VC Exit Door Is Bricked Shut

Venture’s whole model depends on the exit, and in 2026 the exit door is bricked shut. Here is the liquidity doom loop strangling non-AI startups, and the funding that pays out without an IPO.

The Exit Door Is Bricked Shut

Every venture deal is a promise about a door at the far end. An IPO. An acquisition. A payday that makes the risk worth it. In 2026, someone bricked that door shut. Money goes in, almost nothing comes out, and for non-AI founders that jammed exit is not a distant worry. It is the trap you are already standing in.

[Suggested image: a fire-exit door welded shut with a heavy chain, an EXIT sign still glowing above it. Alternative: a brick wall freshly laid across a doorway.]

The Door at the End of Every Deal

Strip venture capital down to its plumbing and it is a liquidity machine. Limited partners hand money to a fund. The fund deploys it into startups. The startups, in theory, grow and exit through an IPO or an acquisition. The cash flows back, the LPs get paid, and they recommit to the next fund. Every part of that loop depends on the last one: the exit. Jam the exit, and the whole machine seizes.

In 2026, the exit is well and truly jammed. The single most sobering number in venture right now: if unicorns kept exiting at the pace of recent years, clearing the backlog would take roughly 49 years. The pipeline is not draining, it is clogged with companies too large to be easily acquired and too expensive for the current public markets. We spent a decade minting billion-dollar companies and forgot to build them an exit.

The drought is now structural. The market is four years deep into a liquidity crunch, and net cash flows to LPs have been negative by about $169 billion since 2022. Nearly half of all unicorns have now been held for nine years or more. The people who funded the last decade of startups are still waiting to be paid.

To feel how abnormal this is, rewind to 2021, when the United States saw close to 400 venture-backed IPOs in a single year. The next year that number fell off a cliff, and it has never truly recovered. An entire generation of companies was built on the quiet assumption that the public market would be waiting at the finish line. Instead it went home and locked the gate behind it

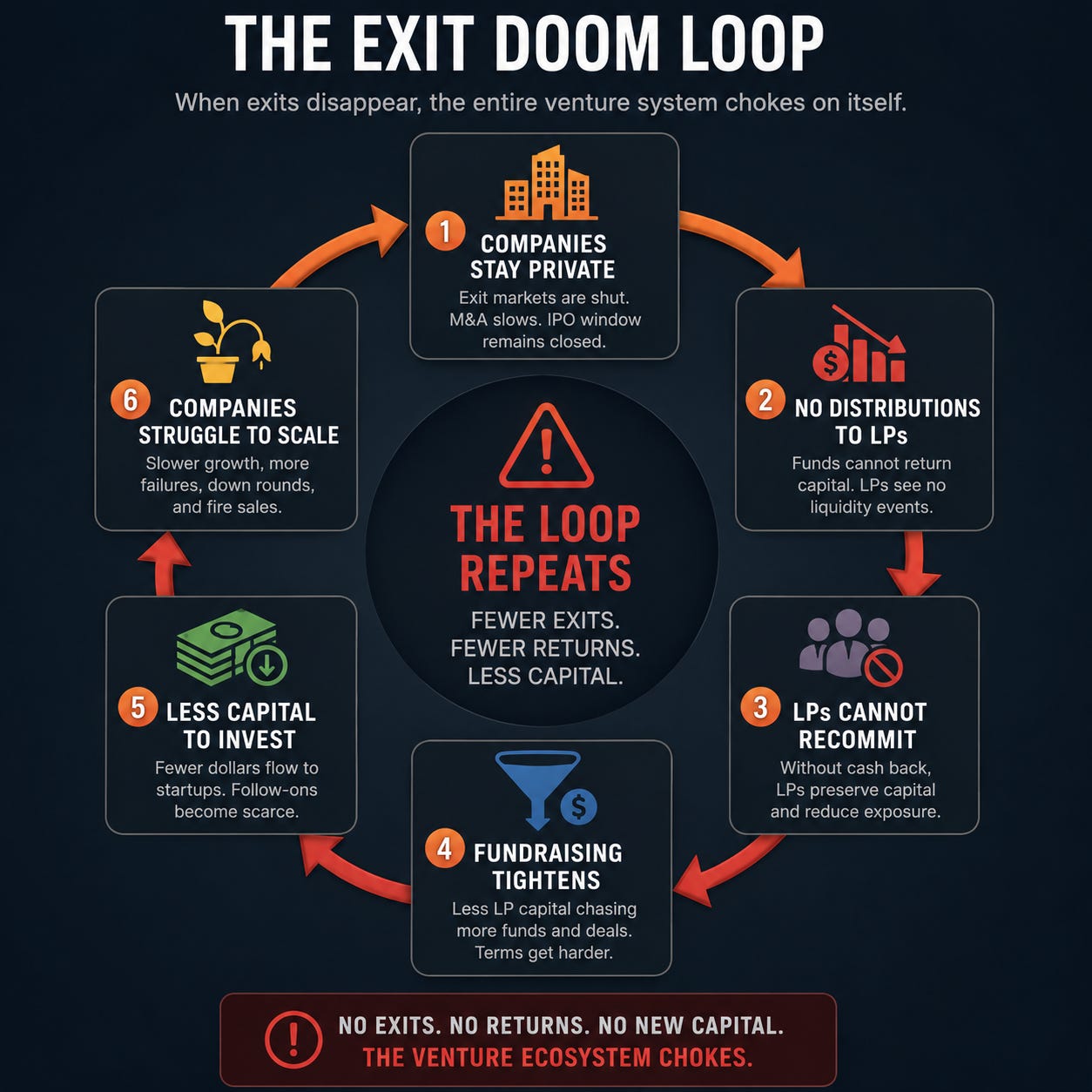

.The Doom Loop

Here is where it turns vicious, because the problem feeds itself. Companies cannot exit, so LPs receive no distributions. With no distributions, LPs cannot, or will not, recommit. Fundraising tightens and concentrates in a few established firms. Less capital reaches new startups, and the companies already in the system are forced to stay private even longer, which clogs the exit further. Round and round it goes, each lap pulling a little more oxygen out of the room.

[Suggested image: a circular flow diagram of the doom loop: companies stay private, no distributions, LPs cannot recommit, fundraising tightens, less capital, repeat. (Use the exit-doom-loop diagram from the visual set.)]

You can see the desperation in the workaround. Venture secondaries, where founders and investors sell their stakes to each other rather than wait for a real exit, hit roughly $293 billion in 2025, and over the year to mid-2025 even outran the total value of venture-backed IPOs. Secondaries have hit an all-time high. When the front door is bricked shut, everyone starts climbing out the window.

But a window is not a door. Secondaries are a pressure valve, not a cure, and the price of using them keeps rising. Shareholders who held for eight years counting on an IPO are now staring at year ten, eleven, twelve, and as more sellers pile in, buyers tighten and the clearing price drops. This is liquidity by haircut, and the haircut gets deeper the longer the door stays shut.

The squeeze radiates outward. Starved of distributions, LPs ration new commitments and funnel what remains to a few brand-name funds, leaving everyone else fundraising into a headwind. Some managers now lean on continuation vehicles, essentially selling companies to themselves, just to manufacture a distribution. Cambridge Associates expects these vehicles to account for a meaningful slice of all distributions in 2026. When an industry has to invent liquidity, the real thing is conspicuously missing.

Why the Bricked Door Hurts Non-AI Most

“But the IPO window is reopening,” someone always says. Sort of. It is cracking open for a handful of giants. The mega-IPOs that might unclog the system could be the tide that lifts all boats, or the wave that capsizes the market, soaking up the public-market demand that exists. Either way, the door opens for them, not for you. The selective thaw is an AI-and-mega-cap thaw.

So the non-AI founder gets the worst of both worlds: all of the exit pressure, none of the exit. You inherit the seven to ten year clock, the board pushing for the big outcome, the whole machine built around an eventual sale, while the door that sale depends on is welded shut for everyone but the mega-caps. You are told to build toward a payday that the market has quietly cancelled.

Even the funds themselves have stopped pretending. They are now openly hunting alternative financing structures for companies that are not IPO or M&A ready, engineering partial liquidity because the traditional kind has gone missing. When the people who built the exit-dependent model start shopping for a way around it, that is your signal. The door is not opening for you. It is time to stop waiting at it.

The human cost is quieter than a crash but just as real. Companies that cannot exit and cannot raise become zombies, alive but going nowhere, their equity frozen on paper nobody can spend. Founders who poured a decade in cannot get liquid. Employees holding options watch them gather dust. Down rounds and recaps wait at the end of the runway. For a non-AI company, the bricked door does not announce itself with a bang. It just quietly removes every way out

Why The VC Risk Swap Doesn’t Need the Door

This is the quiet brilliance of the VC Risk Swap in a frozen market: it pays out without an exit. Value returns through milestones, on a schedule, no IPO and no acquisition required. The funder gets defined, downside-protected liquidity without waiting a decade for a bricked door to crack open. The founder is freed from building toward a door that may never open, keeps the company and the equity, and keeps building. In a market where the exit is bricked shut, a structure that returns capital without one is not a clever workaround. It is the main road.

Subscribe to SaferWealth for more field notes from a market that forgot to build its own exit, plus the structures that pay founders and funders without one.

Questions about your specific situation? Reach out directly at riskswap@saferwealth.com.

CONNECT WITH SAFERWEALTH

Expand your learning beyond this post:

1. Web: SaferWealth.com, alternative startup funding structures.

2. YouTube: The Capital ToolKit, funding strategy and structure breakdowns.

3. Rumble: @SaferWealth.

4. Contact: riskswap@saferwealth.com.

ABOUT THE AUTHOR

Sean Cavanagh (BAS, CPA, CA, CF, CBV) is the founder of SaferWealth and creator of the VC Risk Swap, an alternative startup funding structure that preserves founder equity and control through milestone-based, downside-protected capital. With over three decades in business valuation, M&A advisory, and structuring, Sean writes about funding the businesses the venture market overlooks.

DO YOUR OWN RESEARCH

Sources referenced in this post:

• The VC Corner, the liquidity crisis doom loop, the 49-year backlog and $293B in secondaries.

• PitchBook, the mega-IPOs that could shut out the rest of VC, four years of drought and the selective thaw.

• 2026 US Venture Capital Outlook, $169B in negative LP cash flows and 9+ year holds.

• Earlyasset, the 2026 private market bifurcation, rising secondary discounts and stranded shareholders.

• Cambridge Associates 2026 outlook, secondaries at an all-time high.

• Strut Consulting, the 2026 VC landscape, funds engineering alternative liquidity.

📖 RELATED READING

• The VC Corner: The Liquidity Crisis Doom Loop: the clearest map of the cycle starving the asset class.

• PitchBook: The Mega-IPOs That Could Shut Out the Rest of VC: why the thaw favours giants, not you.

• Earlyasset: The 2026 Private Market Bifurcation: liquidity by haircut, explained.

Educational disclaimer: This content is for educational purposes only and does not constitute legal, tax, financial, or investment advice. The VC Risk Swap is a sophisticated structure that must be implemented with independent professional advisors for your specific situation. All examples are illustrative. Neither the author nor SaferWealth accepts liability for actions based on this content. This material supplements but never replaces proper professional consultation and judgment.

© 2026 SaferWealth. All rights reserved.