The Wealth Multiplication Effect

How Competitive Sale Processes Create Generational Wealth. The difference between a restricted sale and a proper auction process isn’t measured in percentages. It’s measured in multiples.

A business owner had an $8 million deal on the table. His biggest competitor. Clean, simple, done. He almost took it. Eighteen months later, a European buyer paid $14.5 million for the exact same company. The business didn’t change. The process did. That $6.5 million difference has a name: the competitive sale premium.

10 KEY TAKEAWAYS, THE WEALTH MULTIPLICATION EFFECT

Competition multiplies, negotiation incrementalizes: A proper auction process doesn’t add to your sale price, it multiplies it. One buyer negotiates. Multiple buyers compete.

Different buyers have different math: Your competitor values what he can eliminate. Private equity values IRR and exit multiples. International buyers value strategic positioning. None of them use the same denominator.

The same business is worth different amounts to different buyers: Chapter 6’s formula, Value = Income ÷ Required Rate of Return, produces different answers for every buyer category because each buyer carries a different risk perception.

Unidentified intangible assets allow buyers to underpay: If your purchase price allocation leaves value unassigned, the buyer didn’t overpay, you underidentified.

The $8M to $14.5M gap is not extraordinary: It is the normal outcome of a properly structured competitive sale process versus a direct-to-competitor transaction.

International buyers pay for what domestic buyers already have: Distribution channels, technology advantages, market entry, and currency arbitrage all drive premiums that local competitors have no reason to pay.

PE buyers with deployment mandates will stretch: A private equity fund with a $200M deployment mandate and a timeline is not a patient negotiator.

The emotional cost of leaving money behind is permanent: Owners who close restricted deals spend years haunted by what the competitive process would have produced.

Goodwill is real money hiding in plain sight: The $62M goodwill in the TechCorp/DataSoft case study wasn’t invented, it was identified. Identification is your job. Letting buyers identify it for you is expensive.

This post proves the math: Three buyer scenarios, one business, radically different prices, and a real case study showing exactly how it happens.

📚 READING PREREQUISITES

This post builds on foundational YBAWS! concepts. Full comprehension requires prior posts. Key terms and formulas are revisited deliberately to reinforce how they compound.

Recommended Prior Reading:

Chapter 6: The Fundamental Valuation Formula, Value = Income ÷ Required Rate of Return

Chapter 8 Post 1: Open Your Borders, Why Restricting Your Buyer Market Costs You Millions

Why the Same Business Is Worth Four Different Prices

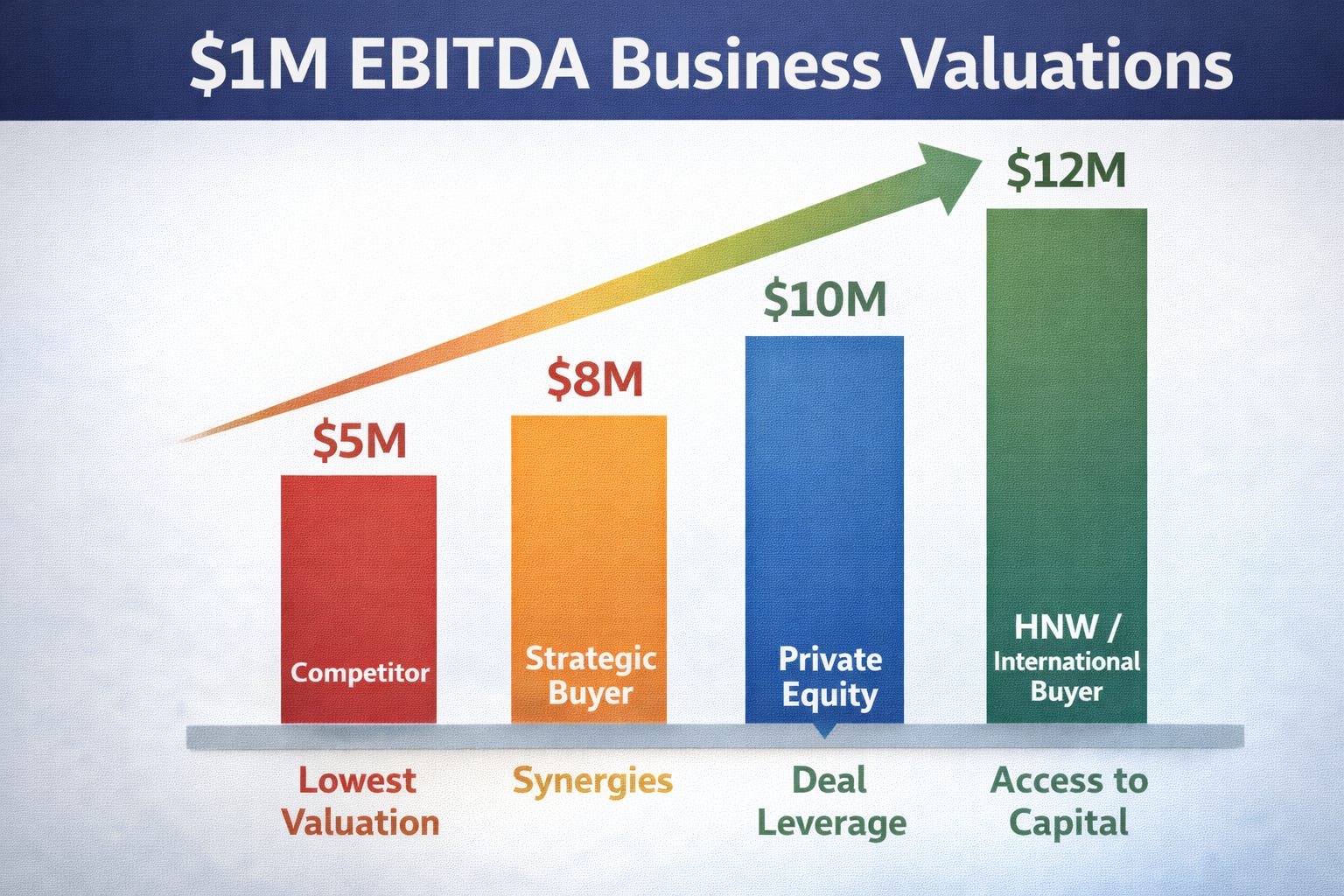

Consider this scenario. Your business generates $1M in EBITDA consistently. Here’s what it might be worth to four different buyers:

Largest competitor: $5M, calculates synergies based on cost eliminations, applies a high required return because he knows the integration risk intimately

Strategic buyer in adjacent industry: $6M, values market access and customer relationships he doesn’t currently have

Private equity group seeking a platform acquisition: $8M, values stable cash flow as a financial instrument with consolidation upside priced into a portfolio IRR

International acquirer seeking market entry: $12M, values the years it would take to build what you already have, in a currency stronger than yours

You’ll never find out which is true unless you open the doors. And you’ll never maximize any of these numbers unless they’re all competing simultaneously.

This is the direct application of Chapter 6’s core formula. Value = Income ÷ Required Rate of Return. Each buyer type carries a fundamentally different required rate of return based on their specific risk perception, strategic need, and capital cost. Same income. Dramatically different denominators. Dramatically different values.

The Case Study: $8M to $14.5M

A client had convinced himself that selling to his largest competitor was the only logical path. “They know the business,” he said. “It makes sense to them.” He was ready to close at $8 million.

He was persuaded, with significant resistance, to run a proper competitive process instead. Eighteen months later, a European buyer paid $14.5 million for the same business. No material changes to operations. No revenue growth that justified the gap. The difference was pure competitive process premium, and the specific fact that the European buyer was purchasing distribution infrastructure his competitor already had in place. And paying in Euros.

That $6.5M difference is: