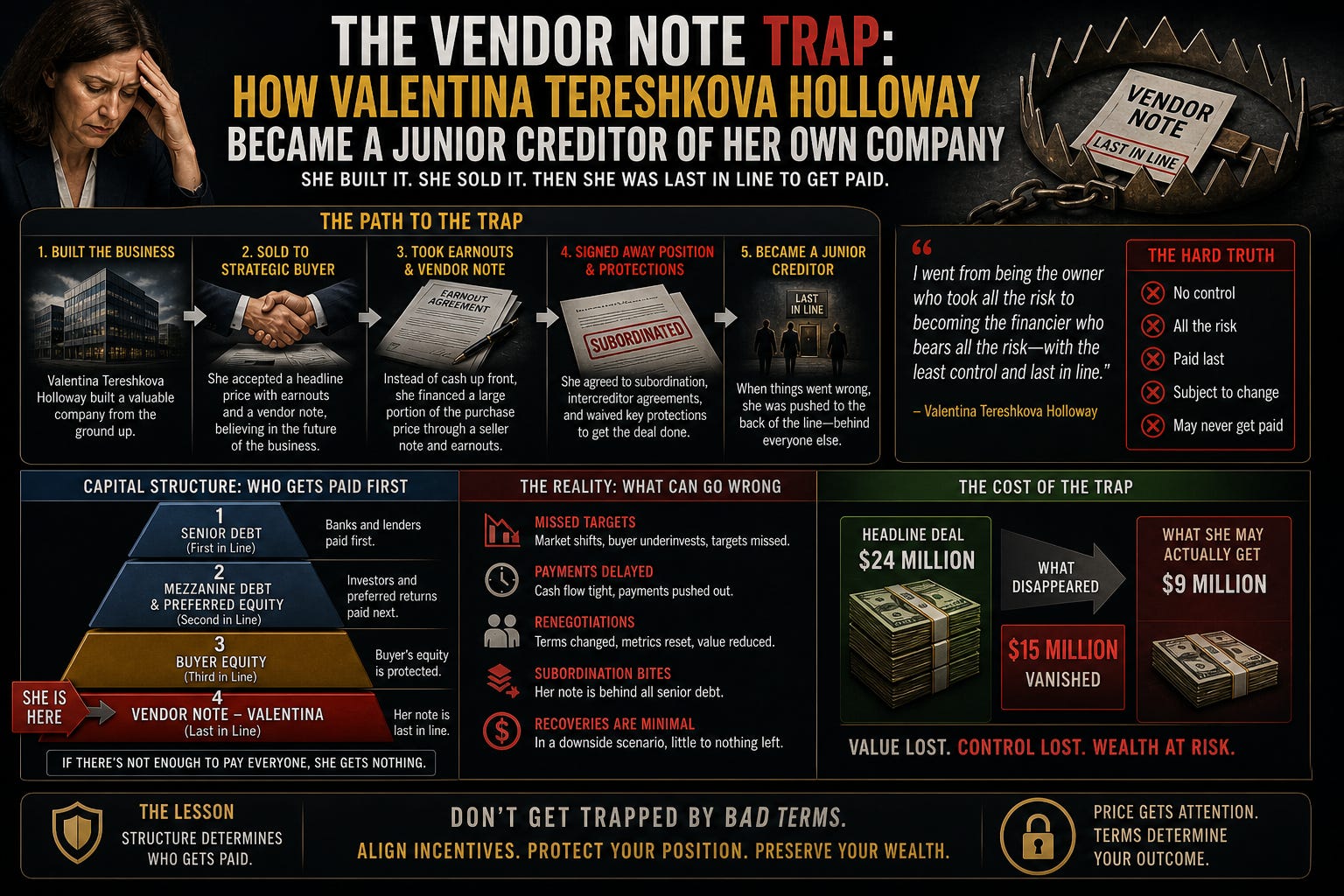

1. The control paradox describes the structural reality that an earnout makes the seller financially responsible for outcomes the seller cannot control, while granting the buyer complete operational authority to determine those outcomes. Sellers underestimate it because their entrepreneurial confidence convinces them they can navigate any management environment, and because their emotional commitment to the deal blocks dispassionate evaluation of buyer incentives. Valentina’s case study illustrates the paradox precisely. Apex made every operational decision that determined her earnout: warehouse consolidation, inventory redistribution, personnel terminations, and strategic redirection. Valentina bore every consequence, including a 19% standalone revenue collapse, a year two earnout of zero, and the destruction of customer relationships she had built over twenty two years. She had no contractual right to influence any of those decisions because the sale had transferred operational authority to Apex while leaving the financial risk with her.

2. Four specific buyer actions that constitute soft defaults: First, redirecting resources to other portfolio companies, defensible because the buyer has fiduciary obligations to optimize the broader portfolio rather than maximize one acquired entity’s earnout. Second, delaying product launches whose timing would benefit the seller’s earnout calculation, defensible because product timing is a strategic business judgment within management discretion. Third, implementing hiring freezes during periods when the earnout requires growth, defensible because workforce planning falls within ordinary management authority and may be required by senior debt covenants. Fourth, reassigning key personnel to other strategic priorities, defensible because personnel allocation is a fundamental management prerogative. Each action is legally defensible because the purchase agreement transferred the authority to make these decisions to the buyer. The seller’s only recourse is a “best efforts” or “good faith” claim, which courts rarely enforce against documented business judgment.

3. A vendor note at 5% interest is inadequate compensation because the rate approximates government bond yields while the underlying risk profile resembles unsecured equity. The capital structure priority queue places vendor notes behind senior secured lenders, institutional lenders, and trade creditors, meaning that in distressed scenarios the vendor note holder recovers last and often recovers nothing. Subordination mechanics compound the problem because clauses permitting future subordination to new senior facilities allow the buyer to push the vendor note further down the priority queue without seller consent, as Valentina experienced when Apex refinanced into an $87 million senior facility. The proper risk adjusted yield for an unsecured, subordinated, illiquid note to a leveraged acquirer should be in the 12% to 15% range, not 5%. Valentina’s $3.71 million suspended balance, sitting indefinitely behind senior debt, illustrates the pricing failure with brutal clarity.

4. Three structural protections that would have changed Valentina’s outcome. First, an explicit prohibition on future subordination of the vendor note without seller consent. This single clause would have prevented the $87 million senior refinancing from pushing her note to the bottom of the queue and would likely have preserved her quarterly payment stream. Second, a minimum payment floor on the earnout, payable regardless of performance, set at perhaps $1 million per year for the three earnout years. This would have converted $3 million of contingent value into deferred but certain value, dramatically improving the risk adjusted present value of the deal. Third, contractual resource commitments requiring Apex to maintain Skyward’s Cincinnati warehouse operations, customer relationships, and key personnel for at least the duration of the earnout period. This would have prevented the operational rationalization that caused the 19% standalone revenue collapse. Combined, these three protections would have likely doubled Valentina’s realized outcome.

5. A generalist lawyer reviews documents for general legal compliance, contract enforceability, and obvious red flags. An M&A specialist reviews the same documents for the structural mechanics of risk allocation, subordination dynamics, earnout manipulation pathways, and the dozens of standard clauses that look innocuous individually but combine to transfer value from seller to buyer. The clauses that destroyed Valentina’s deal were standard. They appear in most M&A purchase agreements. A generalist sees standard language and accepts it. A specialist sees standard language and recognizes it as the mechanism by which the buyer will extract value back through the back door after closing. The distinction is often the difference between a $4.85 million outcome and a $9 million outcome on the same headline deal, which represents a return on legal fees of 50 to 100 times the cost differential between generalist and specialist counsel.

Educational Disclaimer

The content of this assessment is provided for educational and informational purposes only. It does not constitute legal, financial, tax, valuation, or investment advice. All case studies and scenarios referenced are fictional and created from collective industry experience. The names used are inspired by real historical figures but represent fictional business owners with no connection to the actual persons, their families, or their estates. Consult qualified advisors for your specific situation. Neither the author nor YBAWS! accepts liability for actions taken based on this material.

YBAWS! (Your Business Ain’t Worth Sh*t!) is a trademark and educational platform dedicated to helping business owners understand corporate value and marketability.

© 2026 YBAWS! All rights reserved.