Valuation Paralysis: Why Traditional Frameworks Fail AI Startups

You cannot value an AI seed-stage company the same way you value SaaS. Comparable analysis is fiction. Founder pedigree creates hyperscaler risk. Market sizing is speculation. Nobody has figured out w

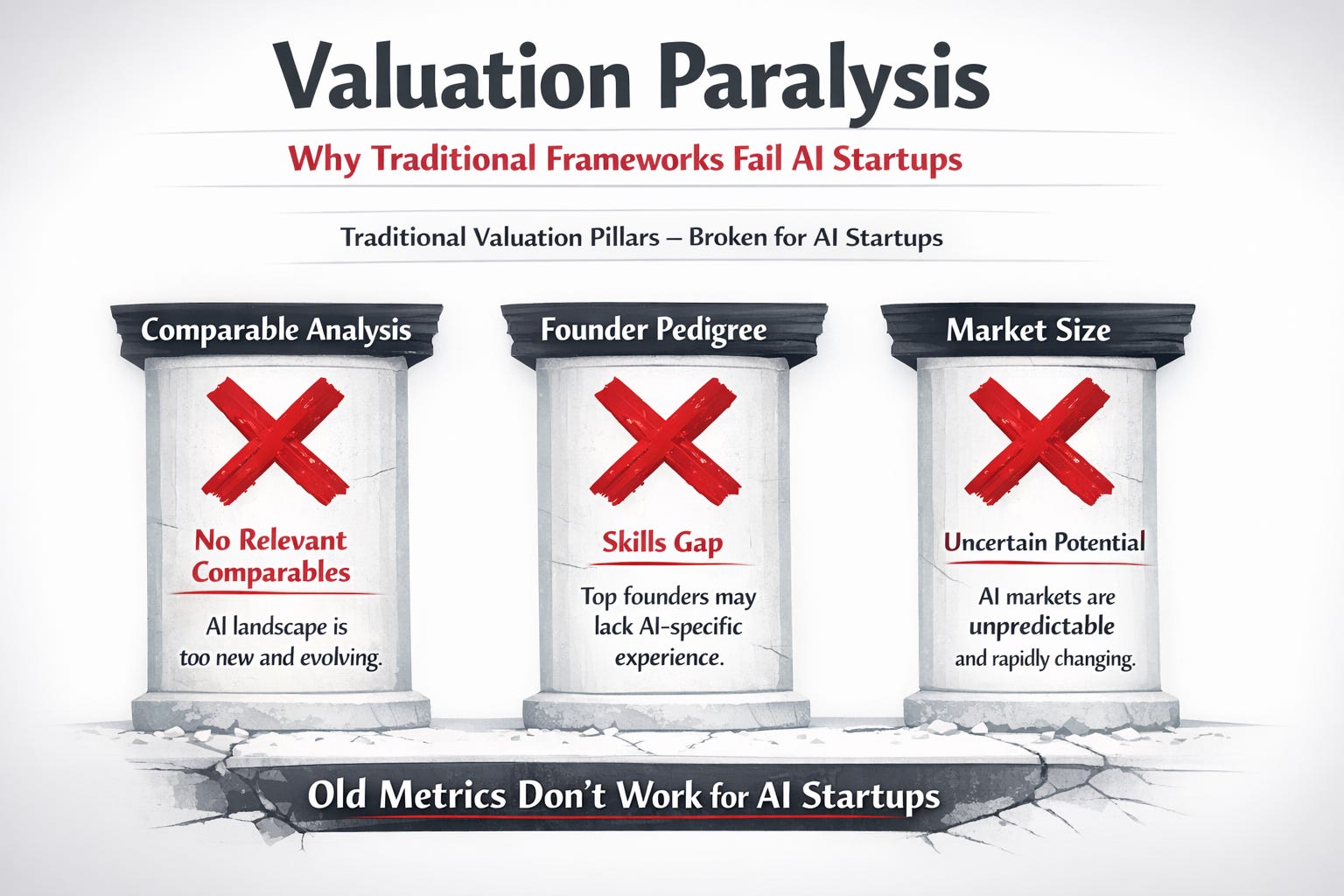

Traditional seed valuations rely on three pillars: comparable company analysis, founder pedigree, and total addressable market size. For AI startups, all three pillars are fundamentally broken. VCs are still using them because nothing better exists. This creates massive capital allocation inefficiency and destroys value for founders and investors alike.

10 KEY TAKEAWAYS - AI VALUATION CRISIS

1. Comparable analysis is fiction for AI: Which companies are comparable to your AI startup? None of them, or all of them.

2. Founder pedigree is hyperscaler risk: Premium credentials mean premium poaching probability. You pay up for what increases loss risk.

3. Market sizing is speculative fiction: You cannot do TAM analysis when you are creating a market that does not exist yet.

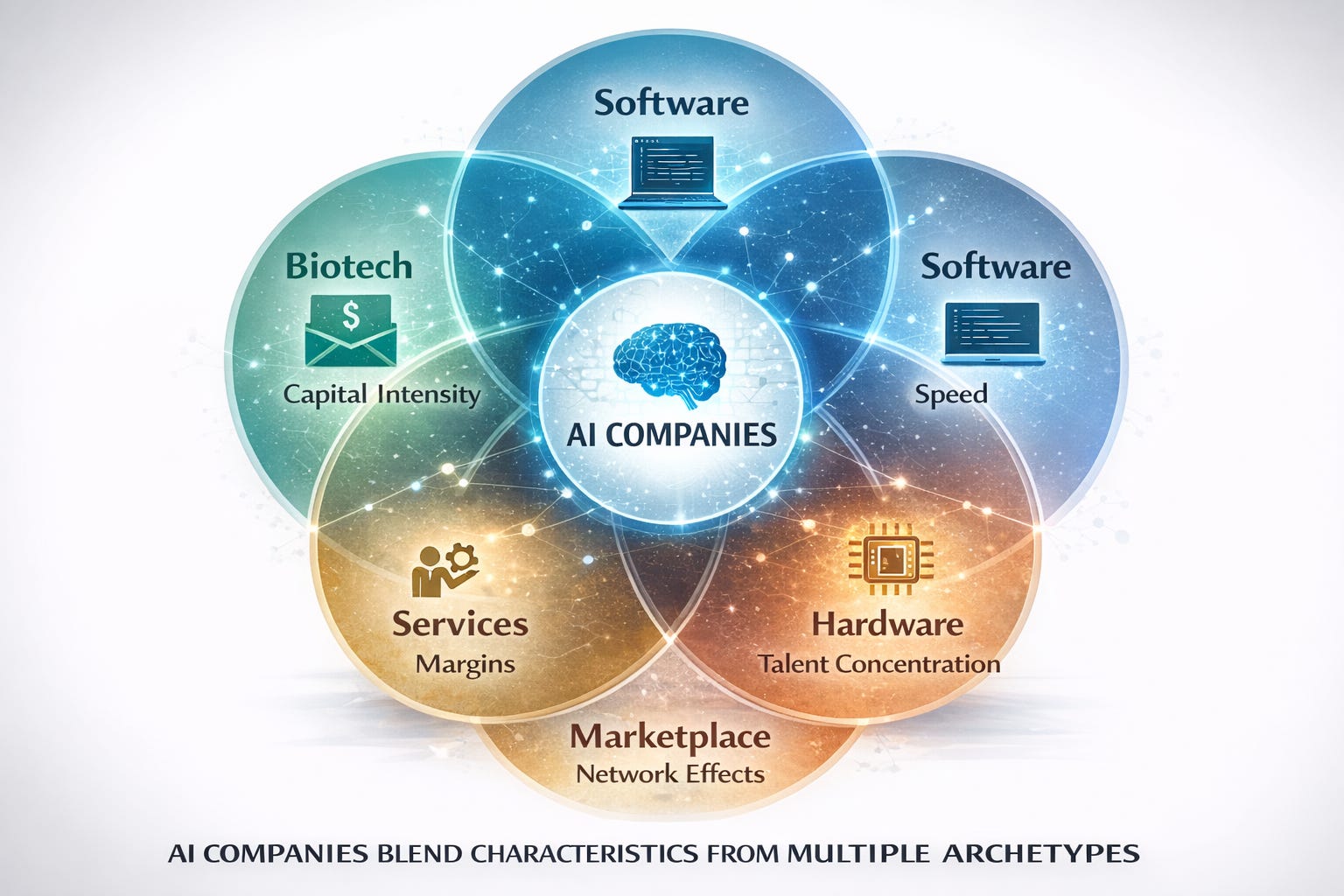

4. AI companies blend multiple archetypes: Biotech capital intensity, software speed, hardware talent concentration, services margins.

5. SaaS multiples create mispricing: Applying ARR multiples to AI companies ignores compute cost scaling and talent risk.

6. Too-high valuations create down rounds: Pricing based on hype leads to broken cap tables when reality emerges.

7. Too-low valuations crush founders: Excessive dilution before proving anything misaligns incentives and hurts recruiting.

8. New frameworks are needed: Talent retention risk, commodity horizon, data moat strength, integration depth.

9. Revenue guarantees bypass valuation problems: The VC Risk Swap avoids fixed-price equity by aligning capital with actual outcomes.

10. Adaptive structures acknowledge uncertainty: Milestone-based funding adjusts to reality rather than forcing false precision upfront.

📚 READING PREREQUISITES

This post builds on concepts from earlier posts including AI company taxonomy, compute economics, reverse acqui-hire dynamics, and enterprise versus consumer strategies. Understanding these risk factors provides essential context for evaluating why traditional valuation frameworks fail.

Recommended Prior Reading:

• Post 1: The AI Valley of Death - Why Seed Funding Timelines Are Broken

• Post 2: Pure AI vs. AI-Enabled - The Taxonomy That Determines Fundability

• Post 3: The Compute Trap - Why AI Startups Burn Seed Capital in Months

• Post 4: The Reverse Acqui-Hire Crisis - When Your Team Becomes Your Liability

• Post 5: Enterprise vs. Consumer AI - Why B2B Is the Only Sustainable Path

• Series overview available at SaferWealth.com

The Three Broken Pillars of Traditional Valuation

Traditional seed valuations rely on three pillars: comparable company analysis, founder pedigree and team quality, and total addressable market size. For AI startups, all three pillars are fundamentally broken, yet most VCs continue using them because nothing better exists.

Broken Pillar 1: Comparable Company Analysis Is Fiction

Which companies are comparable to your AI video generation startup? Runway? Different business model. Haiper? They got acqui-hired. Pika? Private, unknown financials. OpenAI? They raised $100B at completely different scale.

You end up either comparing to companies that are not actually comparable, or using such a wide range of potential comps that the valuation becomes meaningless. Every AI company claims they are different and pioneering new categories, which is often true but makes valuation comparison impossible.

Broken Pillar 2: Founder Pedigree Is Hyperscaler Risk

Yes, your founders worked at DeepMind, have PhDs from Stanford, and published in NeurIPS. That is impressive and suggests technical capability. It also means Google, Microsoft, or Anthropic will hire them in 18 months, leaving you with worthless equity.

Premium pedigree creates premium reverse acqui-hire risk. You are paying up for the very factor that increases probability of total loss. Traditional valuation frameworks treat pedigree as pure upside. For AI companies, it is a double-edged sword.

Broken Pillar 3: Market Size Is Speculative Fiction

You are not addressing a market. You are trying to create one. AI markets do not exist in the traditional sense until someone builds a product that defines the category. You cannot do bottoms-up market sizing when usage patterns are unknown. You cannot do TAM/SAM/SOM analysis when adoption curves are unpredictable.

VCs end up accepting wild market size claims because there is no data to disprove them, then pricing rounds based on optimistic scenarios that rarely materialize.

Why AI Companies Defy Existing Valuation Categories

The fundamental problem is that AI companies have characteristics from multiple existing company archetypes without fitting any single one cleanly:

• Biotech-like capital intensity: Need $5M-$50M before showing real traction, similar to drug development

• Software-like speed expectations: Ship products in months, not years like traditional R&D

• Hardware-like talent concentration: 3-5 key people are the entire value, like chip design teams

• Services-like variable margins: Compute costs scale with revenue, unlike pure software

• Marketplace-like network effects: Data improves models, models attract users, users generate data

Traditional valuation frameworks assume companies fit one category. AI companies fit none, which creates mismatches everywhere. A biotech-style milestone-based valuation makes sense for capital intensity but ignores speed-to-market pressure. A SaaS multiple makes sense for margins but ignores compute cost scaling. A talent-driven valuation makes sense for concentration risk but ignores that talent might leave for hyperscalers.

Three Flawed Approaches VCs Currently Use

Most VCs are doing one of three things when valuing AI companies. None of them are satisfying:

Approach 1: Avoid the Problem Entirely

Just pass on AI deals or only write small experimental checks. This is the safest personal career move. You cannot be blamed for losses you never took. But it means missing the defining technology shift of the decade. VCs pursuing this strategy will have clean track records and no AI winners in their portfolio.

Approach 2: Price in Massive Dilution

Assume 50-60% of the company will evaporate through reverse acqui-hires, feature commoditization, or hyperscaler competition. Price rounds as if you are buying twice as much equity as the term sheet says. A 20% ownership deal gets priced as 10% ownership because half the equity will turn worthless.

This approach creates higher effective valuations than founders realize and massive tension when actual dilution happens.

Approach 3: Use Non-Equity Structures

Revenue guarantees, debt-like instruments, or hybrid securities that hedge downside while preserving upside. This is where the VC Risk Swap and similar structures come in. They acknowledge that traditional equity pricing does not match AI risk profiles and create alternative mechanisms.

The honest reality: VCs are taking bigger leaps of faith than they would admit in partner meetings. AI seed-stage valuation remains more art than science, more negotiation than analysis, and more hope than math.

Toward Better AI Valuation Frameworks

Here is what a more honest AI startup valuation framework might include:

Talent retention risk score (0-10): How likely are founders and key engineers to leave for hyperscalers in next 24 months? Factors include founder age and wealth, hyperscaler connections, team size, and technical uniqueness. Higher risk equals lower valuation.

Commodity horizon (months): How long until foundation model improvements make your differentiation obsolete? Longer horizon equals higher valuation. Products with 6-month commodity horizons cannot justify venture scale valuations.

Data moat strength (0-10): How defensible is your proprietary data? Quality, exclusivity, network effects. Stronger data moat equals higher valuation, but most AI companies overestimate their data moat.

Enterprise integration depth (0-10): How painful is it for customers to switch? API wrapper equals 0. Deep platform integration with change management requirements equals 10. Higher integration depth justifies higher valuations.

Compute cost trajectory: Are unit economics improving or degrading as you scale? Companies whose margins deteriorate with growth cannot sustain venture-scale businesses.

Hyperscaler conflict score (0-10): How likely are Google, Microsoft, or Amazon to see you as competitive threat worth crushing? Higher conflict equals higher risk equals lower valuation. Companies in hyperscaler blind spots can command premiums.

This framework is still imperfect, but it is more honest about AI-specific risks than pretending SaaS comps make sense. The real work is in calibrating scores. What does a 7 on talent retention risk actually mean quantitatively? How do you weight different factors? What is the math that converts these scores into equity prices?

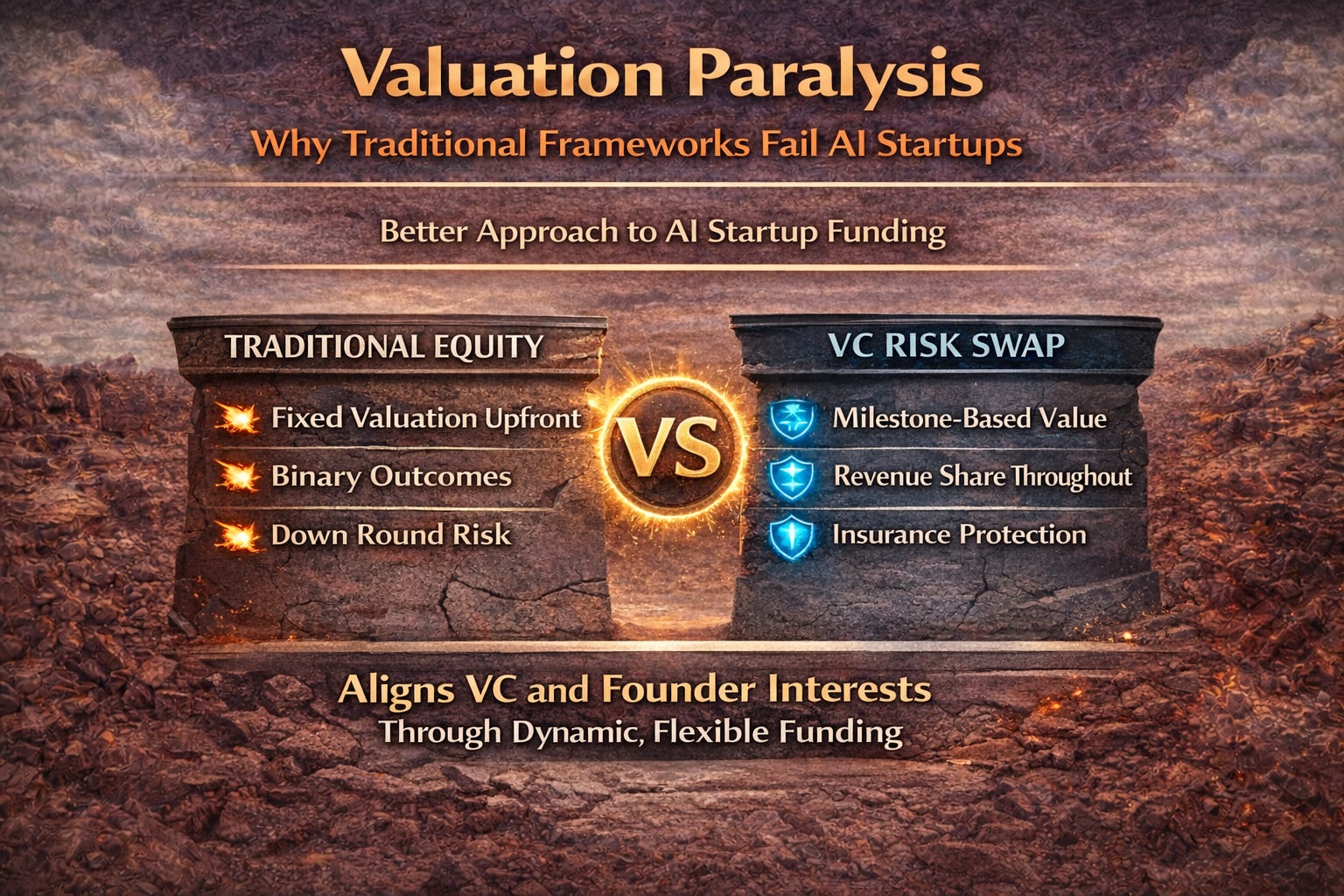

The VC Risk Swap: Bypassing Valuation Paralysis

Nobody has definitive answers yet on how to value AI companies properly. The VC Risk Swap offers an alternative approach: bypass the valuation problem entirely by using structures that adjust based on actual outcomes rather than forcing impossible upfront precision.

How the VC Risk Swap Addresses Valuation Uncertainty:

Avoids fixed-price equity decisions: Traditional equity requires agreeing on a valuation before anyone has real data. The VC Risk Swap provides capital through revenue guarantees, deferring equity decisions until business value becomes clearer. No one has to pretend they know what the company is worth before it has proven anything.

Milestone-based value realization: Instead of betting everything on one upfront valuation, the structure releases capital as milestones are achieved. First enterprise contract triggers additional funding. Technical validation unlocks next tranche. Value gets established through demonstrated progress, not speculative negotiation.

Risk-appropriate returns: Revenue share mechanisms provide returns throughout the funding period, not just at exit. Funders receive compensation for risk as value is created, rather than waiting for binary exit outcomes. This acknowledges that AI company outcomes exist on a spectrum, not just success or failure.

Downside protection independent of valuation: The insurance component provides capital recovery mechanisms regardless of what the company ends up being worth. Funders do not need to price in catastrophic loss scenarios because the structure hedges them directly.

Why This Matters for AI:

• Acknowledges uncertainty: Nobody pretends to know what the company is worth before proving anything

• Avoids down round dynamics: No inflated valuation to collapse later when reality emerges

• Preserves founder equity: No excessive dilution based on guesswork valuations

• Provides funder protection: Insurance and revenue share reduce reliance on exit multiples

• Creates aligned incentives: Both parties benefit from actual progress rather than valuation games

Traditional fixed-price equity rounds create false precision. AI companies are too uncertain for false precision. Better to create adaptive structures that acknowledge uncertainty and align incentives as information emerges.

What This Means for Founders and Investors

For Founders:

• Understand that your valuation is basically made up. Not because VCs are stupid, but because the frameworks do not exist yet.

• If a VC offers you a $20M post-money valuation for your pre-revenue AI company based on comps, they either do not understand AI or they are setting you up for a down round when reality emerges.

• Better to take a $10M valuation with protective structures than a $20M valuation that creates future problems.

• Consider alternative structures that acknowledge uncertainty rather than forcing false precision.

For Investors:

• If you are using SaaS multiples to value AI companies, you are either overpaying or underpricing risk. Probably both simultaneously.

• Build better frameworks or stick to valuations so low they survive any reasonable downside scenario.

• The first VC firm that develops a rigorous, defensible AI startup valuation framework will eat everyone’s lunch for the next decade.

• Consider non-equity structures that hedge uncertainty rather than forcing precision you cannot have.

The honest approach for both sides: acknowledge the valuation uncertainty explicitly. Structure deals with mechanisms that adjust based on actual outcomes rather than pretending you can predict them upfront.

💡 KEY TAKEAWAYS

Remember These Core Principles:

• Traditional frameworks are broken: Comps, pedigree, and market sizing all fail for AI companies

• AI companies blend multiple archetypes: No single existing framework captures the risk profile

• The VC Risk Swap bypasses valuation problems: Milestone-based funding avoids forcing false precision

• Acknowledge uncertainty explicitly: Better to structure for adjustment than pretend you know

• Beware inflated valuations: A lower valuation with protection beats a higher one that creates future problems

❓ FREQUENTLY ASKED QUESTIONS

Q: Why do traditional valuation frameworks fail for AI startups?

A: Three pillars of traditional valuation are broken for AI. Comparable analysis fails because no true comps exist for pioneering AI categories. Founder pedigree creates hyperscaler risk rather than pure upside since prestigious backgrounds increase poaching probability. Market sizing is speculative because AI companies create markets rather than entering existing ones.

Q: Why is founder pedigree actually a risk factor for AI companies?

A: Premium credentials from DeepMind, Stanford, or OpenAI signal technical capability but also signal attractiveness to hyperscalers. The same pedigree that justifies higher valuations increases probability of reverse acqui-hire. You are paying a premium for the factor most likely to cause total loss. Traditional frameworks treat pedigree as pure upside when it is actually a double-edged sword.

Q: What characteristics make AI companies hard to categorize?

A: AI companies blend multiple archetypes: biotech-like capital intensity requiring $5M-$50M before traction, software-like speed expectations for product shipping, hardware-like talent concentration where 3-5 people hold all value, services-like variable margins where compute scales with revenue, and marketplace-like network effects where data improves models. No single framework captures all these dimensions.

Q: How does the VC Risk Swap address valuation uncertainty?

A: The VC Risk Swap bypasses fixed-price equity decisions by providing capital through revenue guarantees with milestone-based releases. Value gets established through demonstrated progress rather than speculative negotiation. Revenue share provides returns throughout funding rather than requiring exit multiples. Insurance provides downside protection independent of valuation. The structure acknowledges uncertainty rather than forcing false precision.

Q: Should founders accept high valuations from investors who do not understand AI?

A: No. A $20M valuation based on broken frameworks sets you up for a down round when reality emerges. Better to take a $10M valuation with protective structures or a VC Risk Swap that acknowledges uncertainty. Inflated valuations create cap table problems, misaligned expectations, and future fundraising difficulties. The goal is building a company, not maximizing paper valuations that collapse.

🎯 READY TO ESCAPE VALUATION PARALYSIS?

Understanding why traditional valuation frameworks fail is the first step toward better capital structures. The VC Risk Swap offers an alternative that acknowledges uncertainty rather than forcing false precision.

Subscribe to SaferWealth for insights on alternative startup funding structures, AI commercialization strategies, and the VC Risk Swap framework. Join founders and funders who are building better capital structures for the AI era.

Have questions about your specific situation? Drop a comment below or reach out directly. I respond to every message.

📖 RELATED READING

Continue Your Learning:

• a16z Valuation Frameworks: Andreessen Horowitz perspectives on startup valuation methodologies.

• PitchBook Valuation Data: Industry data on AI startup valuations and round sizes.

• First Round Capital Startup Insights: Seed-stage investment perspectives and valuation discussions.

CONNECT WITH SAFERWEALTH

Expand Your Learning Beyond This Post:

1. Web: SaferWealth.com - Alternative Startup Funding Structures

2. YouTube: TheCapitalToolkit - VC Risk Swap Educational Content

3. LinkedIn: LinkedIn @SaferWealth - Startup Finance Innovation

4. Rumble: @saferwealth - Educational video content on alternative funding

5. Instagram: @saferwealth - Quick insights and updates

👤 ABOUT THE AUTHOR

Sean Cavanagh, BAS, CPA, CA, CF, CBV

With over three decades in business valuations, M&A advisory, and tax structuring, Sean delivers unvarnished truth about startup funding challenges. Starting at Deloitte and Canada Revenue Agency, he now advises founders and funders on alternative capital structures through SaferWealth.com. The VC Risk Swap framework reflects his frustration with funding structures that consistently fail AI startups.

Connect with Sean:

• 🌐 SaferWealth.com

📚 DO YOUR OWN RESEARCH

The concepts discussed in this article are grounded in industry data and market analysis. Below are authoritative sources for readers who want to dive deeper:

Valuation Resources:

• Investopedia - Startup Valuation Methods

• Investopedia - Term Sheet Basics

• Investopedia - Total Addressable Market

AI Company Research:

• CB Insights - AI Startup Valuations

• PitchBook - AI Funding Analysis

• Crunchbase - AI Company Data

AI Companies Referenced:

• OpenAI

This section empowers readers to verify information, explore topics deeper, and develop their own informed perspectives on AI startup valuation challenges.

⚖️ EDUCATIONAL DISCLAIMER

This guide provides information only, not professional advice. Consult qualified advisors for your specific situation. All cases are fictional, created for educational purposes from collective industry experience. Neither the author nor SaferWealth accepts liability for actions based on this content. This material supplements but never replaces proper professional consultation and judgment.

SaferWealth is an educational platform dedicated to helping founders and funders understand alternative capital structures for AI startups.

© 2026 SaferWealth. All rights reserved.