Part 1 of 3: The Broken VC Model

The venture capital model is broken. Not catastrophically, but quietly, burning out founders through endless equity dilution and leaving angel investors wondering why 90% of their portfolio flatlines. Traditional seed rounds and Series A financing force founders into valuation fights on day one, surrender 20-40% equity, and trap investors in binary outcomes. This is Part 1 of our three-part series examining what’s wrong with venture capital and introducing a fundamentally different approach: the VC Risk Swap.

Key Takeaways: Part 1

Traditional venture capital forces founders into valuation disputes before proving product-market fit

Founders can own just 15% by Series B due to cumulative equity dilution

90% of traditional startup investments fail, creating power law returns

The 18-month sawtooth financing cycle turns businesses into perpetual fundraising machines

The reverse acqui-hire scenario devastates investors while big companies acquire talent

Series Navigation

Part 1: Venture Capital is Dangerous

Part 2: Venture Capital is Safe

Part 3: Venture Capital is Working

The Founder’s Nightmare: Fighting for Your Own Company

Valuation Warfare Before Product-Market Fit

You’ve built something real. Maybe you’re pre-revenue but commercial ready, or generating early traction ready to scale. You need growth capital, so you begin the fundraising dance.

The first problem hits immediately: pre-money valuation. Every pitch deck ends with the same awkward conversation. You think your startup is worth $10M. The VC thinks $3M. Both know the number is essentially fiction, yet you’re surrendering 20-40% of your company based on it.

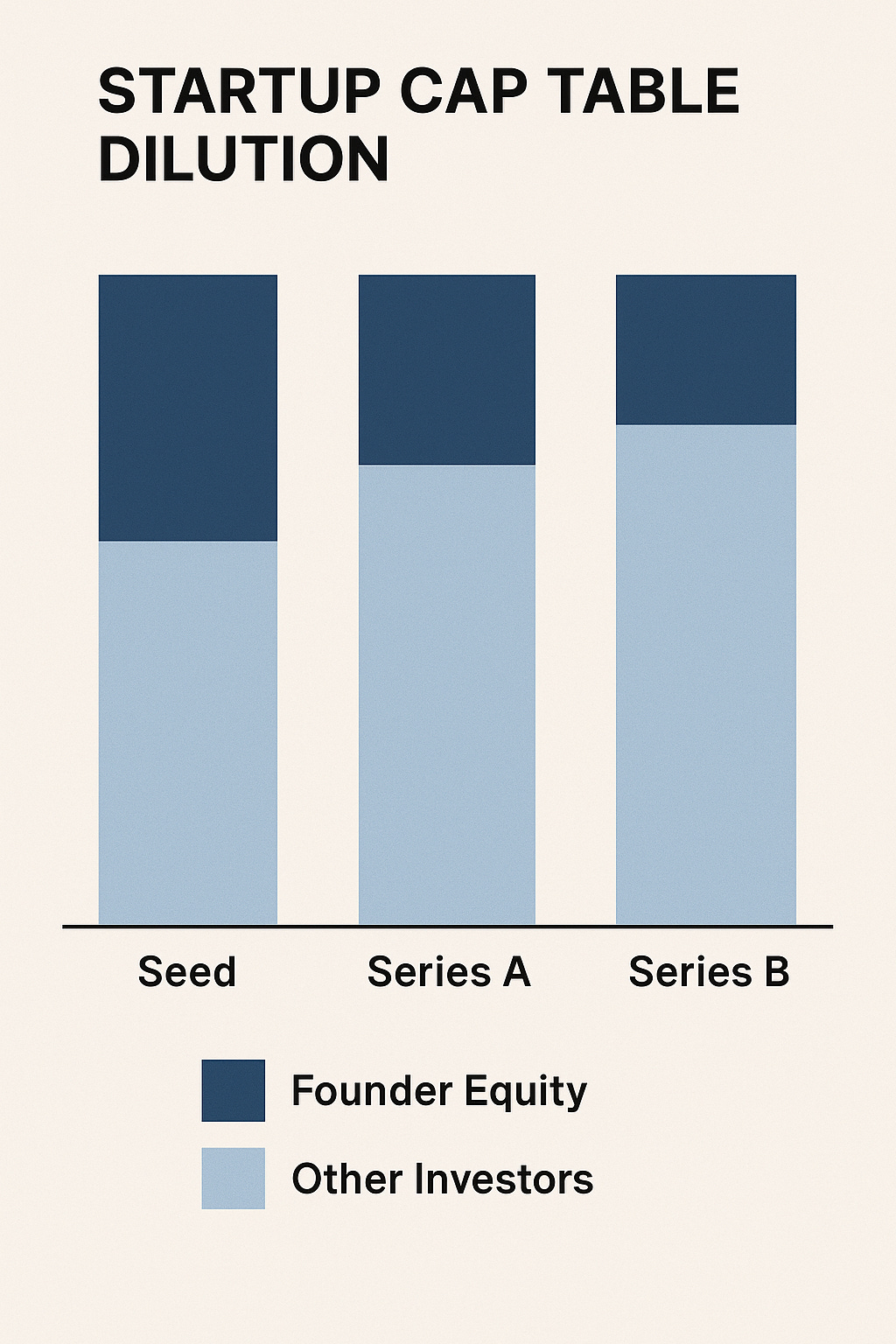

The Dilution Death Spiral

Then comes equity dilution, the slow-motion surrender of your company:

Seed round: Give up 25% for initial capital

Series A: Another 20-25% to scale operations

Series B: An additional 15-20% to achieve growth targets

Result: You now own 15% of what you built

The cap table transforms into a minefield featuring liquidation preferences, anti-dilution provisions, participating preferred stock, and voting rights that override your strategic vision. Board composition shifts from founder-controlled to investor-dominated.

The 18-Month Fundraising Hamster Wheel

Sawtooth financing creates an exhausting cycle: raise a round, deploy capital over 18-24 months, begin fundraising again before runway expires, repeat indefinitely. The actual business becomes secondary to hitting KPIs that justify the next round’s valuation. Your burn rate climbs, runway shrinks, and down rounds crater perceived value.

Term sheets arrive laden with restrictive covenants. Your exit strategy gets dictated by investors’ fund lifecycles, not your company’s optimal trajectory.

The Investor’s Headache: Power Law Gambling Without Protection

The Brutal Math of Traditional Venture Investing

You’re an accredited investor, perhaps managing a family office or angel syndicate. You want startup exposure and alternative investments beyond public markets.

Traditional venture investing offers brutal economics: portfolio diversification requires 20-30 companies minimum, 90% of equity stakes return zero, you’re gambling on power law returns where one unicorn pays for all failures, and no downside protection exists.

The due diligence process exhausts resources while providing no guarantees. You’re assessing market opportunity, go-to-market strategy, unit economics, customer acquisition cost (CAC), and lifetime value (LTV), yet can’t predict success.

Standard venture investments offer zero structural protection: capital deployment with no safeguards, subordination to creditors, complete wipeout in acqui-hire scenarios, holding periods stretching 7-10 years, minimal secondary markets for early-stage equity, and liquidity events that may never materialize.

The Reverse Acqui-Hire: When “Success” Means Total Loss

![Reverse acqui-hire flow, Alt text: Reverse acqui-hire transaction showing investor value destruction]

The Nightmare Scenario Traditional VC Can’t Solve

Let’s examine the reverse acqui-hire: You’ve built legitimate technology and developed intellectual property (IP). You’ve generated revenue but struggle to scale. Product development costs exceed projections. A larger company approaches wanting your team, not your product. They “acquire” the company but let the corporate entity die.

The acquisition price barely covers liabilities. The liquidation preference stack means common shareholders get nothing. Angel investors and seed-stage investors are wiped out. Protective provisions protect nobody.

Winners: Large company acquires engineers below market cost; founders get jobs.

Losers: Early investors receive tax write-offs; common shareholders get zero; years of innovation produces no shareholder value.

This pattern has become standard in deep tech, biotech, and capital-intensive sectors. Traditional venture capital actively incentivizes this value-destroying outcome.

What Comes Next

We’ve examined fundamental problems with traditional venture capital: valuation warfare forcing premature decisions, dilution spirals stripping founder control, the fundraising hamster wheel, power law gambling destroying investor capital, and reverse acqui-hires benefiting only acquirers.

In Part 2, we’ll introduce the VC Risk Swap, a fundamentally different capital structure eliminating these problems. You’ll learn how this approach sidesteps valuation fights, preserves founder equity, provides patient capital over 5+ years, and offers actual downside protection for investors.

About the Author

Sean Cavanagh, BAS, CPA, CA, CF, CBV

With over three decades negotiating business sales and conducting valuations, Sean delivers unvarnished truth about business exits. Starting at Deloitte and Canada Revenue Agency, he now advises business owners through his M&A practice. YBAWS! reflects his frustration with owners who consistently overvalue their companies.

Do Your Own Research

Venture Capital & Startup Financing:

Feld, Brad, and Jason Mendelson. Venture Deals: Be Smarter Than Your Lawyer and Venture Capitalist. 4th Edition, Wiley, 2019

Graham, Paul. Y Combinator Essays on Startup Funding. 2005-2023

Kaplan, Steven N., and Per Strömberg. “Financial Contracting Theory Meets the Real World: An Empirical Analysis of Venture Capital Contracts.” The Review of Economic Studies, vol. 70, no. 2, 2003

Startup Ecosystem Studies:

CB Insights: The Top 20 Reasons Startups Fail. 2023 Analysis Report

National Venture Capital Association (NVCA): Venture Capital Yearbook Data. 2020-2024

PitchBook: Venture Capital Valuations Report. Q1-Q4 2024

Startup Failure & Acqui-hire Analysis:

TechCrunch: The Acqui-hire Phenomenon - Analysis of Tech Talent Acquisitions. 2015-2024

Eisenmann, Tom, et al. “Why Startups Fail: A New Roadmap for Entrepreneurial Success.” Harvard Business Review, 2021

Connect

Web: SaferWealth.com - Alternative Startup Funding Structures

Video: Rumble @SaferWealth - VC Risk Swap Educational Content

LinkedIn: LinkedIn @SaferWealth - Startup Finance Innovation

Disclaimer

This information is for educational purposes only and does not constitute legal, tax, accounting, or investment advice. The VC Risk Swap structure involves complex legal and tax considerations. Consult qualified professionals before making any investment or financing decisions.

YBAWS! Your Business Ain’t Worth Sh#t is a reader-supported publication.

Subscribe Now | Continue to Part 2 | Visit SaferWealth.com

Last Updated: January 2025

Copyright: © 2025 Safer Wealth. Educational use permitted with attribution.