Two Pilots, Two Deals, Two Outcomes: Case Study

Sally Ride Marchetti vs Buzz Aldrin Castellanos

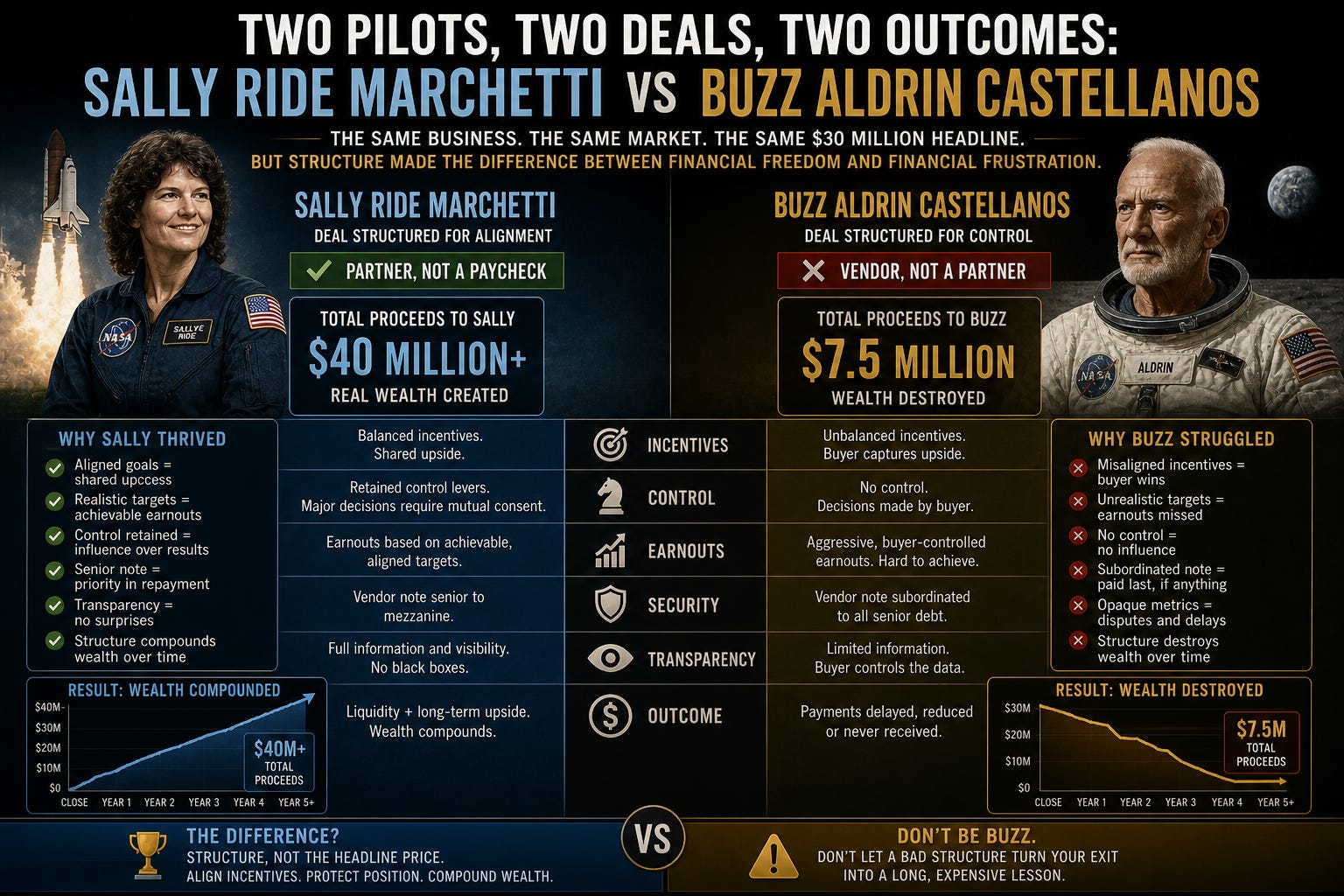

Sally Ride Marchetti and Buzz Aldrin Castellanos ran nearly identical businesses. Both had built specialty SaaS platforms serving mid market healthcare administrators. Sally’s company, Apogee Patient Systems, generated $7.8 million in annual revenue. Buzz’s company, Lunar Health Workflow, generated $7.5 million. Both had been founded around the same time. Both had EBITDA margins in the mid 20% range. Both attracted the attention of MedStack Holdings, a private equity backed healthcare technology consolidator, in the same calendar quarter of 2023.

MedStack offered both founders the same headline number: $32 million.

Sally walked away with $39 million in realized value. Buzz walked away with $9.4 million. The difference was not luck. The difference was structure.

Buzz’s Structure: The Extraction Template

Buzz’s deal looked like every cautionary tale in Chapter 12.

$5 million cash at closing

$14 million earnout, years 1 through 4, tied to Lunar’s standalone revenue and EBITDA

$10 million earnout, years 5 through 7, tied to “operational efficiency metrics” determined by MedStack

$3 million vendor financing note, 4% interest, ten year amortization

Buzz’s lawyer flagged none of the structural problems. MedStack’s representatives were charming, professional, and emphasized the headline number at every meeting. Buzz signed within six weeks of the first conversation.

By year three, MedStack had pivoted Lunar’s product roadmap toward a competing platform they had acquired six months after Buzz’s deal. The “operational efficiency metrics” governing years 5 through 7 were calculated using formulas Buzz had never seen during negotiation. The vendor note was subordinated to a new senior credit facility within ninety days of closing.

Buzz’s total realization at year five: $9.4 million. The remaining headline value will not arrive.

Sally’s Structure: The Aligned Partnership

Sally’s transaction specialist was a chartered business valuator who had closed forty seven deals across the healthcare technology sector. Before any negotiation began, she ran a probability weighted present value analysis on MedStack’s initial $32 million proposal and calculated the real value at approximately $11 million. She showed the math to Sally on a single page.

Sally then made a decision Buzz never made. She told MedStack she would not accept their structure, but she would consider a partnership structure that aligned the incentives. The negotiation that followed lasted four months and produced a fundamentally different deal.

Sally’s Final Structure:

$14 million cash at closing

$5 million in MedStack equity, vesting over four years

$8 million earnout over three years, tied to combined healthcare technology segment EBITDA, not Apogee’s standalone results

$5 million minimum payment floor on the earnout, payable regardless of performance

Sally retained the CEO role for five years with strategic veto power on product roadmap, customer transitions, and personnel changes affecting Apogee’s core team

The cash at closing nearly tripled. The earnout was tied to combined performance, eliminating MedStack’s ability to manipulate Apogee’s standalone metrics. The minimum floor converted $5 million from contingent into deferred but certain. The strategic veto gave Sally tools to defend the operational decisions that determined earnout achievement.

The Outcomes Compounded Over Time

Year one, Sally’s CEO authority blocked a proposed product platform consolidation that would have crushed Apogee’s customer base. The combined healthcare technology segment grew 18% year over year. Sally’s earnout payment for year one came in at $3.2 million.

Years two and three, the segment continued to grow as Sally’s product expertise helped optimize three other portfolio companies within MedStack’s holdings. The earnout payments came in at full target. The MedStack equity Sally received as part of the deal appreciated as the broader portfolio grew.

By year five, Sally’s total realized value:

Cash at closing: $14 million

Earnout payments received: $8 million

Minimum payment floor: $5 million

MedStack equity, current value: approximately $12 million

Total realized value: $39 million

The same headline that delivered $9.4 million to Buzz delivered $39 million to Sally. The variance was structural, not strategic.

The Permanent Lesson

Sally’s transaction specialist later wrote an internal memo to her colleagues describing the deal as “a textbook example of structural negotiation.” The memo’s central observation was simple. Buzz negotiated the headline. Sally negotiated the structure. Both ended up with $32 million on paper. Only one ended up with $32 million worth of value.

Sally now mentors other healthcare technology founders. Her single piece of advice never changes. The price is the easy part. The structure is the deal. Hire someone who can read the structure before you fall in love with the price.

Twenty two months of negotiation work produced a $29.6 million difference in outcome. That is what terms trumping price actually looks like in real M&A practice.

All characters, businesses, and events in this case study are entirely fictional and created for educational purposes only. The names are inspired by real historical figures but represent fictional business owners with no connection to the actual persons, their families, or their estates. Any resemblance to real persons, businesses, or transactions is coincidental. This material does not constitute legal, financial, tax, or valuation advice. Consult qualified advisors for your specific situation.