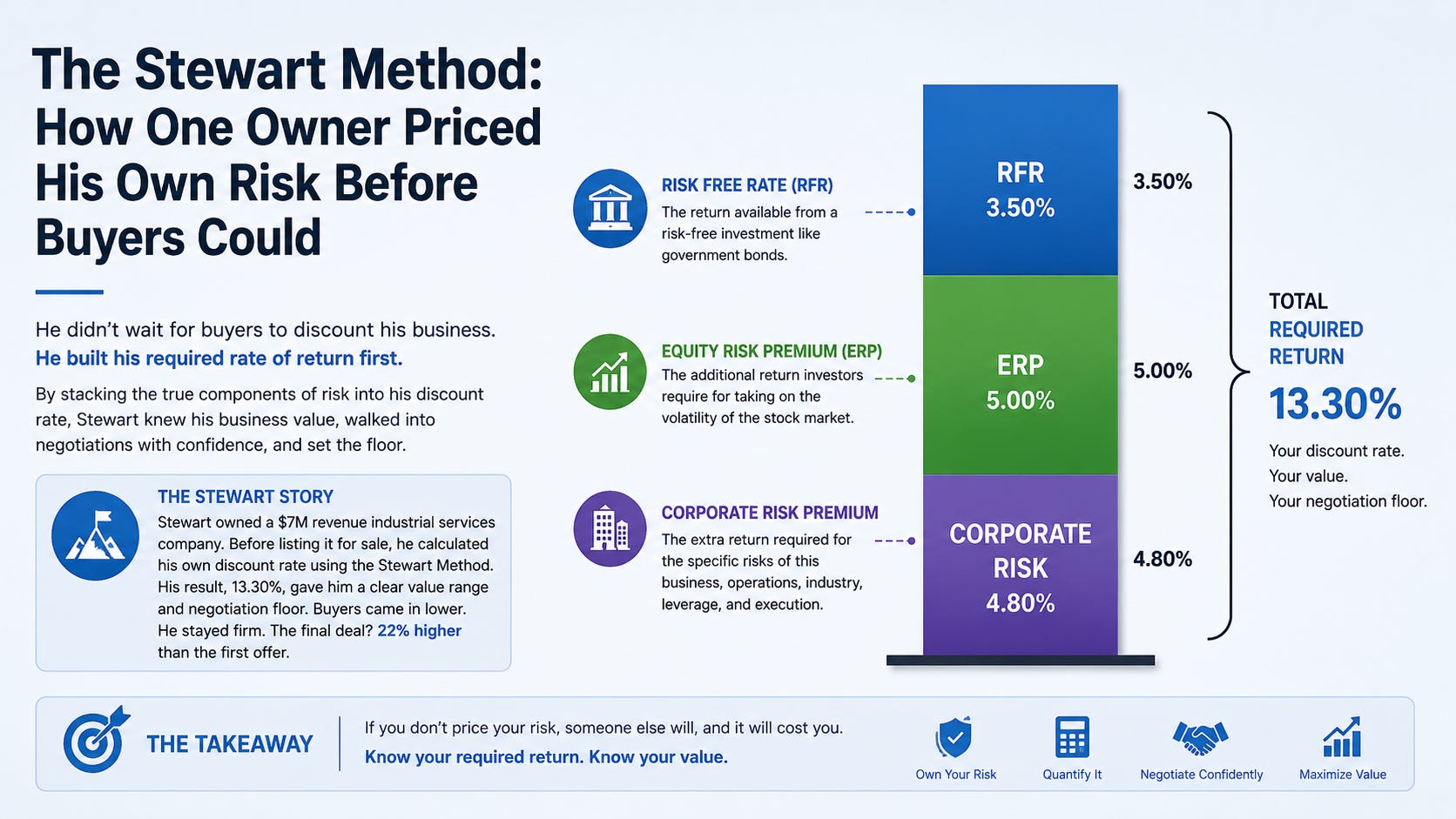

Disclaimer: The following case study is entirely fictional. The character name is inspired by a legendary Formula 1 driver but represents a fictional individual with no connection to that real person, their family, or their estate. Financial figures are illustrative only.

Jackie Stewart Ashford built Ashford Precision Components over twenty two years into a respected supplier of machined parts for industrial equipment manufacturers. By the time he decided to explore an exit, the company generated $9 million in revenue and $2 million in EBITDA. Jackie assumed, like most owners, that a healthy profit line meant a healthy price. He had heard competitors “went for 6x,” so he anchored on a $12 million number and started interviewing advisors.

The first advisor to earn his trust did something Jackie did not expect. Instead of celebrating the profit, she asked him to price his own risk before any buyer did it for him.

The Required Return Reality

She started with the recipe. The risk free rate that quarter sat near 4%, drawn from ten year government bonds. The equity risk premium, referencing Damodaran’s published data, was running around 5.5%. That gave a market baseline near 9.5%, which she rounded to 10% for clean illustration.

“Everything above that 10%,” she explained, “is corporate risk, and corporate risk is the only ingredient you can actually change.”

Then she walked Ashford Precision through its company specific premium. Jackie personally approved every quote above $50,000. His two largest customers represented 55% of revenue with no long term contracts. Processes lived in the heads of three senior machinists nearing retirement. Financial reporting was reactive, produced by an external bookkeeper months after quarter end.

Her assessment, for illustration only, stacked up like this:

• Management and key person risk, 8%

• Customer concentration risk, 6%

• Operational and process risk, 4%

• Financial reporting risk, 3%

Total company specific risk premium, 21%. Added to the 10% market baseline, Ashford Precision carried a 31% required return, which translated to a multiple of roughly 3.2x, since 1 divided by 0.31 is about 3.2. On $2 million EBITDA, that math produced a defensible value near $6.4 million, not the $12 million Jackie carried in his head.

The Reckoning

Jackie was, in his own words, insulted. He had expected the advisor to argue his multiple up, not cut it nearly in half. She held her ground with the math. “A buyer is not paying for your profit,” she told him. “A buyer is paying for the probability that your profit survives without you. Right now that probability is low, and the price reflects it.”

She framed the choice the way this chapter frames it. Jackie could spend the next eighteen months chasing revenue growth, or he could spend it shrinking the 21% premium. A racing man by temperament, Jackie understood the analogy immediately. The fastest driver is not the one who ignores risk, it is the one who measures every corner and manages it. He chose to manage his corners.

The De Risking Program

Over the following eighteen months, Ashford Precision attacked each risk category deliberately, applying systems thinking and multiplier logic rather than a growth at all costs mindset.

On management depth, Jackie hired an operations manager, promoted a senior estimator into a quoting role, and documented an approval matrix so quotes no longer routed through him alone. On customer concentration, he formalized supply agreements with his two largest accounts, added three mid sized customers through a modest outbound sales effort, and set an internal policy capping any single customer at 20% of revenue. On process, he documented setup sheets and quality checklists for every recurring part, cross trained the machinists, and captured tribal knowledge before retirements could erase it. On financials, he engaged a fractional controller who delivered monthly statements, cash flow forecasts, and variance analysis.

The investment across personnel, systems, and advisory support totaled roughly $350,000 over eighteen months.

The New Math

When the advisor reassessed, the transformation was visible in the premium, not merely the profit. For illustration:

• Management and key person risk fell from 8% to 3%

• Customer concentration fell from 6% to 2%

• Operational risk fell from 4% to 2%

• Financial risk fell from 3% to 1%

The company specific premium dropped from 21% to 8%. Added to the 10% baseline, the required return fell to 18%, lifting the multiple to roughly 5.5x, since 1 divided by 0.18 is about 5.5. Meanwhile EBITDA had grown modestly from $2 million to $2.3 million as the tighter operation shed waste.

New indicative value: $2.3 million EBITDA multiplied by 5.5x, roughly $12.65 million.

Jackie had nearly doubled his company’s value, not by doubling revenue, but by pricing and then shrinking his own risk before a buyer used it against him. On a $350,000 investment, the value lift of roughly $6.25 million represented a return of about 1,785%. When a strategic buyer eventually cited Ashford’s “institutional stability” as justification for a premium, Jackie finally understood. He had stopped being the driver the company could not race without, and had become the team principal who built a machine that ran without him. For the mechanics behind key person discounts, William Buck’s overview of key person risk and Wall Street Prep on customer concentration map closely to what Jackie lived.